Key Stats for Upstart Stock

- 52-Week Range: $24 to $87

- Current Price: $27

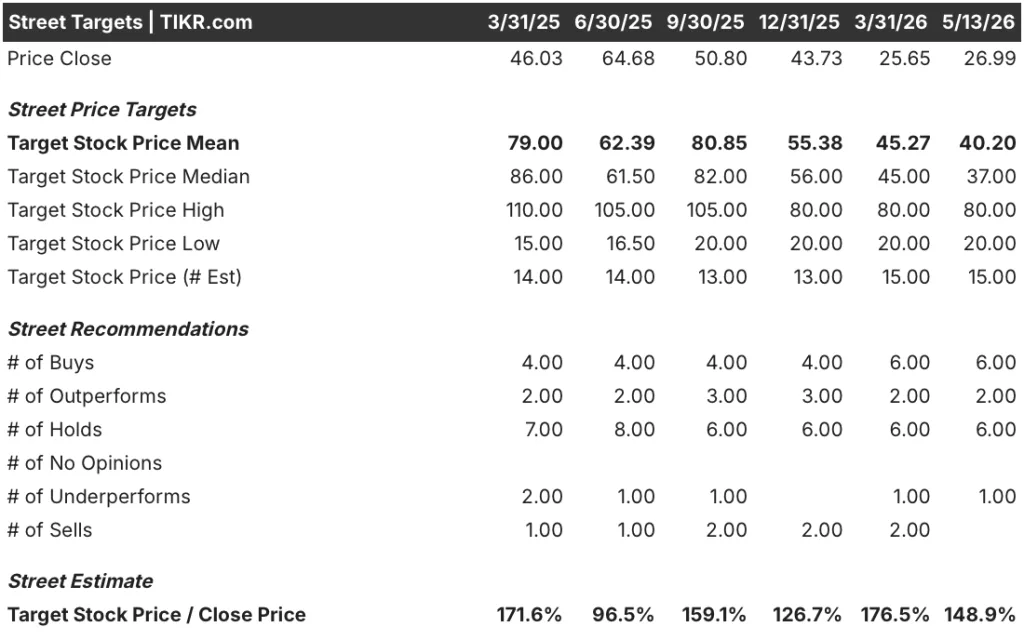

- Street Mean Target: $40

- Street High Target: $80

- Analyst Consensus: 6 Buys / 2 Outperforms / 6 Holds / 1 Underperform

- TIKR Model Target (Dec. 2030): $199

What Happened?

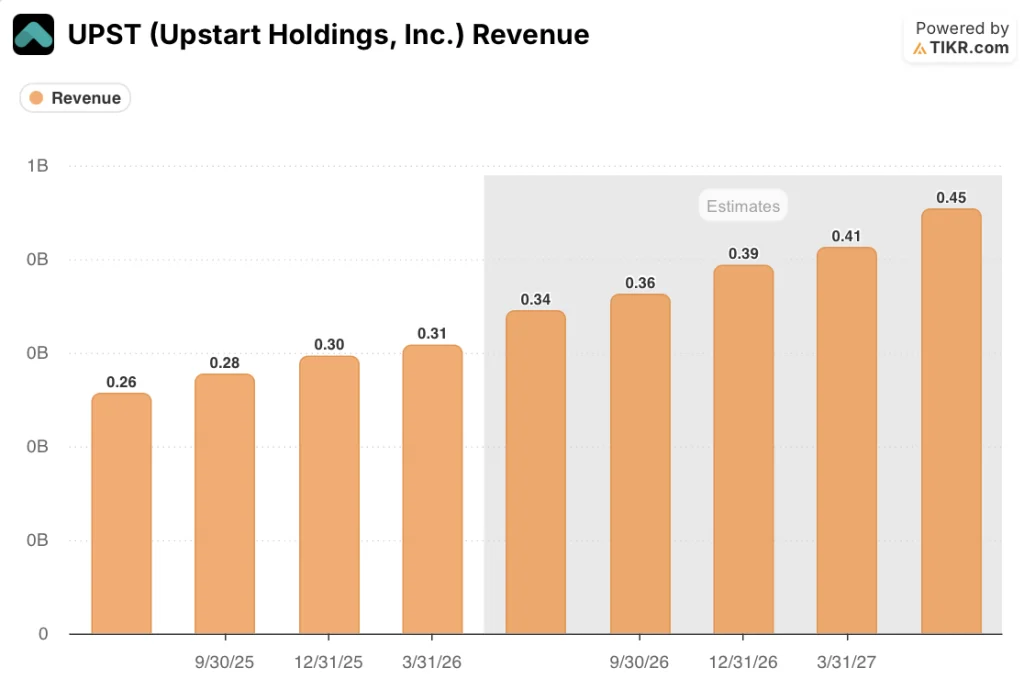

Upstart Holdings (UPST), the AI-powered lending marketplace that uses machine learning to replace traditional FICO scoring for banks and credit unions, posted first-quarter revenue of $308 million, up 44% year-over-year, as originations climbed 61% to $3.4 billion.

The results were driven by broad acceleration across every product line, with auto originations surging more than 300% year-over-year and home lending growing roughly 250%, as Upstart’s software integrations into dealership workflows and its 6-day HELOC closing process pulled volume from legacy lenders.

Loan origination volume reached 425,356 loans in the quarter, up 77% from a year earlier, a figure that reflects both the expanding active dealer network and better-than-seasonal strength in core personal loans, which held flat sequentially against a Q1 that historically sees a 10% decline.

CEO Paul Gu stated on the Q1 2026 earnings call that “originations grew 61% year-over-year and revenue grew 44%, while profit declined marginally — these are strong results and put us comfortably on track to meet our full year guidance on both the top and bottom lines.”

The company also announced in March its application for a national bank charter, a structural move designed to expand Upstart’s addressable market across all 50 states, reduce the operational costs of originating loans, and give Upstart a direct regulatory relationship as AI reshapes consumer credit over the next decade.

Funding supply reinforced the growth story: Upstart secured over $4 billion in committed capital year-to-date, including a $1.25 billion forward-flow deal with Fortress Investment Group, a $1.2 billion 24-month commitment from Centerbridge Partners, and a $1 billion agreement with Eltura Ventures and Aperture Investors.

Wall Street’s Take on UPST Stock

The Q1 beat matters less than what it confirms: Upstart’s platform is accelerating across every dimension simultaneously, and the market has not yet reconciled that trajectory with the stock’s current valuation.

UPST’s revenue grew 44.4% in Q1 2026, and consensus estimates project around 34% growth in Q2, 31% in Q3, and 33% in Q4, putting the full-year figure in line with the company’s own $1.4 billion guidance — a compounding top line backed by the $4 billion in committed capital that eliminates the funding risk bears have cited for two years.

Fourteen analysts covering Upstart stock have landed at a mean price target of $40.20 against the current price of $27, implying roughly 49% upside, with the most bullish target sitting at $80 — Wall Street is waiting for the bank charter application to clear regulatory review and for secured lending margins to improve as auto and home scale.

The spread from $20 to $80 encodes a genuine debate: the low end prices in continued macro uncertainty and execution risk on the charter, while the high end reflects the full value of a platform that could eliminate $200 million in annual frictional costs once the bank structure is operational.

The risk is macro: Upstart’s Upstart Macro Index, a proprietary measure of consumer credit health the company uses to calibrate its models, has held stable since late 2025, but any deterioration in consumer repayment patterns would compress origination volume and push the $294 million EBITDA guide out of reach.

Q2 2026 earnings will be the first test of whether origination momentum held through April and May; the specific number to watch is whether fee revenue tracks toward the around $340 million implied by the full-year guidance pace, confirming that Q1 was a platform inflection and not a one-quarter aberration.

What Does the Valuation Model Say?

The TIKR mid-case model assigns Upstart stock a target price of $159 by December 2030, built on a 21.2% revenue CAGR assumption through 2035 and a net income margin of 38.4%, an outcome that the company’s own 3-year guidance of around 35% annual growth suggests is actually conservative in the near term.

At $26.99 against a mid-case intrinsic value of $159, Upstart stock appears deeply undervalued: the current price implies the platform compounds revenue at less than half the rate management has guided to and credit markets are actively funding.

The central question is not whether Upstart grows, but whether the bank charter, margin expansion in auto and home, and core personal loan reacceleration arrive on the timeline the model requires.

What Has to Go Right

- The bank charter clears OCC and FDIC review, unlocking the full 50-state addressable market and removing the estimated $200 million in annual frictional origination costs tied to managing a network of intermediary financial institutions.

- Auto contribution margins improve materially in the second half of 2026, as management guided, driven by higher sell-through of loans to third parties and continued automation reducing per-loan processing costs.

- Core personal loan originations reaccelerate through 2026 off the stronger-than-seasonal Q1 base, where volume held flat sequentially against a historical 10% decline.

- The $4 billion in committed capital, including Centerbridge’s 24-month deal and Fortress’s 15-month renewal, continues to absorb origination volume without balance sheet expansion, keeping the capital-efficient model intact.

- Cash Line, Upstart’s first revolving credit product launched in early Q2, gains traction with the 20-million-plus consumers already in the database, adding a durable recurring revenue stream the current multiple does not price in.

What Could Go Wrong

- Consumer credit quality softens as macro pressures compress household budgets, causing the Upstart Macro Index to deteriorate and triggering a model-driven reduction in approval rates that slows origination volume below the $1.4 billion revenue guide.

- The bank charter application faces regulatory delay beyond 2026, deferring the $200 million in cost savings and TAM expansion the bull case assigns to the near-term period.

- Auto and home contribution margins improve more slowly than the H2 2026 guidance implies, as dealer software adoption and HELOC automation remain earlier-stage than the sequential growth rates suggest.

- The $80 high-end analyst target requires execution on multiple fronts simultaneously; any single miss, whether charter timing, macro deterioration, or margin stagnation, compresses the story back toward the $20 low-end target.

Should You Invest in Upstart Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Upstart Holdings, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Upstart Holdings, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UPST stock on TIKR for Free →