Key Stats

- Current Price: €31 (May 14, 2026)

- Q2 FY2026 Revenue: €618M, +8% reported / +14% constant currency YoY

- Q2 FY2026 Adjusted EPS: €0.50, down 9% YoY

- FY2026 Revenue Guidance: €2.3B–€2.35B (+10%–12% reported, +13%–15% constant currency)

- FY2026 Adjusted EPS Guidance: €1.90–€2.05

- TIKR Model Price Target: €52

- Implied Upside: ~75%

Birkenstock Q2 FY2026 Earnings Breakdown

Birkenstock stock (BIRK) generated €618M in Q2 revenue, up 8% on a reported basis and 14% in constant currency, absorbing a 640 basis point FX headwind from the sharp depreciation of the dollar and other non-euro currencies.

Adjusted EPS came in at €0.50, down from €0.55 in Q2 FY2025, with €0.09 of the decline attributable to FX translation and €0.08 to a noncash revaluation of an embedded derivative in the company’s senior notes.

APAC led all segments at 30% constant-currency growth, more than twice the pace of the other regions, with India, China, and Japan delivering the strongest individual results.

Americas grew 14% in constant currency, supported by B2B sell-through at key partners that was up over 30%, according to CEO Oliver Reichert on the Q2 earnings call.

EMEA grew 11% in constant currency, but Reichert disclosed that the Middle East conflict reduced EMEA revenue by approximately €6M and cut consolidated growth by about 100 basis points.

Own retail was up over 60% in constant currency with same-store sales accelerating to double digits from Q1, and the company added 5 new doors to bring the global total to 111 against a fiscal year-end target of 140.

Adjusted EBITDA was €198M, down 1% YoY; excluding the €27M FX translation drag, EBITDA grew 13%, per CFO Ivica Krolo on the Q2 earnings call.

Birkenstock reiterated full-year guidance for 13%–15% constant-currency revenue growth, targeting €2.3B–€2.35B in reported revenue with approximately 350 basis points of FX headwind embedded in the full-year figure.

Adjusted EPS guidance of €1.90–€2.05 includes €0.15–€0.20 of FX pressure, and the company confirmed that a €179M share repurchase authorization remains available, with open market purchases now under active consideration as the business enters its seasonally strong cash generation period.

The company estimated IEEPA tariff refund claims of approximately €30M, though timing remains uncertain as refund filings are pending the next administrative steps in the U.S. customs process.

Birkenstock Stock’s Income Statement: Margin Pressure Arrives in Force

Birkenstock stock is navigating a period of real margin compression, as FX and tariff headwinds are overriding the underlying operating improvement the business continues to produce in constant-currency terms.

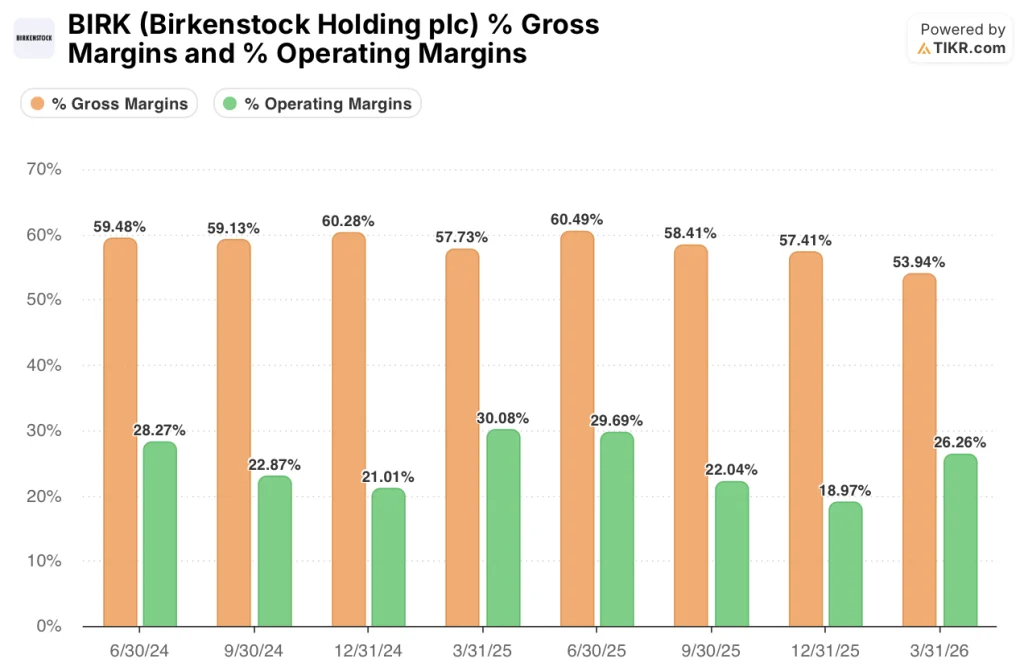

Gross margin peaked at 60% in Q1 FY2026, pulled back to 58% in Q2 FY2025, and compressed to 54% in the most recent quarter, a trajectory that reflects the full weight of dollar depreciation flowing through reported figures.

Adjusted gross margin of 55% was down 310 basis points YoY; Krolo attributed 230 basis points to FX and 90 basis points to U.S. tariffs on the Q2 earnings call, noting that on a currency and tariff-neutral basis, gross margin was actually up 10 basis points year over year.

Operating margin fell to 26% in Q2 FY2026 from 30% in the same quarter a year earlier, consistent with the gross margin compression pattern.

Adjusted EBITDA margin of 32% was down 270 basis points YoY, but excluding FX and tariff impacts, the margin would have been up 60 basis points to approximately 35%, per Krolo on the Q2 earnings call.

Birkenstock guided for adjusted gross margin of 57%–57.5% for the full fiscal year, inclusive of a combined 200 basis points of pressure from FX and tariffs, with tariff headwinds expected at approximately 100 basis points in Q3 and 50 basis points in Q4.

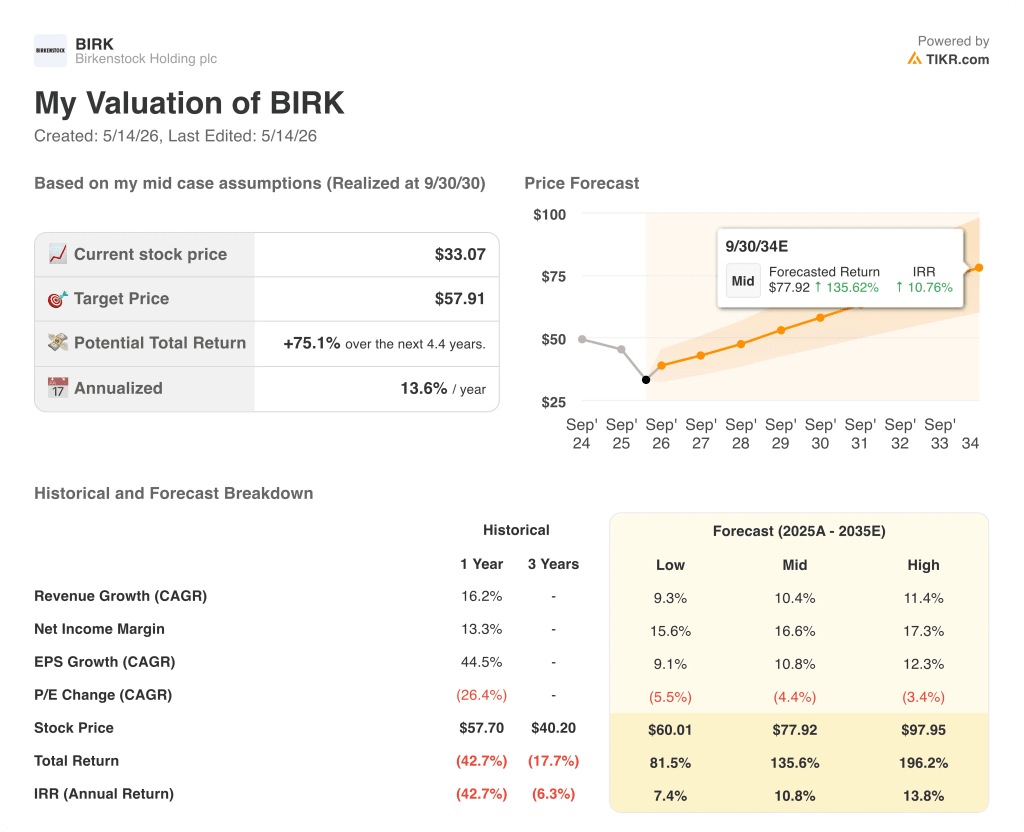

What Does the Valuation Model Say?

TIKR’s model sets a price target of €51.96 on Birkenstock stock, implying approximately 75% upside from the current price of €30.67 over roughly 4.4 years.

The mid-case assumes revenue growth of 10.4% CAGR and a net income margin of 16.6%, with EPS growing at a 10.8% CAGR — assumptions the Q2 result does not obviously invalidate, given that constant-currency momentum held within guidance range.

The model also embeds annual P/E compression of 4.4% in the mid-case, meaning the path to €51.96 depends on earnings growth running fast enough to outpace a multiple that is contracting in the base scenario.

Q2 sharpens both sides of the risk/reward: reported EPS looks soft due to transitory noncash charges, but constant-currency fundamentals and reaffirmed full-year guidance keep the core investment case intact.

With tariff and FX headwinds now quantified and embedded in guidance, Birkenstock stock’s investment case is broadly unchanged from a quarter ago — the business is executing at plan, and the discount to the TIKR model target remains as wide as it has been.

Birkenstock confirmed constant-currency momentum is on track, but FX translation and escalating tariffs continue to obscure the underlying result in reported numbers, and that gap needs to close for the re-rating to materialize.

What Has to Go Right

- Constant-currency revenue growth must hold within the 13%–15% guided range in Q3 and Q4, a target management says is achievable even if current external headwinds persist

- FX headwinds are expected to ease to approximately 200 basis points in Q3 and become largely neutral in Q4, which would allow reported figures to more accurately reflect constant-currency performance

- The €30M IEEPA tariff refund, if received on a reasonable timeline, provides an unmodeled margin tailwind not embedded in current full-year guidance

What Could Still Go Wrong

- EMEA carries an identified €10M–€12M revenue risk tied to the Middle East conflict, with the indirect consumer sentiment impact across Europe remaining difficult to forecast beyond the current quarter

- Tariffs are now running at just over 20% following the U.S. Supreme Court ruling, up from just over 15% post-EU agreement, and any further escalation could push gross margin below the 57%–57.5% full-year target

- Recurring finance costs of €18M–€20M per quarter in H2 are a structural drag on adjusted net profit, compounding the €27M FX hit already absorbed in Q2

- B2B outpacing D2C in H1 could dilute margin mix if the trend persists into the DTC-heavy Q3 and Q4 periods that management itself flagged as most exposed to EMEA headwinds

Should You Invest in Birkenstock Holding plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Birkenstock Holding plc stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Birkenstock Holding plc alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze BIRK stock on TIKR for Free →