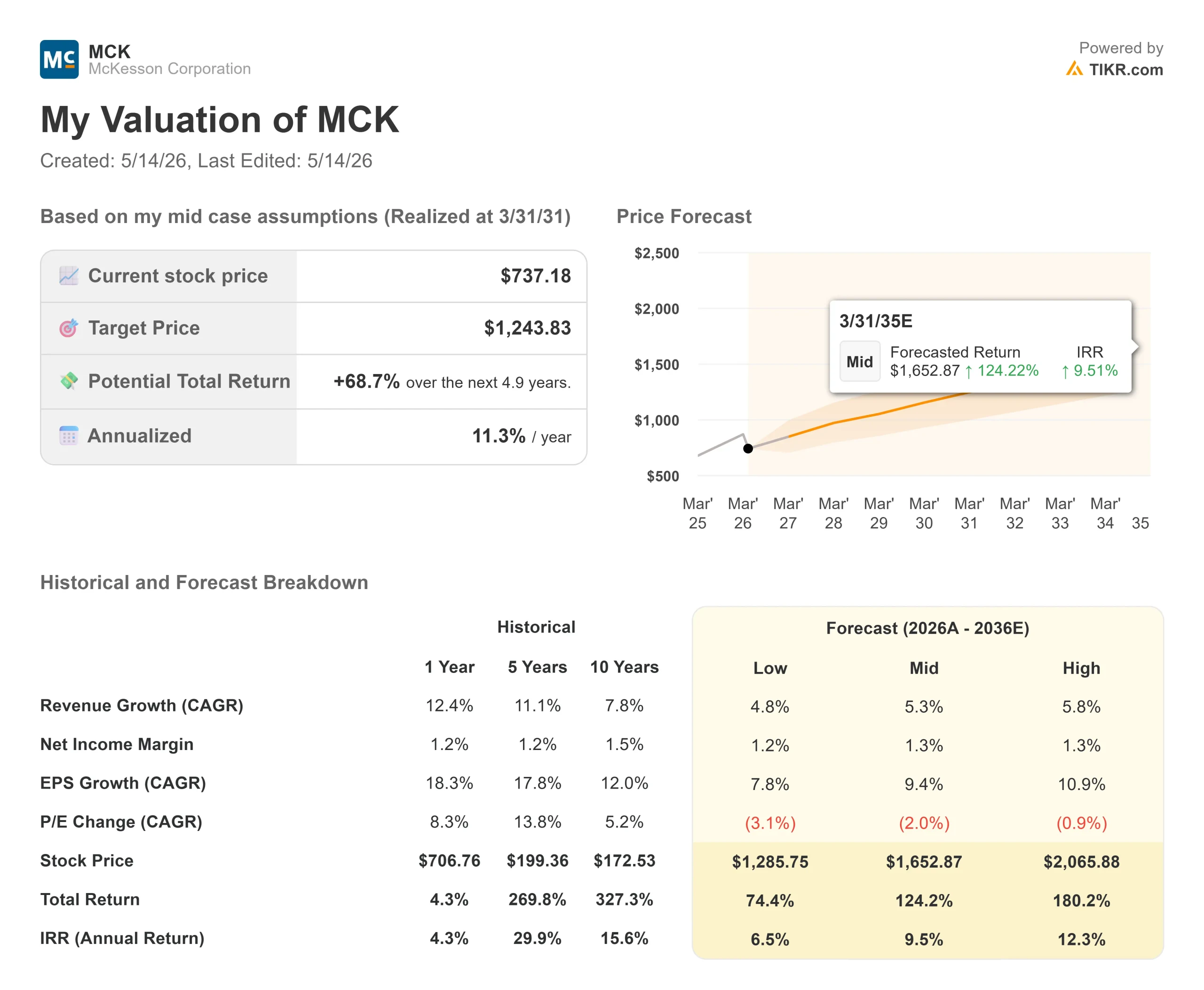

Key Stats for McKesson Stock

- Current Price: $737.18

- Target Price (Mid): ~$1,244

- Street Target: ~$950

- Potential Total Return: ~69%

- Annualized IRR: ~11% / year

- Earnings Reaction: -2.47% (May 7, 2026)

- Max Drawdown: 27.17% on 5/11/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

McKesson Corporation (MCK) has lost 26% from its 52-week high of $999.00, and the bear case has been building for months. GLP-1 drug volumes are slowing. Branded pharmaceutical prices are declining. A revenue miss on May 7 appeared to confirm it all. The stock fell 2.47% on earnings day, then got dragged down again when sector-wide selling pushed MCK roughly 7% lower in a single session alongside peer Cencora (COR), which fell 17.2% in the same move.

Revenue of $96.3 billion missed analyst estimates of roughly $101.4 billion by more than 5%. That headline is hard to shake in a week.

But the bear case has a central flaw: it treats revenue as a proxy for profit. At McKesson, those two figures do not move together. CFO Britt Vitalone addressed this directly at the Bank of America Global Healthcare Conference on May 12, and his explanation matters.

Why the Revenue Miss Was Not a Profit Miss

The shortfall came from two sources: manufacturer list price declines known as WAC, or wholesale acquisition cost, on branded drugs, and a sequential slowdown in GLP-1 distribution volumes in the fiscal fourth quarter. Both compressed revenue. Neither hurt profit.

Vitalone was direct: “We are paid a fair value on a fixed fee-for-service basis for the services that we provide on behalf of the manufacturers and their products. And so if there’s a change in that WAC or list price, it doesn’t have an impact to us.”

The numbers back that up. In the fourth quarter, the North American Pharmaceutical segment actually expanded adjusted operating profit margins by 9 basis points, even as WAC declines hit the top line. Three of four segments delivered double-digit adjusted operating profit growth in the quarter.

The GLP-1 story is similar. McKesson distributed roughly $53 billion in GLP-1 medications in fiscal 2026, growing more than 25% for the full year. Growth slowed sequentially in the fourth quarter to above 20%, and Vitalone acknowledged it. But he also noted that oral GLP-1 formulations are now showing up as an additive to total prescription volumes, not as substitutes for injectables, which expands the addressable market.

The full-year profit picture was strong. Adjusted operating profit grew 15%, and adjusted EPS grew 18% to $39.11 in fiscal 2026. The Oncology and Multispecialty segment alone delivered operating income of $1,149 million, up from $767 million the prior year, a roughly 50% jump driven by platform acquisitions in community oncology and eye care. Fiscal 2027 guidance calls for adjusted EPS of $43.80 to $44.60, another 12 to 14% increase, with each core segment at the upper end of McKesson’s long-range targets.

See historical and forward estimates for McKesson stock (It’s free!) >>>

The Reshaping the Market Is Undervaluing

Beyond the earnings, McKesson is executing a portfolio transformation that is not in the current price.

On April 20, McKesson announced a definitive agreement with Apollo Funds for a $1.25 billion investment in its Medical-Surgical Solutions (MMS) business, acquiring roughly a 13% minority stake at an implied valuation of approximately $13 billion. McKesson retains operating control and majority ownership. The deal is a precursor to a planned MMS IPO expected in the second half of calendar 2027.

Vitalone detailed the groundwork at the BofA conference: MMS is legally and operationally separate, has audited carve-out financial statements, and now carries an independent revolving credit facility and Term Loan A. Apollo’s experience with complex carve-outs joins the board. The valuation uncertainty that hung over MMS for the past year has a public anchor.

What remains after the separation is a focused McKesson centered on three platforms: North American Pharmaceutical distribution, Oncology and Multispecialty, and Prescription Technology Solutions (RxTS). The RxTS segment is often underestimated. About 55% of its revenue comes from third-party logistics, a distribution-like business contributing less than 5% of segment operating profit. The rest of the prior authorizations, affordability solutions, and denial conversion tools are technology-driven, higher-margin, and directly tied to specialty pharmaceutical growth. McKesson added more than 40 new programs to its RxTS platform in fiscal 2026 alone.

On the cost side, Vitalone pointed to 293 basis points of operating leverage from automation and AI: demand planning tools, ambient scribe in oncology practices, and chatbots replacing manual call center workflows. He called it “early innings.”

Is the Fear Rational?

Three concerns are driving the selloff. Each has a direct answer.

GLP-1 deceleration is real but overstated as a risk. Slowing from above 25% to above 20% growth on a $53 billion annual distribution base is not a thesis-breaking development. Oral GLP-1 formulations are expanding the market, not displacing it.

WAC price declines on branded drugs like STELARA hurt revenue but not profit. McKesson’s fee-for-service model holds its economics through list price changes by design. And rather than watching the biosimilar transition from the sidelines, McKesson is entering that market directly through its North Star private-label portfolio, beginning with Stimufend, a biosimilar for Neulasta.

MMS separation risk is the most legitimate concern. Carve-outs are complex. But the Apollo investment resolves the headline valuation uncertainty, injects $1.25 billion of capital, and adds a partner with specific carve-out experience. The execution risk is meaningfully lower than it was before April 20.

What the multiples show: MCK now trades at 12.61x NTM EV/EBITDA and 16.65x NTM P/E. Six weeks ago, at the March 31 quarter-end, those same multiples sat at 15.20x and 19.87x, respectively. That kind of compression, against a business still guiding double-digit EPS growth, is what creates a genuine valuation opportunity.

The Street has not abandoned the stock. Of 17 analysts tracked by TIKR, 11 rate MCK a Buy, 4 Outperform, and 2 Hold. Zero rate it Underperform or Sell. The mean price target is $949.73 29% above today’s price. JP Morgan maintained Overweight while cutting its target to $1,015 after earnings. Deutsche Bank reiterated Buy at $875.

See how McKesson performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $737.18

- Target Price (Mid): ~$1,244

- Potential Total Return: ~69%

- Annualized IRR: ~11% / year

See analysts’ growth forecasts and price targets for McKesson stock (It’s free!) >>>

The TIKR mid-case model tracks closely with consensus estimates and McKesson’s own long-range targets. The two primary revenue drivers are specialty pharmaceutical volume growth, oncology, and GLP-1 distribution, and expanding RxTS technology services, together embedding a revenue CAGR of around 5% through March 2031. The EPS CAGR runs at approximately 9%, supported by operating expense leverage and a share repurchase program that has reduced McKesson’s share count by more than 23% over five years.

The margin driver is automation-led operating expense leverage. The mid-case net income margin assumption of around 1.3% is consistent with McKesson’s historical 1.2% to 1.4% range, reflecting the low-margin, high-volume structure of pharmaceutical distribution.

The primary risk is a sharper-than-expected deceleration in GLP-1 distribution whether from Medicare policy shifts, faster direct-to-consumer adoption, or manufacturer pricing changes that compress fee-for-service economics.

Conclusion

The thesis rests on one number: adjusted EPS for fiscal 2027. McKesson guided $43.80 to $44.60, with the midpoint roughly in line with what the Street expected before the earnings report. If the company delivers and the consistency of its earnings track record suggests the range is achievable, then 16.65x forward earnings looks like a discount to a quality compounder the market has temporarily mispriced.

The first checkpoint is the Q1 fiscal 2027 earnings report, currently expected around August 5, 2026. Watch two things: adjusted EPS on track with guidance, and GLP-1 distribution volumes holding above 20% growth. If both hold, the 26% discount to the 52-week high has a clear path to closing. If management cuts the EPS range or GLP-1 volumes fall meaningfully below 20%, the bear case earns real credibility.

The profit trajectory is intact. The strategic reshaping is on schedule. And 15 of 17 analysts still rate this stock a Buy or Outperform. The fear may be creating the entry point.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in McKesson?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up McKesson, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track McKesson alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze McKesson on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!