Key Stats for Bank of America Stock

- 52-Week Range: $42.35 to $57.55

- Current Price: $50.78

- Street Mean Target: ~$63

- TIKR Target Price (Mid): ~$75

- TIKR Annualized IRR (Mid): ~9% per year

- Q1 2026 Net Income: $8.6B (up 17% YoY)

- Q1 2026 EPS: $1.11 (up 25% YoY)

- Q1 2026 Net Interest Income: $15.7B (up 9% YoY)

- Dividend Yield: 2.4%

Value your favorite stocks like BAC with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

How the Rate Cycle Compressed BAC’s Earnings and Why It’s Now Running the Other Way

Bank of America (BAC) is the second-largest bank in the US and one of the most interest-rate-sensitive financial institutions in the world. Recognizing sensitivity is key to understanding the stock.

When rates were near zero in 2020 and 2021, BAC deployed its enormous deposit base into long-duration bonds. When the Fed raised rates sharply in 2022 and 2023, those bonds declined in value, and BAC was earning low fixed rates on a massive portfolio while paying higher rates to retain deposits. That compressed net interest income made the earnings numbers look worse than the underlying business deserved.

That dynamic is now reversing. NII grew 9% to $15.7 billion in Q1 2026. Revenue rose 7% to $30.3 billion. Net income came in at $8.6 billion, up 17% year over year, with EPS of $1.11, representing the strongest quarterly earnings per share the bank has produced in nearly two decades. Management raised full-year NII growth guidance to 6%-8%.

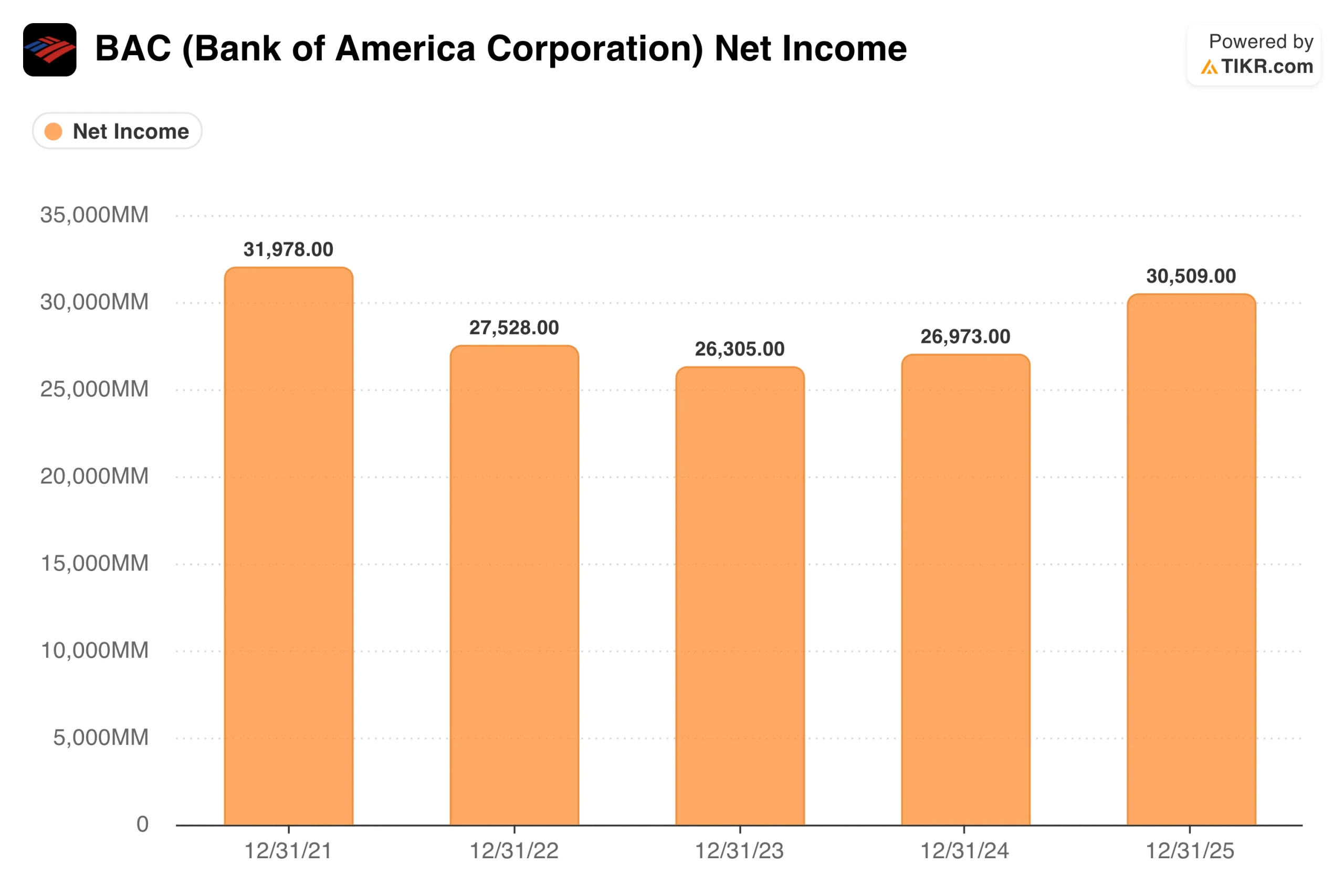

The net income chart clearly shows the rate cycle. BAC earned $31.98 billion in 2021, watched it compress to $26.3 billion in 2023 as the bond portfolio headwinds hit, and recovered to $30.5 billion in 2025. Deposits, loans, and wealth management assets all grew throughout the period. The earnings compression was a rate story, not a franchise story.

See analysts’ growth forecasts and price targets for BAC stock (It’s free!) >>>

What Analysts Think About BAC After the Q1 Beat

The Street target of around $63 implies roughly 24% upside, and consensus is broadly constructive. Q1 showed operating leverage of nearly 3%, with revenue growing faster than expenses, and credit quality remained manageable with provisions declining year over year to $1.3 billion.

BAC returned $9.3 billion to shareholders in Q1 alone, including $7.2 billion in buybacks. The 2.4% dividend yield adds an income floor that most bank peers cannot match at comparable multiples, and the 30% payout ratio leaves substantial room for continued dividend growth. At roughly 11 times forward earnings, the multiple looks conservative, given the NII expansion that is now demonstrably underway.

What the EPS Acceleration Looks Like From Here

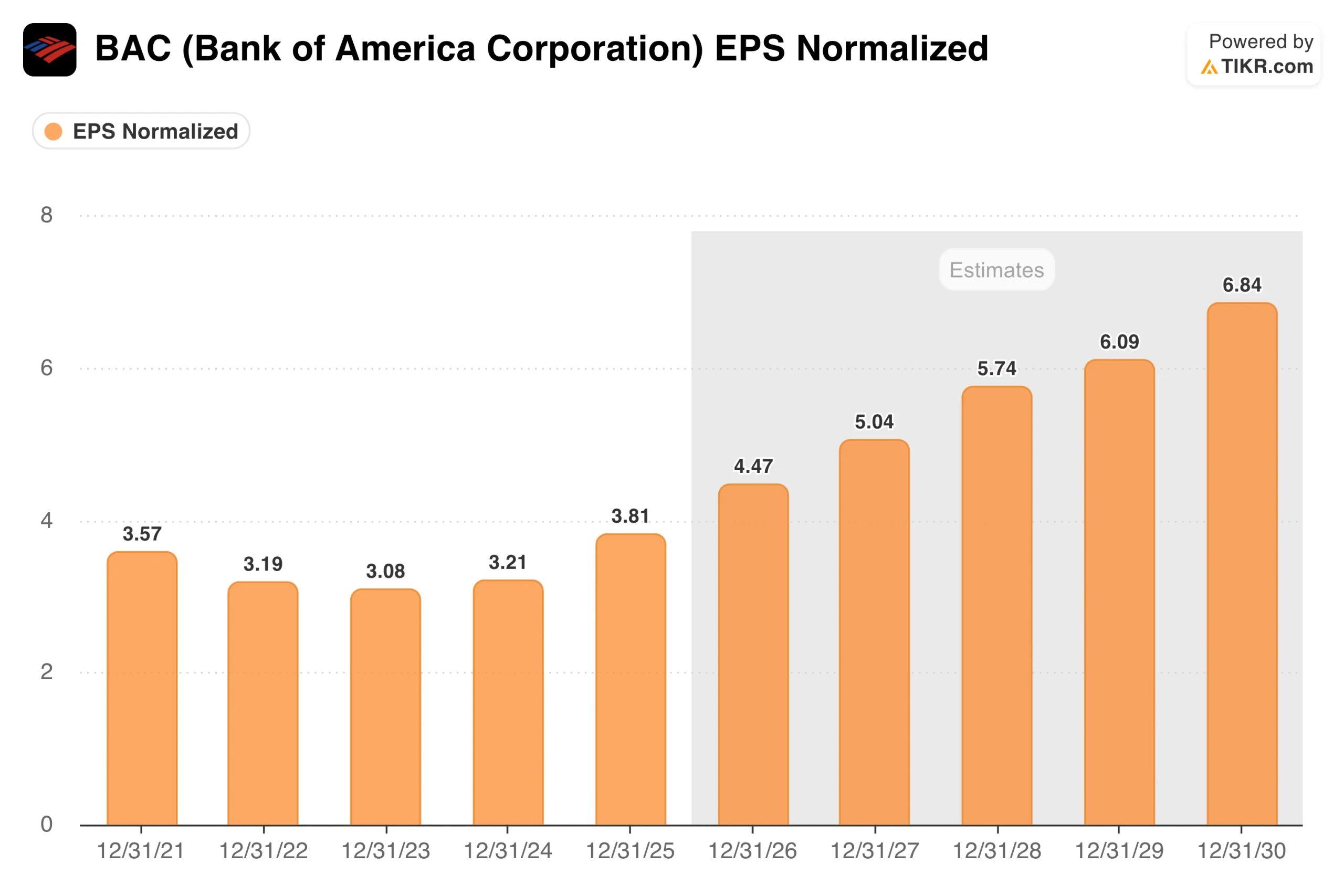

Normalized EPS bottomed at $3.08 in 2023 and has been climbing: $3.21 in 2024, $3.81 in 2025. The forward estimate for 2026 is around $4.50, the strongest full-year EPS in BAC’s recent history. Consensus then projects around $5 in 2027 and around $5.75 in 2028, a forward two-year growth rate of roughly 15%.

That is a meaningful acceleration for a bank at 11 times earnings. The drivers are the NII expansion already underway, operating leverage as expenses grow more slowly than revenue, and the continued compounding of the Merrill Lynch and Private Bank wealth management franchises, which generate relatively stable fee income across credit cycles.

Value BAC instantly (Free with TIKR) >>>

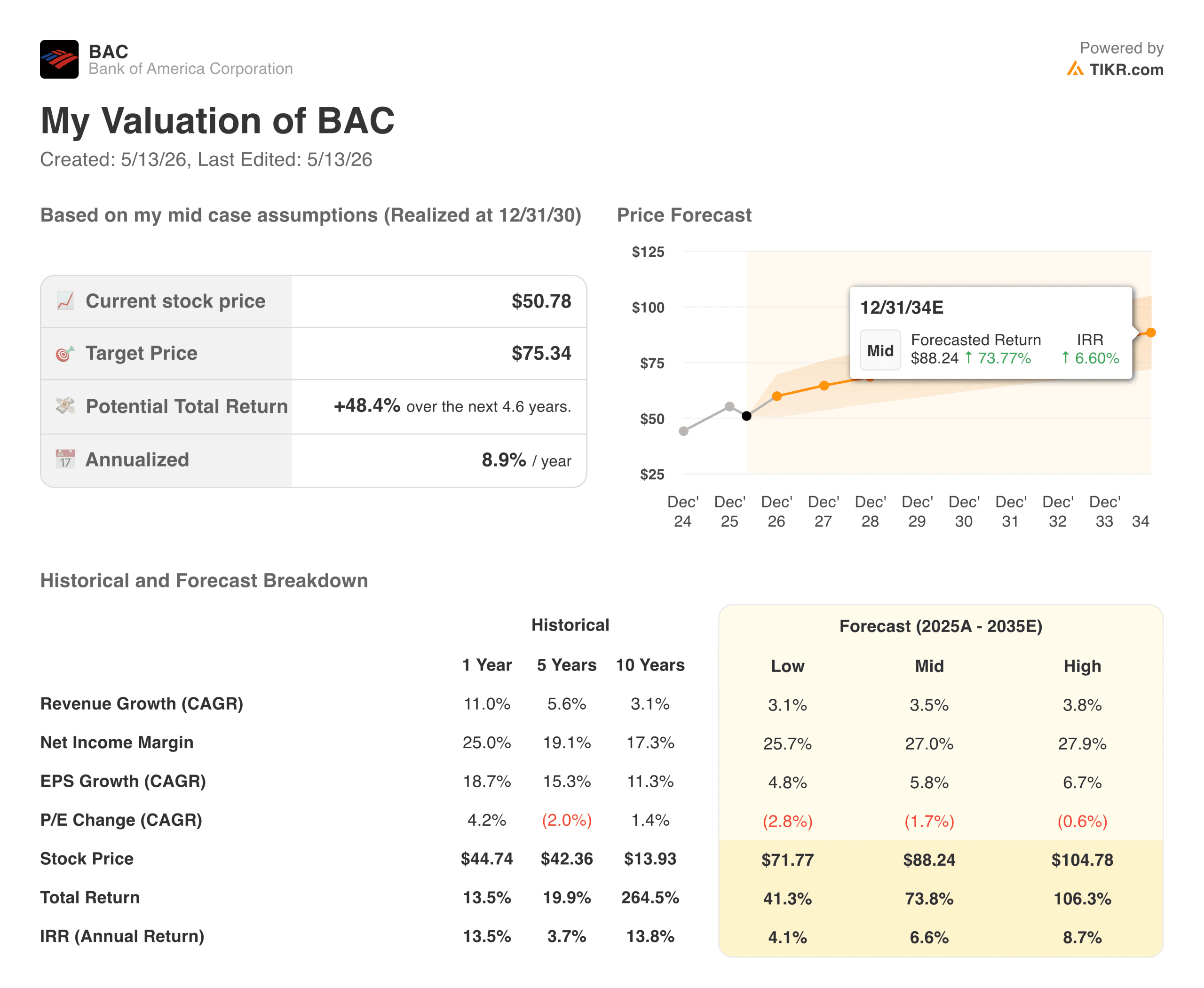

What the TIKR Model Implies at the Current Price

The TIKR model targets around $75 per share in the mid case, implying a total return of roughly 48% over about 4.6 years, or about 9% annually. The 2.4% dividend adds another 10%-11% in cumulative income over the period.

The model uses revenue growth of around 3.5% per year, a net income margin of around 27%, and EPS growth of around 6% per year. These are not aggressive assumptions. The low case targets around $72 at roughly 4% per year. The high case reaches around $105. Even the conservative scenario implies meaningful upside when the dividend is included.

The Case for BAC: NII Expansion, Scale, and Capital Returns

The NII tailwind has further to run. As more of the fixed-rate bond portfolio matures and is reinvested at current rates, net interest income continues to expand without requiring incremental risk-taking. It is time-driven earnings growth.

On top of that, the Merrill Lynch wealth management franchise manages trillions in client assets and generates fee income that is relatively rate-insensitive, compounding steadily in the background. With $3.3 trillion in assets and $2 trillion in average deposits, BAC’s scale creates operating leverage that smaller competitors cannot replicate, which is exactly what the Q1 numbers demonstrated.

The Risks: Rate Sensitivity Still Runs Both Ways

The same rate sensitivity helping BAC can hurt it if conditions shift. Management quantified this directly: a 100-basis-point decline in rates beyond the forward curve would reduce NII by around $2 billion over the next 12 months. More aggressive Fed cuts than expected would moderate the expansion thesis.

Credit quality has been cooperative, but the consumer loan book is large. If unemployment rises, charge-offs move higher quickly. And revenue growth of around 3.5% annually is the right framing for expectations. The return thesis is about EPS acceleration from NII expansion and buybacks, not a revenue inflection.

Is BAC Worth Buying at $51?

BAC posted its highest EPS in nearly two decades, raised its NII guidance, and returned over $9 billion to shareholders in one quarter. The stock is still 12% below its 52-week high.

The net income recovery from $26.3 billion in 2023 to $30.5 billion in 2025 is not a projection; it is already in the results. The EPS trajectory toward an estimated $4.50 this year and $5.75 by 2028 reflects a business whose earnings power was never as impaired as the bond portfolio narrative suggested.

The TIKR mid-case of around $75 at roughly 9% per year, plus a 2.4% dividend, is a competitive total return for one of the most durable financial franchises in the world. The Street sees $63. The model sees $75. The stock is at $51.

See analysts’ growth forecasts and price targets for BAC stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!