Key Stats for Marriott Stock

- 52-Week Range: $253 to $380

- Current Price: $350.19

- Street Mean Target: $377

- TIKR Target Price (Mid): ~$418

- TIKR Annualized IRR (Mid): ~4% per year

- Q1 2026 EPS: $2.73 (beat $2.35 estimate)

- Q1 2026 Global RevPAR Growth: ~2% YoY

- FY2026 EPS Guidance: $5.40 to $5.60

- Bonvoy Members: 237 million

Value your favorite stocks like MAR with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What the Q1 2026 Beat Revealed About Marriott’s Demand Picture

Marriott (MAR) manages and franchises over 9,200 properties with more than 1.75 million rooms across 141 countries. It does not own most of those hotels. Instead, it collects fees tied to revenue and bookings while leaving the capital investment and operating risk to property owners. That asset-light structure is why Marriott generates billions in free cash flow while carrying a relatively small balance sheet.

Q1 2026 results reinforced that the post-pandemic travel cycle has staying power. Adjusted EPS came in at $2.73 against a consensus estimate of $2.35, a meaningful beat. Global RevPAR grew roughly 2% year over year, driven by strong performance in the Middle East and Asia Pacific, as well as continued demand across the Starwood brand portfolio.

Bonvoy, Marriott’s loyalty program, now counts 237 million members, a base that drives direct bookings, reduces distribution costs, and generates co-branded credit card revenue independent of any single property’s occupancy.

Management guided full-year 2026 EPS to $5.40 to $5.60, with global RevPAR expected to grow 2% to 4%. The guidance is solid but not accelerating, which suggests where we are in the travel cycle.

See historical and forward estimates for Marriott stock (It’s free!) >>>

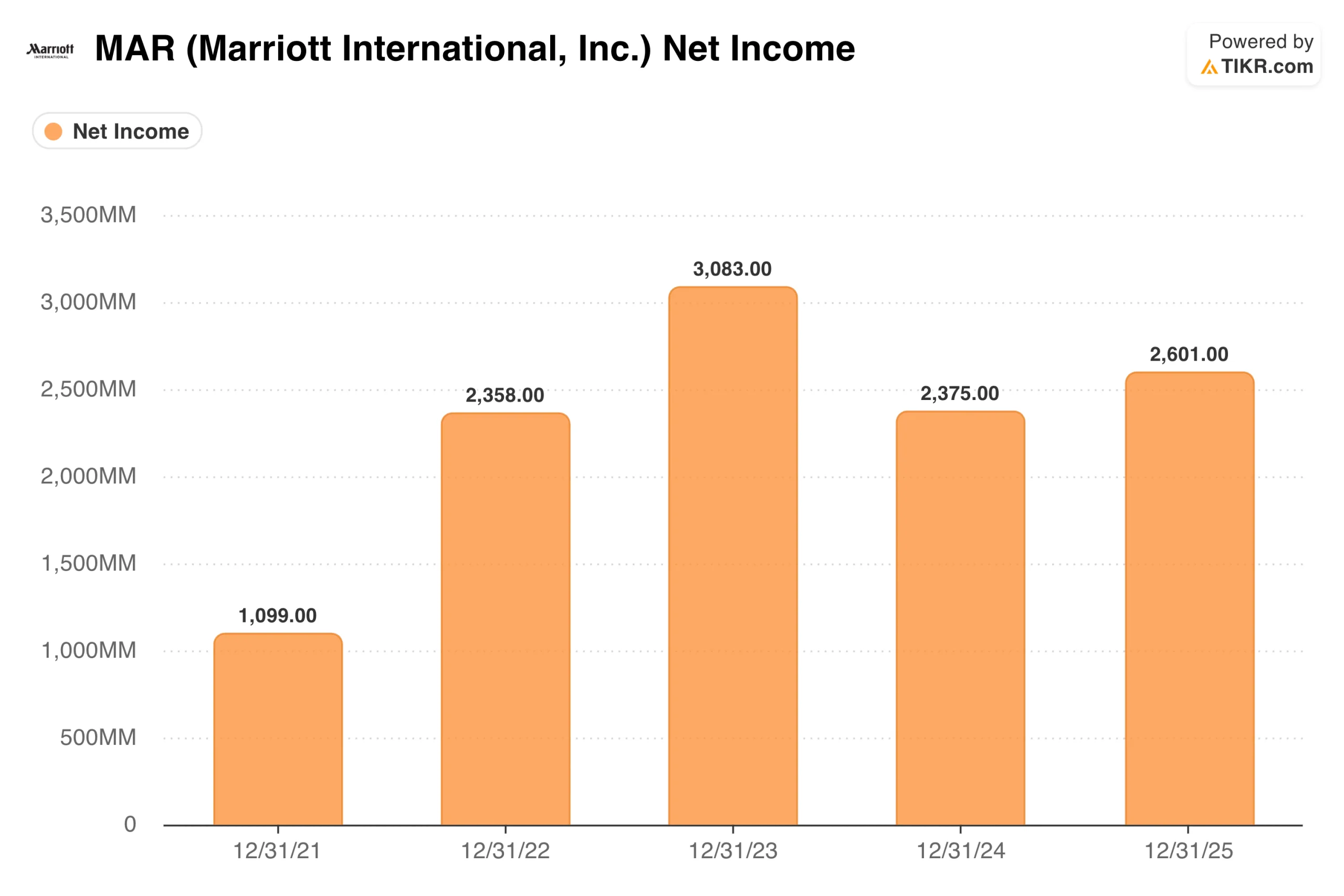

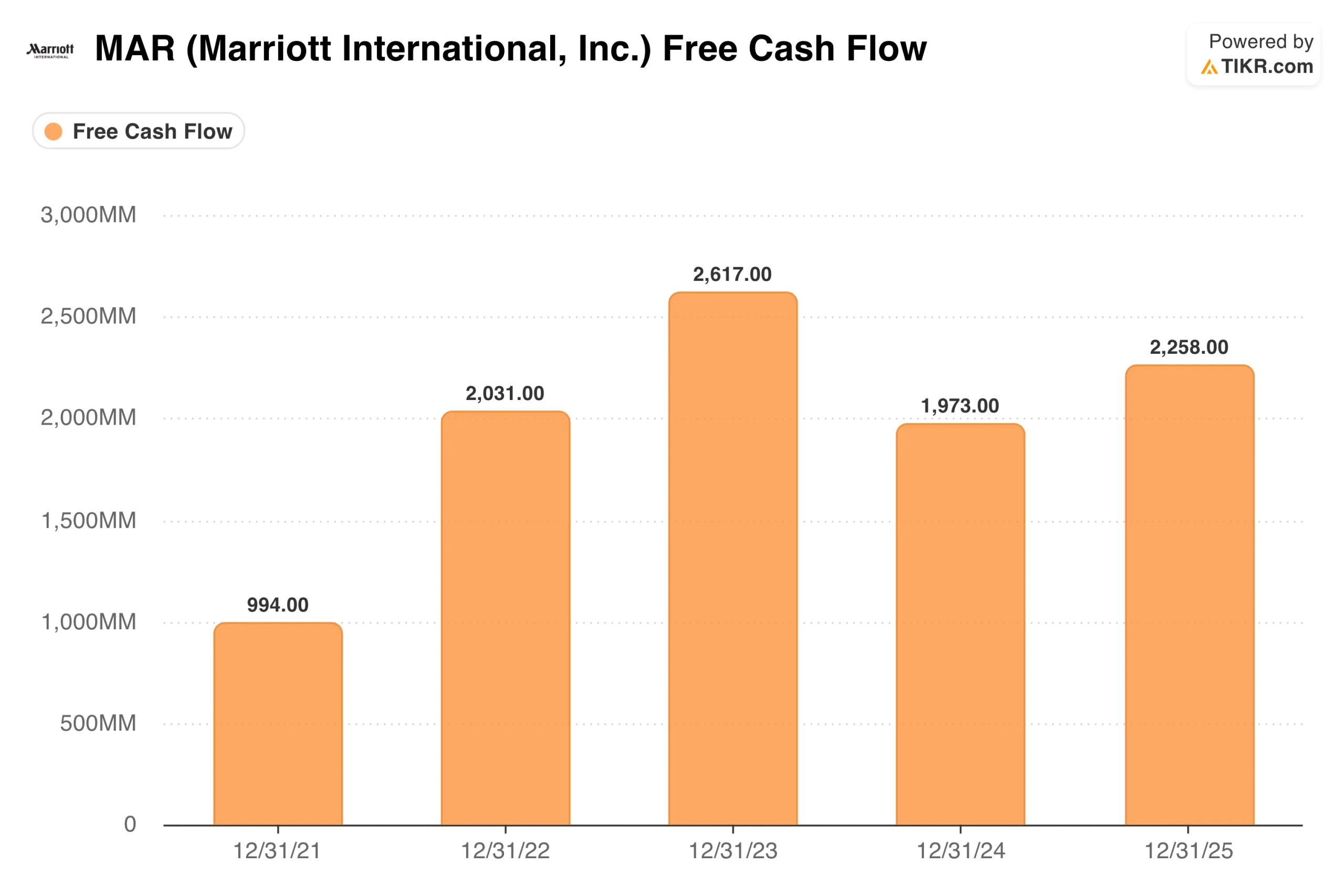

What Net Income and Free Cash Flow Say About the Business Quality

Net income recovered sharply from the pandemic, rising from $1.1 billion in 2021 to $2.4 billion in 2022, peaking at $3.1 billion in 2023 as pent-up travel demand drove exceptionally strong RevPAR growth. It dipped to $2.4 billion in 2024 before recovering to $2.6 billion in 2025.

The 2023 peak and 2024 step-back are worth understanding. The 2023 figure benefited from unusually strong normalization of post-COVID demand. The 2024 dip reflected more normalized conditions, higher technology investment, and some one-time items. Something in the $2.5-$2.7 billion range is the more honest ongoing run rate.

Free cash flow tells the same story. Marriott generated $994 million in FCF in 2021 as the business was still recovering, ramped to $2.0 billion in 2022, peaked at $2.6 billion in 2023, dipped to $2.0 billion in 2024, and recovered to $2.3 billion in 2025.

Consistently above $2 billion annually, with no meaningful capital expenditure drag because Marriott does not build hotels. That FCF gets returned to shareholders through buybacks and dividends, which is why the share count has been declining for years despite modest revenue growth.

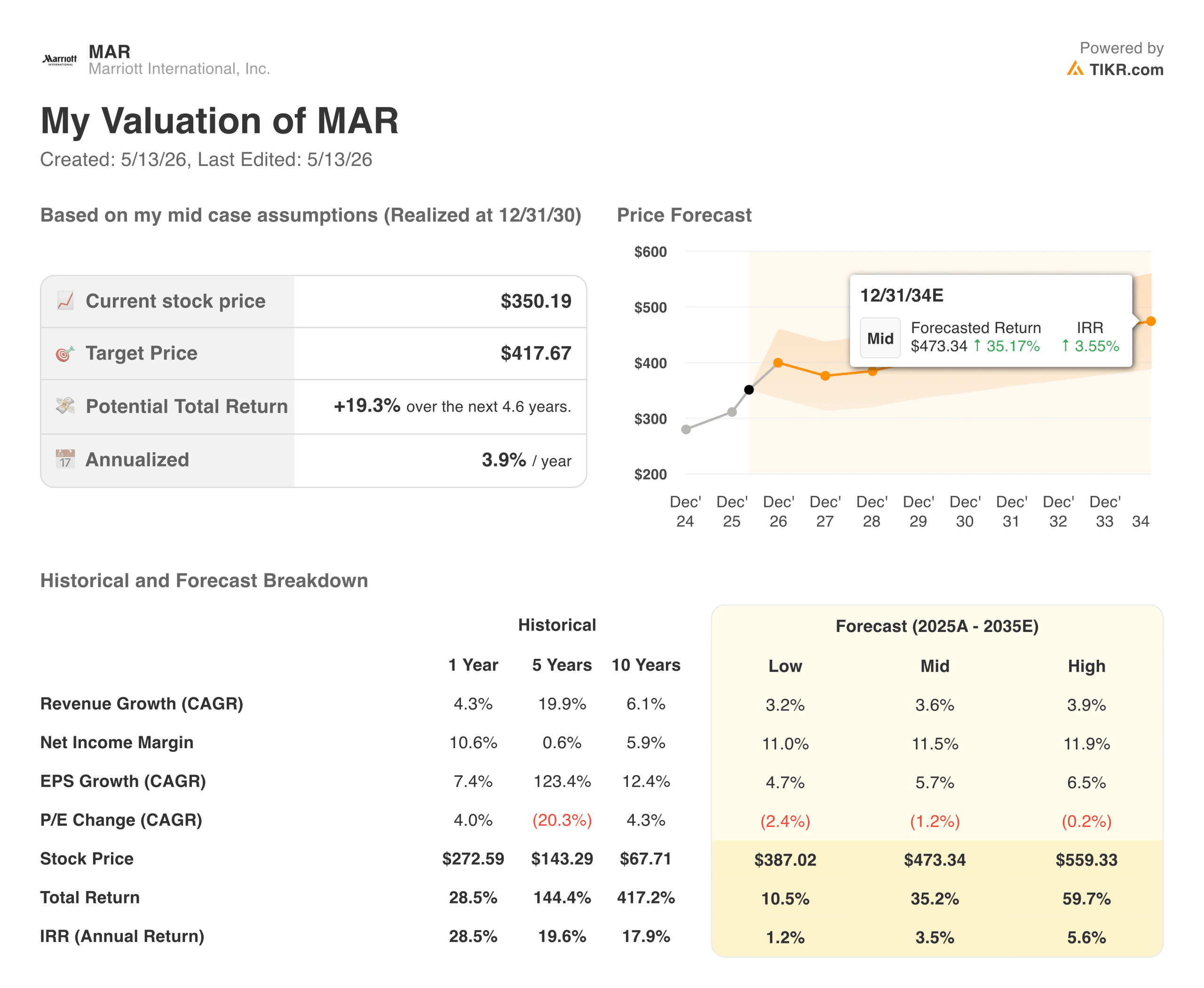

What the TIKR Model Says: An Honest Look at the Return Profile

This is where the MAR story gets more nuanced than the prior few years of strong performance might suggest.

The TIKR model targets around $418 per share in the mid case, implying a total return of roughly 19% over about 4.6 years, or about 4% annually. The model uses revenue growth of around 4% per year, net income margins of around 12%, and EPS growth of around 6%. Those are reasonable assumptions for a mature, asset-light hospitality franchise.

The challenge is that 4% per year is not a compelling standalone return, particularly for a business with real sensitivity to travel demand cycles and macroeconomic conditions. The low case, which targets around $387, barely implies any upside from the current price. The high case reaches around $559 at roughly 6% annually, which requires the full bull scenario to play out.

This is not a knock on the business. It is an honest read of what the current price implies.

See what analysts think about MAR stock right now (Free with TIKR) >>>

The Case for MAR: Brand Scale, Asset-Light FCF, and a Loyalty Moat

Marriott’s competitive position is genuinely difficult to replicate. 31 brands, spanning budget to ultra-luxury, give it pricing power across every traveler segment. The Bonvoy program’s 237 million members create a distribution advantage: direct bookings are cheaper for Marriott than third-party channels and stickier for the hotels. The asset-light model means capital requirements are minimal and FCF conversion is high. Growth comes from signing management and franchise agreements, not building hotels.

International expansion is the long-term growth lever. Marriott is meaningfully underpenetrated in markets such as China, India, and Southeast Asia compared with its US presence. As middle-class travel in those regions grows, the pipeline of new properties provides multi-year visibility into room-count growth that does not depend on RevPAR acceleration in mature markets.

The Risks: Cycle Sensitivity and a Tight Valuation

Travel demand is cyclical. Marriott’s revenue is tied to occupancy and room rates, both of which can move quickly in a downturn. The current 2% to 4% RevPAR growth guidance is solid, but if economic conditions soften, that number can turn negative quickly, and earnings follow.

The valuation leaves little margin for error. At the current price, the mid-case return is roughly 4% annually. Any meaningful shortfall in revenue growth or margin assumptions pushes the model toward the low case, where the return is barely above zero. That is not a comfortable cushion for a cyclically sensitive business that has already priced in much of the good news.

Is MAR Worth Buying at $350?

Marriott is one of the best-run businesses in global hospitality. The brand scale, Bonvoy, the asset-light model, and management’s execution record are all genuine advantages. None of that is in question.

The TIKR model is saying that the current price already reflects most of those advantages. A mid-case return of around 4% annually is what you earn for owning a great business at fair value. The high case at around 6% is more interesting, but it requires travel demand to stay resilient, international expansion to accelerate, and Bonvoy monetization to keep growing.

For investors who want exposure to a world-class hospitality franchise as a long-term core holding, MAR makes sense. For investors looking for meaningful upside from current levels, the model suggests the risk-reward is more modest than it was a year ago when the stock was trading closer to $272.

See analysts’ growth forecasts and price targets for MAR stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!