Key Takeaways:

- Duolingo (DUOL) reported Q1 2026 revenue of $292 million, up 27% year-over-year, with net income rising 24% to $43.5 million, but the company maintained rather than raised its annual revenue guidance.

- The stock has declined approximately 80% from its 52-week high of $541 to around $105, and Argus Research downgraded it to “hold” in March 2026.

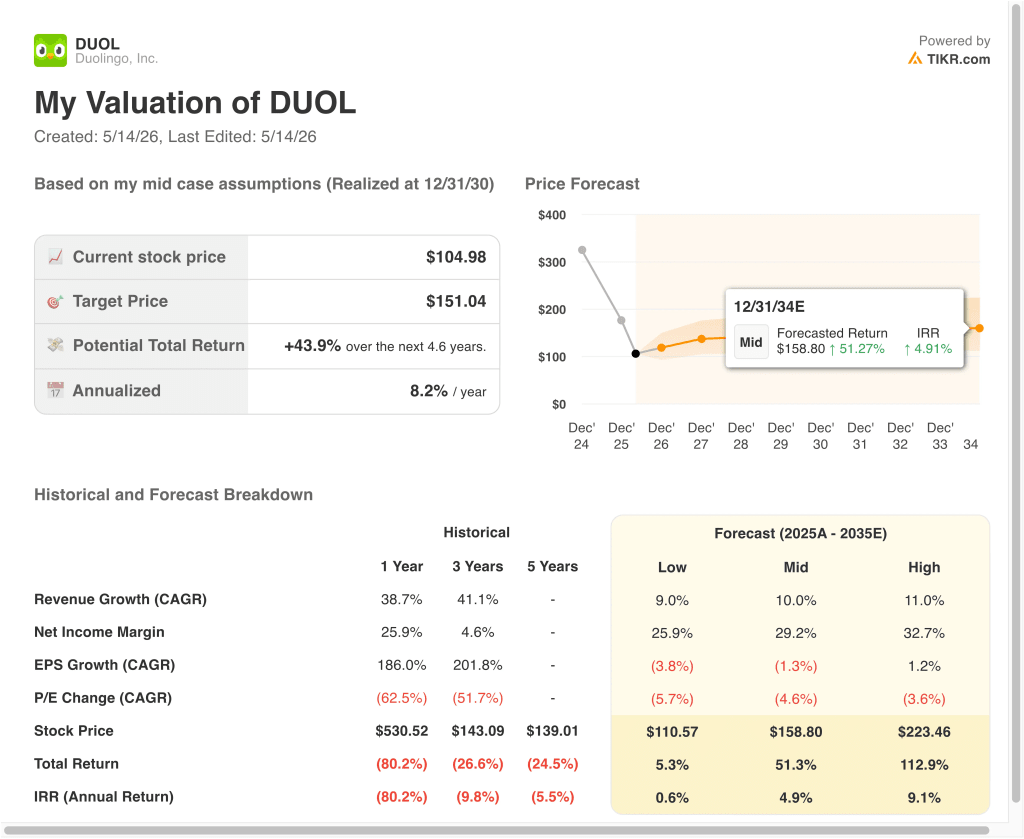

- DUOL stock could reasonably reach around $151 per share by December 2030, based on our valuation assumptions.

- This implies a total return of around 44% from today’s price of $105, with an annualized return of 8.2% over the next 4.6 years.

What Happened?

Duolingo, Inc. (DUOL) is the world’s most downloaded language learning app, offering gamified lessons in over 40 languages through a freemium model. The company reported Q1 2026 revenue of $292 million, up 27% year-over-year, and net income of $43.5 million, up 24%. But the stock has fallen approximately 80% from its 52-week high of $541 to around $105 as of mid-May 2026.

Duolingo’s freemium model means most users access the app at no cost. A smaller paying segment subscribes to Duolingo Plus for an ad-free experience and advanced features, and a premium tier called Duolingo Max offers AI-powered conversation practice. So revenue growth depends directly on converting free users into paying subscribers and expanding that paid base over time.

Argus Research downgraded the stock to “hold” in March 2026, reflecting concern about slowing growth momentum. The current street consensus price target of $104 sits just below the current price of $105, suggesting that most analysts view the stock as roughly fairly valued at this level. But the company holds net cash of approximately $1.16 billion, providing strong financial stability with no debt burden.

Duolingo’s AI-powered Duolingo Max tier represents the next growth frontier, but adoption and monetization of AI features remain early-stage. LTM gross margin of 72.7% and EBIT margin of 14.8% show the business is profitable and operationally sound.

However, the forward two-year EPS CAGR is negative, reflecting the near-term drag from elevated AI development investment. And the forward two-year revenue CAGR of 15.1% is solid but no longer exceptional relative to the premium multiples the stock once commanded.

Here’s why Duolingo stock could offer modest near-term returns from this level, but long-term investors should weigh the limited upside implied by the extended model with care.

What the Model Says for DUOL Stock

We analyzed the upside potential for Duolingo stock based on its global language learning platform leadership, growing AI-powered product features, and improving profitability as its freemium monetization model scales over time.

Based on estimates of 14.1% annual revenue growth, 10.7% operating margins, and a normalized P/E multiple of 15.4x, the model projects Duolingo stock could rise from $105 to around $142 per share.

That would be a 35% total return, or a 12% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for DUOL stock:

1. Revenue Growth: 14.1%

Duolingo’s one-year revenue CAGR was 38.7%, and the three-year CAGR was 41.1%. But the company is now signaling a more moderate growth trajectory, choosing to prioritize user engagement over near-term monetization. Q1 2026 revenue grew 27% year-over-year, which is healthy but below the company’s historical pace.

Based on analysts’ consensus estimates, we used a 14.1% revenue growth forecast, reflecting a realistic forward path as Duolingo’s user base matures and the company faces tougher year-over-year comparisons.

This rate also aligns with the forward two-year consensus revenue CAGR of 15.1%, suggesting the 14.1% assumption is consistent with broader analyst expectations for the business.

2. Operating Margins: 10.7%

Duolingo’s LTM EBIT margin was approximately 8.4%, reflecting profitable but investment-heavy operations. The gross margin of 72.7% provides a healthy foundation for future margin improvement as operating leverage kicks in. But the company is spending heavily on AI feature development and user acquisition.

Based on analysts’ consensus estimates, we used a 10.7% operating margin target, reflecting modest improvement as AI investments generate higher-value monetization and the company achieves greater leverage on its fixed cost base.

And this level of margin improvement appears achievable over the next few years without requiring aggressive monetization changes that could risk damaging user engagement.

3. Exit P/E Multiple: 15.4x

Duolingo currently trades at a forward NTM P/E of around 15.4x, dramatically below its historical range of 36x to 87x. This multiple compression reflects the sharp deceleration in growth expectations and the broader correction in consumer tech valuations. And the street consensus target of $104 suggests analysts are not pricing in a meaningful recovery in the near term.

Based on analysts’ consensus estimates, we maintained a 15.4x exit multiple, acknowledging that this substantially compressed P/E could represent fair value if growth stays subdued, but could also represent a significant discount if the company’s AI product monetization re-accelerates meaningfully.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for DUOL stock through 2034 show varied outcomes based on subscriber growth, AI product monetization, and global language learning demand (these are estimates, not guaranteed returns):

- Low Case: Subscriber growth stalls and AI investments fail to drive meaningful revenue monetization → 0.6% annual returns

- Mid Case: Steady subscriber growth and moderate AI product contribution support gradual revenue and earnings improvement → 4.9% annual returns

- High Case: AI-powered features successfully monetize and drive accelerating revenue growth and margin expansion → 9.1% annual returns

Going forward, Duolingo stock faces a nuanced setup because the near-term model projects attractive returns of around 12% per year, but the long-term scenario model implies very limited upside through 2034.

The stock’s 80% decline from its peak has created a much more reasonable entry point on a near-term basis. But investors should closely track whether the company’s AI features can reignite growth above the current 14% to 15% trajectory, since that is the variable that most separates the mid case from the high case in this model.

See what analysts think about DUOL stock right now (Free with TIKR) >>>

Should You Invest in Duolingo?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DUOL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DUOL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!