Key Stats for American Tower Stock

- 52-Week Range: $155 to $234

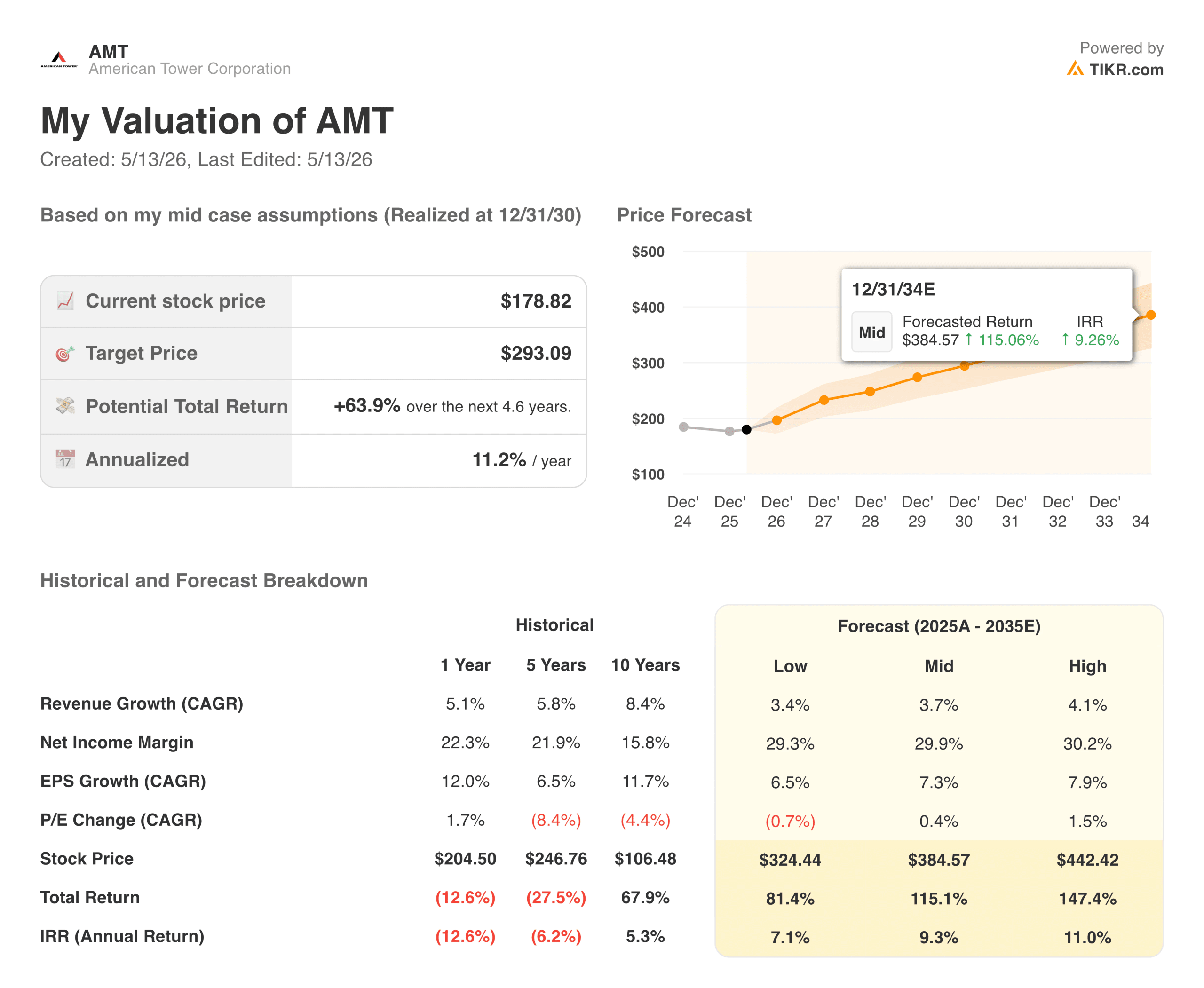

- Current Price: $178.82

- Street Mean Target: ~$235

- TIKR Target Price (Mid): ~$293

- TIKR Annualized IRR (Mid): ~11% per year

- Q1 2026 Revenue: $2.75B (beat estimates by ~3%)

- Q1 2026 Net Income: $877M (up ~76% YoY)

- FY2026 Adjusted FFO Guidance: $9.80 to $10.00 per share

Value your favorite stocks like AMT with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

How the India Exit and Margin Recovery Changed the AMT Story

American Tower (AMT) owns roughly 226,000 communication sites globally: cell towers, rooftop antennas, and distributed antenna systems used by wireless carriers and 5G networks. Carriers lease space on those towers under long-term contracts with automatic annual rent escalators. The revenue is predictable, the costs are largely fixed, and the margin structure is among the best in real estate.

The last few years, though, have been about the noise rather than the business. Rising interest rates hit REITs broadly, and AMT’s India operations added complexity and cost on top of that. The combination of compressed margins and weighing on multiple.

That chapter is largely closed. AMT completed its India exit, simplified the portfolio, and the results have followed. Q1 2026 revenue of $2.75 billion beat estimates by roughly 3%, and net income of $877 million grew 76% year over year. Management raised full-year Adjusted FFO guidance to $9.80 to $10.00 per share.

The margin chart tells the story. Operating margins dipped from 38% in 2021 to 30% in 2022 amid international headwinds. From there, the recovery was steady: around 35% in 2023, 45% in 2024, and 46% in 2025. That is a business that went through a messy transition and came out cleaner on the other side.

See analysts’ growth forecasts and price targets for AMT stock (It’s free!) >>>

Why Wall Street Sees Meaningful Upside From Here

Street consensus sits around $235, with most analysts at Outperform or Buy. The view is that the stock hasn’t fully priced in the margin improvement or the AI infrastructure tailwind.

The near-term driver is 5G densification. As carriers build denser networks to handle higher data volumes, they need more tower leases and more small cells. AMT is a landlord to every major US carrier, and those leases automatically renew at higher rates. In Europe and Latin America, 5G rollout is still in early innings, adding a multi-year runway internationally.

The longer-term thesis is CoreSite. Data centers are the physical layer on which AI runs, and CoreSite’s interconnection-focused campuses bring cloud providers, enterprises, and carriers together in a single facility. It positions AMT as more than a tower company. It makes AMT an infrastructure landlord for the AI economy.

What the EPS Recovery Looks Like From Here

Normalized EPS dipped from $4.62 in 2021 to $3.82 in 2022 and stayed flat through 2023. The recovery started in 2024 at $4.82, reached $5.40 in 2025, and consensus sees a meaningful step-up ahead: around $6.50 in 2026, around $7 in 2027, and approaching $9.50 by 2030.

A quick note for REIT investors: Adjusted Funds from Operations (AFFO) is the more useful metric here than GAAP EPS. It strips out depreciation on tower assets, which are long-lived and don’t actually deteriorate the way accounting assumes. AMT’s FY2026 AFFO guidance of $9.80 to $10.00 per share is the anchor to use when considering dividend coverage and valuation.

Either way, the direction is the same. Earnings compressed during the transition years and are now re-accelerating on a cleaner business.

Value AMT instantly (Free with TIKR) >>>

What the TIKR Model Implies at the Current Price

The TIKR model targets around $293 in the mid case, implying a total return of roughly 64% over about 4.6 years, or about 11% annually.

The assumptions are grounded. Revenue growth of around 4% per year is consistent with AMT’s historical tower escalator profile. Net income margins of around 30% reflect the current operating margin base flowing through to GAAP earnings. EPS growth of around 7% annually reflects steady compounding rather than a heroic inflection.

The low case targets around $325 at roughly 7% per year. The high case reaches around $440. Even the conservative scenario implies meaningful upside from the current price.

The Case for AMT: Compounding Leases, Pricing Power, and AI Infrastructure

The tower business is structurally durable. Carriers cannot build dense networks economically on their own, and once antennas are installed on a tower, switching is not a realistic option. Lease terms run for 10 years or more with automatic escalators, producing revenue that compounds in the background regardless of market conditions.

The AI layer makes the thesis more interesting. AI applications require low-latency, high-bandwidth connectivity, pushing carriers to densify their networks and, in turn, leading to more tower leases. CoreSite captures the data center side of that same spending cycle.

The dividend adds a return floor that growth stocks can’t offer. It’s well covered by AFFO and has grown steadily, which matters to investors who want income alongside capital appreciation.

The Risks: Rates, Leverage, and Slow Top-Line Growth

AMT is a REIT, so interest rates matter a lot. When rates are high, the present value of long-duration cash flows shrinks, and investors can find comparable yields in lower-risk places. The rate environment has been the dominant headwind for three years, and if rates stay elevated, the multiple re-rating takes longer.

Leverage is another consideration. AMT carries a meaningful debt load, and sustained high rates increase refinancing costs over time.

And top-line growth of around 4% annually is steady, not exciting. The return thesis here is about margin expansion, multiple re-rating, and a dividend that keeps growing, not a revenue acceleration story.

Is AMT Worth Buying at $179?

American Tower is a compounder, not a momentum trade. Long-term leases with embedded escalators, margins above 45%, a data center business growing alongside AI demand, and a dividend paid through cycles make the return profile more predictable than most.

The TIKR mid-case target of around $293 at roughly 11% per year is a competitive return for a business this predictable. The margin recovery is real and hasn’t fully shown up in the multiple. EPS rising from $5.40 in 2025 to an estimated $9.50 by 2030 reflects a business quietly doing its job while the market waits for a reason to pay attention.

For patient investors who want infrastructure over growth, the current price looks like a reasonable entry into a business that fixed what needed fixing.

See analysts’ growth forecasts and price targets for AMT stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!