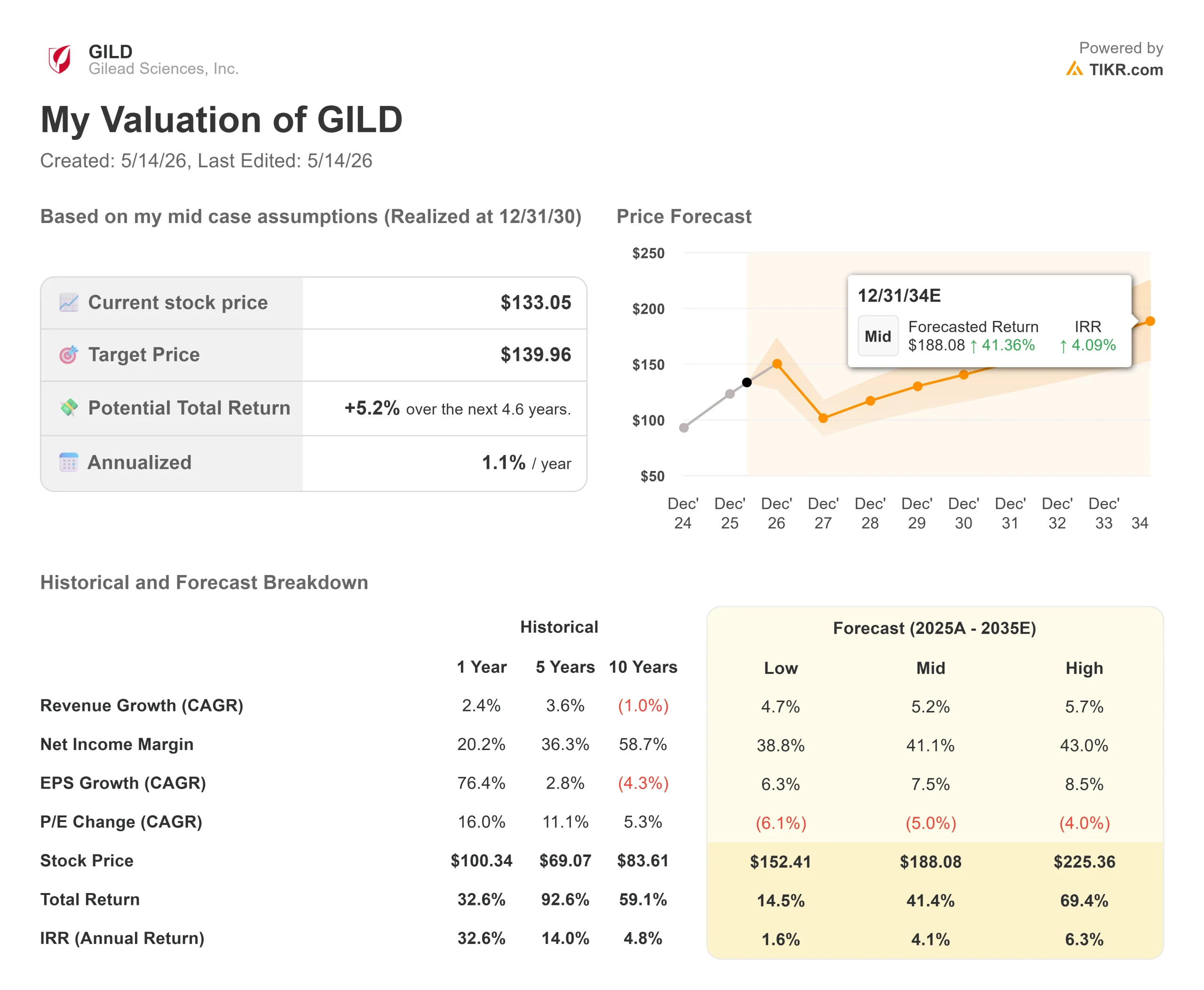

Key Stats for Gilead Sciences Stock

- Current Price: $133.05

- Target Price (Mid): ~$140

- Street Target: ~$158

- Potential Total Return: ~5%

- Annualized IRR: ~1% / year

- Earnings Reaction: -2.04% (5/7/26)

- Max Drawdown: -18.00% (4/27/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Gilead Sciences (GILD) beat Q1 2026 earnings on May 7 and watched the stock fall 2.04% anyway. Five days later, Chief Commercial Officer Johanna Mercier stepped onstage at the Bank of America Healthcare Conference and delivered something the earnings release couldn’t: a detailed look at the commercial mechanics behind three events arriving before December 23, any one of which could materially change how the market prices this stock.

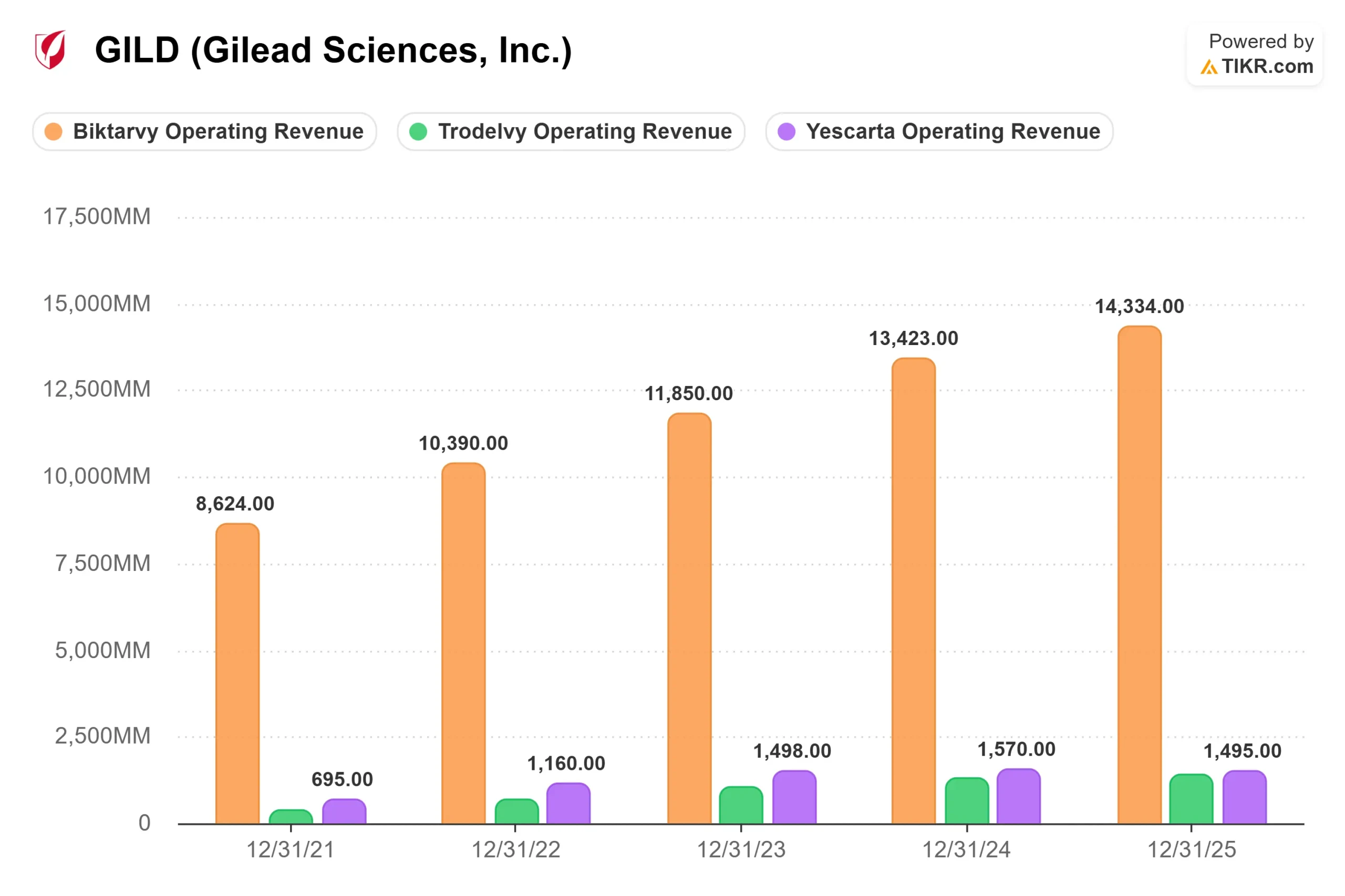

The base business is not the debate. Biktarvy holds over 52% of the U.S. HIV treatment market per Mercier’s remarks, the oncology franchise already exceeds $3 billion in annual revenue per TIKR segment data, and Yeztugo guidance was just raised from $800 million to $1 billion in its first full commercial year. The debate is what GILD is worth once you account for three second-half catalysts that the current $133 price does not fully reflect.

What the Conference Revealed That Earnings Headlines Missed

On Yeztugo, Mercier focused on retreatment rates, the share of patients returning for their second injection. “We are really encouraged to see the numbers right now of them coming back for their second injection,” she said, noting that specialty pharmacy partners initiate outreach a month before each patient’s scheduled return dose. That matters because the long-term thesis runs well past 2026. Mercier said she expects long-acting injectables to eventually capture 60% to 70% of the total PrEP (pre-exposure prophylaxis, a prevention regimen for people at risk of HIV) market over time.

She also flagged a pipeline extension: a once-yearly formulation targeting populations that the six-month product can’t efficiently reach, Department of Corrections settings, emergency rooms, and college campuses. That is a structural market expansion, not a product-cannibalization story.

On Trodelvy, the insight wasn’t the 37% year-over-year Q1 growth Gilead reported. It was why that growth accelerated. The NCCN (National Comprehensive Cancer Network, whose guidelines directly shape prescribing behavior) issued Category 1 guidelines its highest evidence level covering first-line metastatic triple-negative breast cancer (mTNBC, an aggressive subtype) earlier this year. Physicians began prescribing Trodelvy off-label in the first line ahead of formal approval, which also upgraded second-line prescribing behavior. “Many folks were still using older chemotherapies in the second-line setting,” Mercier said. “What we’ve been seeing with the data in the first-line setting is that it’s moved everybody up.” Formal first-line approval is expected in H2 2026.

The third event is the anito-cel FDA decision, with a PDUFA date of December 23, 2026. Gilead completed its $7.8 billion acquisition of Arcellx in late April, taking full ownership of anitocabtagene autoleucel (anito-cel, a BCMA-directed CAR T-cell therapy that reprograms a patient’s immune cells to attack multiple myeloma). The application targets fourth-line relapsed or refractory multiple myeloma, supported by a 96% overall response rate in the Phase 2 iMMagine1 trial.

Mercier’s commercial detail is what stood out. Gilead will have approximately 200 authorized treatment centers live before year-end. Prior CAR-T launches entered the market with roughly 25% of that number. “This will be kind of the biggest launch that we’ve seen with cell therapy with 200 ATCs,” she said. Anito-cel’s safety profile also lends itself to community oncology settings, where most multiple myeloma patients are actually treated.

See historical and forward estimates for Gilead Sciences stock (It’s free!) >>>

A $3.5 Billion Market Today, a $20 Billion Opportunity Over Time

Mercier was direct about the anito-cel runway. The fourth-line multiple myeloma entry point is approximately $3.5 billion. “But really, the opportunity is much greater than that,” she said. Because of anito-cel’s differentiated safety profile, Gilead is targeting earlier treatment lines second line and eventually first line which she sized as “a much larger market like a $20 billion addressable patient population.”

For perspective, Yescarta (Gilead’s existing CAR T-cell therapy for lymphoma) generated $1,495 million in 2025, per TIKR segment data. Anito-cel, successfully commercialized into earlier lines, would be the largest single growth driver in the oncology franchise’s history.

How the Valuation Actually Looks

At 28.71x NTM EV/EBITDA, GILD trades at a significant premium to AbbVie’s 12.72x and Amgen’s 10.49x per TIKR competitor data. But that gap is largely an artifact of acquisition-related charges hitting the 2026 income statement simultaneously. TIKR consensus projects 2027 free cash flow at approximately $13.3 billion as those charges roll off, which would put the stock at a normalized multiple much closer to peers, before crediting any of the three-year-end catalysts.

Biktarvy’s exclusivity runs to 2036, and Mercier noted approximately 70% of newly diagnosed HIV patients initiating therapy are starting on Biktarvy. That franchise doesn’t need to grow to fund the pipeline buildout; it needs to hold. And it is holding.

Of 32 analysts with active recommendations on GILD, 18 rate it Buy, 5 Outperform, 8 Hold, 1 No Opinion, and none carry a Sell. The mean Street target of approximately $158 implies around 19% upside from current levels a gap that reflects how the Street is already crediting pipeline execution above what the TIKR base model assumes.

See how Gilead Sciences performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $133.05

- Target Price (Mid): ~$140

- Potential Total Return: ~5%

- Annualized IRR: ~1% / year

See analysts’ growth forecasts and price targets for Gilead Sciences stock (It’s free!) >>>

The TIKR mid-case model targets approximately $140 by December 31, 2030, using a revenue CAGR of around 5% and net income margins expanding toward around 41%. The two revenue drivers are the Yeztugo PrEP ramp and Trodelvy’s first-line mTNBC expansion, which Mercier described as doubling both the addressable patient population and the average duration of treatment. The primary risk is a negative anito-cel outcome in December, which would remove the single most important re-rating catalyst of the year.

At the mid-case, total return from current levels is around 5% through 12/31/30, with an annualized return near 1%. The Street’s mean target of ~$158 implies the consensus view already credits execution above the TIKR base case, making the December 23 FDA decision the clearest test of whether that premium is earned.

Conclusion

The GILD thesis for H2 2026 hinges on December 23. Anito-cel approval at the fourth-line indication, with 200 ATCs already operational, validates the $7.8 billion Arcellx acquisition and opens the pathway to what Mercier sized as a $20 billion market with line expansion. A complete response letter resets the oncology re-rating narrative.

Watch Trodelvy’s first-line mTNBC FDA decision first, as it arrives earlier in H2 2026 and is a lower-risk signal. NCCN Category 1 designation already created off-label prescribing momentum, so an approval confirms execution rather than surprises anyone. If both catalysts arrive on schedule, the question shifts from whether Gilead can diversify to how fast the revenue mix changes, and that question is worth considerably more than the current $133 price implies.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Gilead Sciences?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Gilead Sciences, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Gilead Sciences alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Gilead Sciences on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!