Key Takeaways:

- Mastercard (MA) beat Q1 2026 estimates with adjusted EPS of $4.60 versus the $4.40 consensus, and guided for full-year adjusted net revenue growth at the high end of low double digits to low teens.

- The company announced the acquisition of BVNK, a platform connecting blockchain-based and traditional fiat payment infrastructure, expanding Mastercard’s position in digital payments.

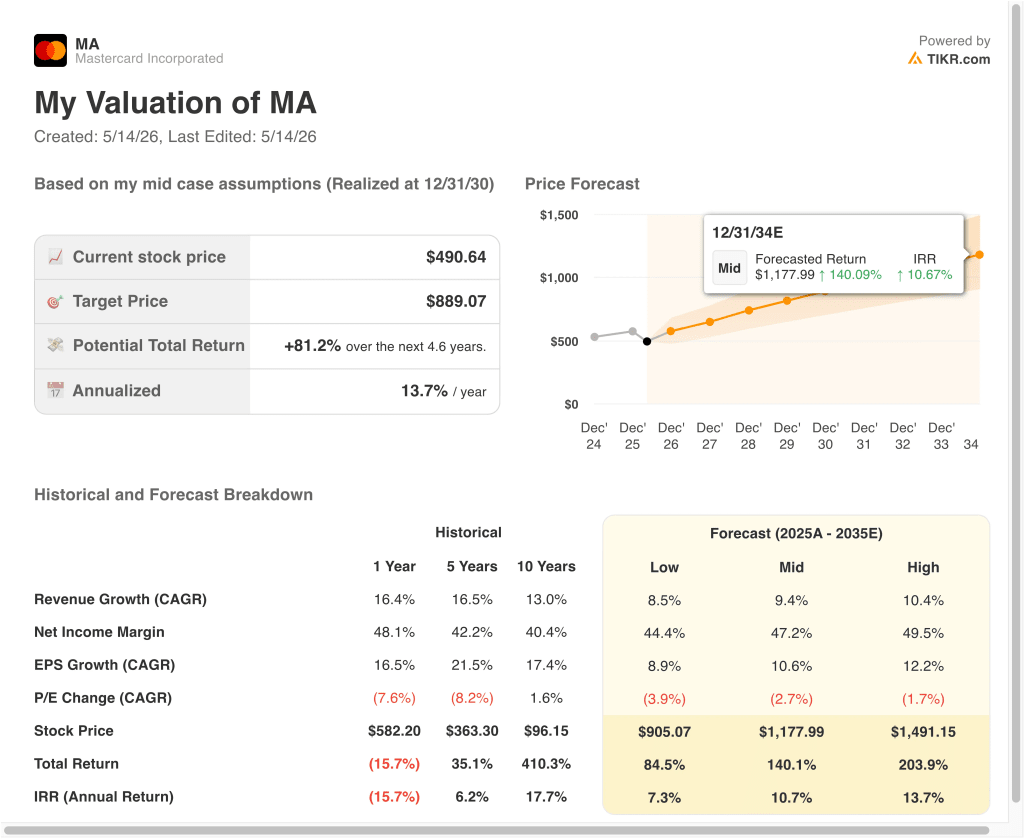

- MA stock could reasonably reach around $889 per share by December 2030, based on our valuation assumptions.

- This implies a total return of around 81% from today’s price of $491, with an annualized return of 13.7% over the next 4.6 years.

What Happened?

Mastercard Incorporated (MA) operates one of the world’s two dominant payment networks, facilitating electronic transactions between cardholders, issuing banks, and merchants globally. The stock declined 12.6% year-to-date through mid-May 2026, underperforming the broader market despite a strong earnings quarter.

In Q1 2026, Mastercard delivered adjusted EPS of $4.60, beating the $4.40 analyst consensus. Management guided for full-year adjusted net revenue growth at the high end of low double digits to low teens, implying around 12% to 13% growth. And the company also recorded a restructuring charge of $202 million in Q1, reflecting ongoing optimization of its workforce and cost base.

Several strategic developments are reshaping Mastercard’s long-term positioning. The company announced it will acquire BVNK, a platform that bridges blockchain-based payment infrastructure with traditional fiat currency payment systems.

This positions Mastercard to capture fee revenue as on-chain digital payments grow. Amazon also launched a Prime Business Card co-branded with U.S. Bank and Mastercard, adding a high-volume commercial relationship to its network.

However, the UK Financial Conduct Authority opened a competition investigation in May 2026 into Mastercard’s, Visa’s, and PayPal’s digital wallet arrangements. So investors are pricing in some regulatory risk alongside the strong operational performance.

Consumer spending has remained broadly resilient. CFO Sachin Mehra cited continued steady growth across affluent and mass-market consumer segments in recent commentary. Mastercard’s LTM gross margin is 100.0%, and EBIT margin is 59.5%, reflecting the highly efficient two-sided network model where the platform earns a fee on every transaction it processes.

Here’s why Mastercard stock could deliver meaningful returns as global cashless payment volumes expand and its investments in digital payment infrastructure scale.

What the Model Says for MA Stock

We analyzed the upside potential for Mastercard stock based on its global payment network duopoly, expanding cross-border and digital transaction volumes, and its highly scalable business model with near-100% gross margins.

Based on estimates of 12.5% annual revenue growth, 60.0% operating margins, and a normalized P/E multiple of 24.2x, the model projects Mastercard stock could rise from $491 to around $745 per share.

That would be a 51.8% total return, or a 17.1% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for MA stock:

1. Revenue Growth: 12.5%

Mastercard grew revenue at a 16.4% CAGR over the past year, and the 10-year CAGR sits at 13.0%. Global electronic payment penetration continues expanding, particularly in emerging markets where cash still dominates. And cross-border transaction volumes, which carry premium fees, have recovered strongly since pandemic-era travel restrictions eased.

Based on analysts’ consensus estimates, we used a 12.5% revenue growth forecast, reflecting modestly more conservative growth as market penetration matures in developed markets, balanced against continued expansion in high-growth emerging economies and new digital payment verticals.

The forward two-year consensus revenue CAGR of 12.8% also provides strong support for this assumption, since it aligns closely with recent and historical performance.

2. Operating Margins: 60%

Mastercard’s LTM operating margin was approximately 58.4%, and the company has historically operated in the upper 50s to low 60s percent range. The business model is highly scalable because incremental transaction volume adds minimal marginal cost to the platform. But the Q1 2026 restructuring charge of $202 million introduced short-term cost noise.

Based on analysts’ consensus estimates, we used a 60.0% operating margin target, reflecting Mastercard’s trajectory toward the top of its historical margin range as efficiency initiatives and technology investments pay off. And the structural shift toward higher-margin digital transactions also supports this outlook.

3. Exit P/E Multiple: 24.2x

Mastercard trades at a forward NTM P/E of around 24.2x, below its historical average of approximately 30x to 32x. This multiple compression reflects near-term caution around the UK FCA regulatory probe and macroeconomic sensitivity to consumer spending trends. But the underlying business fundamentals remain strong.

Based on analysts’ consensus estimates, we maintained a 24.2x exit P/E, reflecting a conservatively set multiple relative to Mastercard’s historical range that acknowledges current regulatory and macro uncertainty without assuming a worst-case regulatory outcome.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for MA stock through 2034 show varied outcomes based on global payment volume growth, digital payment expansion, and regulatory environment (these are estimates, not guaranteed returns):

- Low Case: Regulatory headwinds and slower emerging market growth limit revenue and margin expansion → 7.3% annual returns

- Mid Case: Steady global cashless payment growth and BVNK-driven digital integration support consistent earnings → 10.7% annual returns

- High Case: Accelerating cross-border volumes and successful digital asset fee capture drive above-consensus growth → 13.7% annual returns

Going forward, Mastercard stock will likely reflect investor sentiment around the pace of global payment digitization and the outcome of the UK FCA investigation.

The 12.6% year-to-date decline has made the valuation more attractive relative to recent history, and the near-term model projects around 17.1% annualized returns. But the regulatory probe and macro uncertainty are real risks that investors should monitor closely as the story develops through 2026.

See what analysts think about MA stock right now (Free with TIKR) >>>

Should You Invest in Mastercard?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track MA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!