Key Stats for Regeneron Stock

- Current Price: $716.80

- Street Target (Mean): ~$875

- Target Price (Mid): ~$1,184

- Potential Total Return (Mid): ~65%

- Annualized IRR (Mid): ~11% / year

- Q1 2026 Earnings Reaction: +3.02% (4/29/26)

- Max Drawdown: -21.43% (6/5/25)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Regeneron Pharmaceuticals (REGN) presented at the Bank of America Global Healthcare Conference on May 12, with Ryan Crowe, Senior Vice President of Investor Relations, and Marion McCourt, Executive Vice President of Commercial, on stage. They addressed three things investors have been waiting on: which products fall inside the new Most Favored Nation pricing agreement, how EYLEA HD is holding up against biosimilar competition, and how close the fianlimab melanoma readout actually is.

The stock sits at $716.80, roughly 7% below its end-of-2025 close of $771.87 and about $105 below its 52-week high of $821.11. The core debate is whether the MFN deal creates a pricing ceiling on DUPIXENT, Regeneron’s largest revenue driver, or whether management’s disclosures at this conference clarify and remove that overhang. Crowe’s answer turned on a structural detail the market has largely overlooked.

The MFN Deal: What’s In, What’s Out

The most consequential disclosure at the conference was the product scope of Regeneron’s MFN agreement with the U.S. government. Crowe explained that the deal covers products wholly owned by Regeneron in the U.S. In exchange, the company receives relief from future government pricing mandates and tariff protection through at least January 2029.

EYLEA and EYLEA HD are wholly owned by Regeneron in the U.S. and fall inside the agreement. DUPIXENT, co-commercialized with Sanofi, does not. Crowe was careful about naming specific products given confidentiality obligations, but his framing was unambiguous: “We wholly own EYLEA and EYLEA HD in the U.S., but we do not wholly own DUPIXENT in the U.S.”

For investors discounting REGN on fears of near-term government price caps on DUPIXENT, that distinction matters. DUPIXENT is running at roughly a $20 billion annual global revenue rate, according to McCourt. Any future pricing constraint on that franchise requires a separate negotiation involving Sanofi, not the deal Regeneron has already signed.

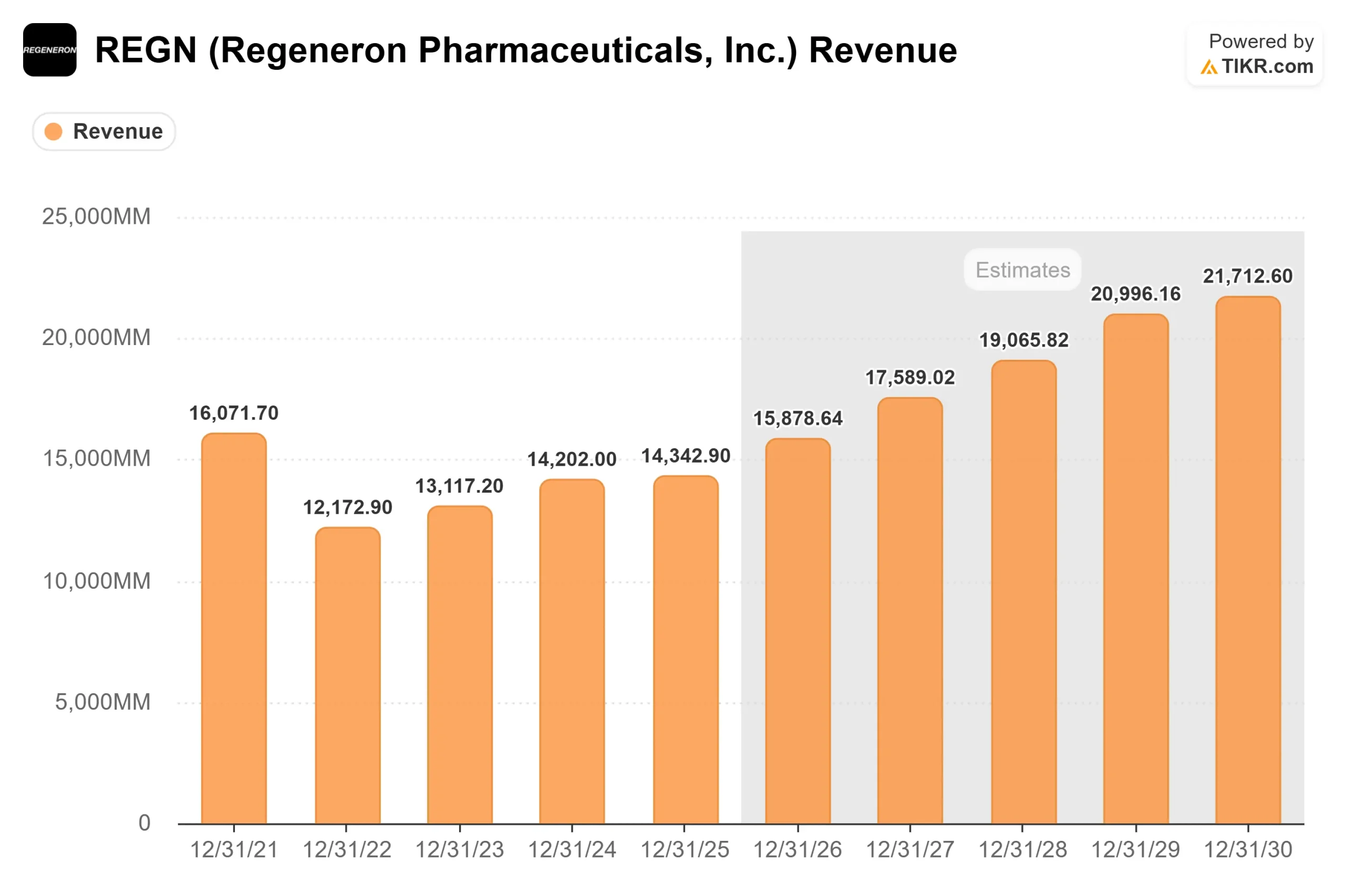

The timing compounds the significance. The Sanofi development balance, a profit-sharing obligation that has compressed Regeneron’s collaboration revenue for years, is expected to clear around Q3 2026. Once it does, Regeneron receives its full share of DUPIXENT profits unencumbered. TIKR’s forward estimates show 2026E normalized EPS of $46.50 accelerating to $53.86 in 2027, a jump of around 16%. That step-up is driven by this profit-share event, not new pipeline approvals.

See historical and forward estimates for Regeneron stock (It’s free!) >>>

DUPIXENT: Nine Indications, One Competitive Moat

DUPIXENT has 1.4 million patients on therapy worldwide across nine U.S. indications. Four of them, including atopic dermatitis, asthma, nasal polyps, and eosinophilic esophagitis, are individually blockbuster-scale. The remaining five, including COPD, bullous pemphigoid, prurigo nodularis, and chronic spontaneous urticaria, are still building prescription volume.

The COPD launch is generating the sharpest physician interest. DUPIXENT became the first biologic ever approved for COPD when the FDA cleared it in September 2024, targeting patients with elevated blood eosinophils, a marker of type 2 inflammation. In the Phase 3 NOTUS trial, the drug reduced moderate or severe COPD exacerbations by 34% versus placebo and improved lung function by approximately 139 mL in FEV1 (forced expiratory volume in one second, the clinical gold standard for measuring lung function).

Crowe sharpened the competitive picture at the conference: the only other biologic in the COPD market “has never demonstrated any lung function improvement, whereas DUPIXENT in its pivotal studies demonstrated approximately 80 mL improvement in FEV1.” Patients are also reducing or eliminating supplemental oxygen reliance, according to both McCourt and Crowe.

The competitive moat is biological, not just commercial. DUPIXENT targets the IL-4 receptor, which sits at the top of the type 2 inflammatory cascade. Oral therapies for atopic dermatitis work further downstream, which led Crowe to conclude they are “unlikely to outperform on skin clearance or itch.” Even in Regeneron’s most established indication, McCourt noted that penetration among treatable atopic dermatitis patients remains only around the high-teens percentage range, leaving a long commercial runway.

EYLEA HD: Franchise Transition on Track

Twelve months ago, the bear case held that biosimilar pressure on EYLEA 2mg would erode the retinal franchise faster than EYLEA HD (aflibercept 8 mg, the higher-dose next-generation formulation) could compensate. The current data doesn’t support that. Per TIKR’s segment data, EYLEA HD generated $1,636.90 million in 2025, up 36% from $1,201.10 million in 2024, and now represents approximately half of the combined U.S. anti-VEGF franchise revenue, according to McCourt at the conference.

The FDA expanded EYLEA HD’s label in November 2025, adding Q4 weekly dosing, the retinal vein occlusion indication, and dosing durability extending to 20 weeks, giving physicians the broadest dosing flexibility of any product in the category. Management guided Q2 2026 EYLEA HD demand growth at approximately 10%, consistent with Q1, while EYLEA 2mg demand was guided to decline mid-to-high teens as biosimilar substitution continues. McCourt also noted that approximately 95% of EYLEA 2mg usage is via prefilled syringe, framing the pending EYLEA HD prefilled syringe approval as an incremental positive for the franchise rather than a prerequisite for continued growth.

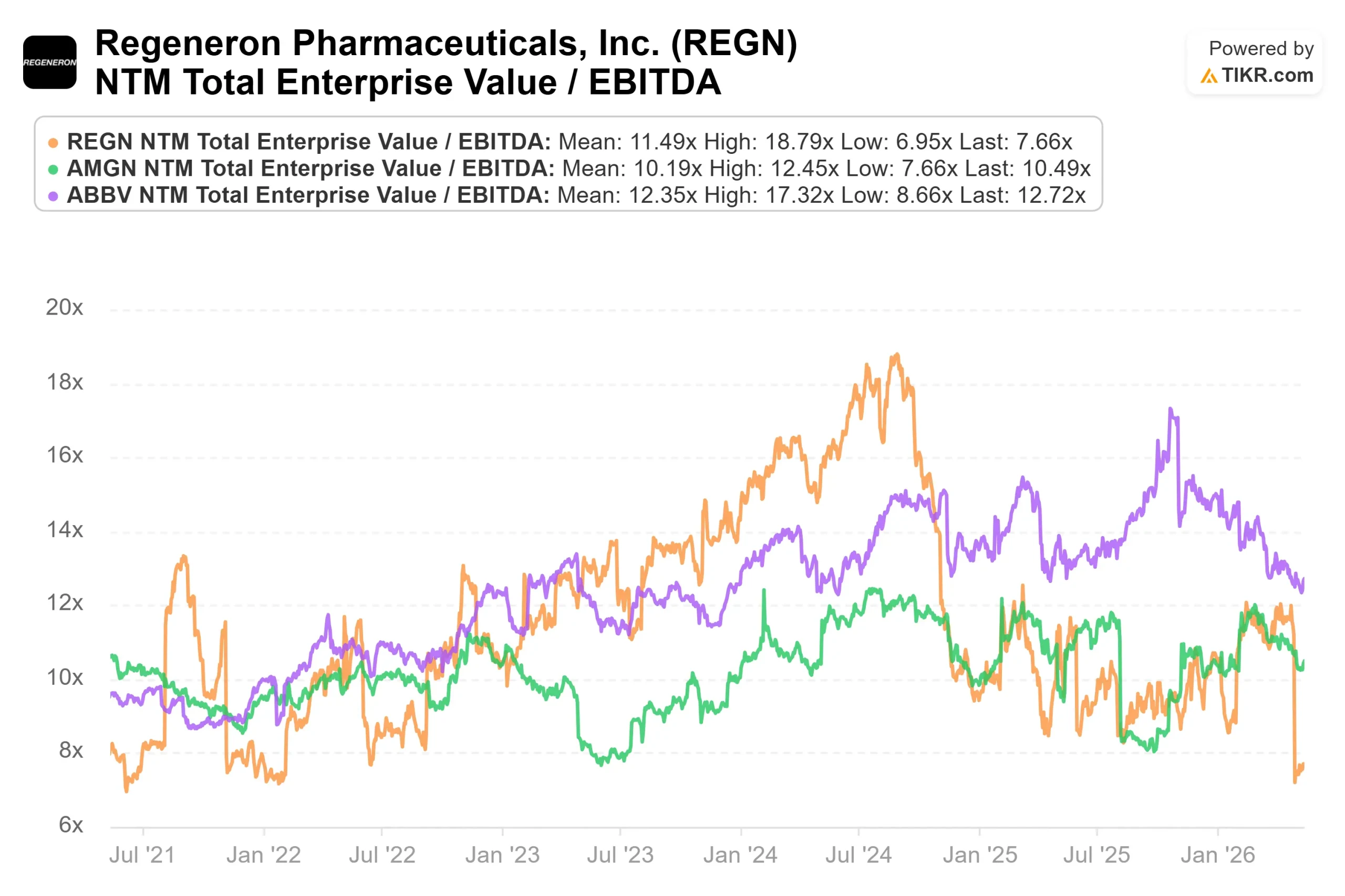

On valuation multiples, REGN trades at an NTM EV/EBITDA of 7.66x per TIKR, compared to AbbVie at 12.72x and Amgen at 10.49x. REGN carries a net cash position of approximately $15.8 billion per TIKR’s capital structure data, while both peers carry substantial net debt. The discount to peers reflects fianlimab uncertainty more than any structural weakness in the underlying business.

Fianlimab: The Readout That Defines the Rest of 2026

The most binary near-term event for REGN is the Phase 3 result from fianlimab plus cemiplimab (Libtayo) versus pembrolizumab (Keytruda) in first-line metastatic melanoma. Regeneron confirmed on April 29 it expects data in Q2 2026, and Crowe at the conference described the readout as fast approaching.

Crowe placed the global metastatic melanoma market at $2 billion to $3 billion. Fianlimab targets the LAG-3 receptor (lymphocyte activation gene 3, an immune checkpoint that suppresses T-cell activity against tumors). The only currently approved LAG-3 combination is Bristol Myers Squibb’s Opdualag, which posted a median progression-free survival of around 10 months and a complete response rate of roughly 12% to 13% in its pivotal trial, according to Crowe. The CTLA-4 plus PD-1 combination set the highest efficacy bar in this setting at 11.7 months median PFS, though it carries significant toxicity.

Regeneron’s Phase 1 data across three independent cohorts showed a pooled median PFS of approximately 24 months and a complete response rate of 25%, according to Crowe. A Phase 3 result that confirms even directional superiority over Opdualag would likely represent a best-in-class profile in a market where the incumbent bar is not especially high.

Two caveats matter going into the readout. First, fianlimab failed to advance to Phase 3 in non-small cell lung cancer, with Phase 2 data not supporting continued development, as Regeneron disclosed in its Q1 2026 earnings release. Second, Crowe confirmed the melanoma Phase 3 protocol was amended in late 2025 after PFS event accumulation ran slower than expected: “We were beginning to get concerned about when exactly the readout would occur,” leading to expanding the contributing patient population while keeping the required event threshold unchanged and requiring at least six months of follow-up for all patients. The amendment was approved by global regulators and became public in April 2026.

The adjuvant melanoma trial passed its first interim analysis, with the Independent Data Monitoring Committee recommending continuation. A second interim is expected in early H2 2026. Crowe was direct that the adjuvant setting carries a higher risk, noting Opdualag generated a hazard ratio of 1.01 versus nivolumab monotherapy in adjuvant melanoma, meaning effectively no benefit, despite winning in advanced disease.

See how Regeneron performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price (model entry): $719.88

- Target Price (Mid): ~$1,184

- Potential Total Return: ~65%

- Annualized IRR: ~11% / year

See analysts’ growth forecasts and price targets for Regeneron stock (It’s free!) >>>

The TIKR mid-case model projects approximately $1,184 as the target price from a $719.88 entry, implying around 65% total return and an annualized return of approximately 11% per year. The model runs through 12/31/30 and is built on two revenue CAGR drivers: DUPIXENT’s continued global expansion across nine indications, and EYLEA HD’s displacement of EYLEA 2mg in the U.S. retinal market. The net income margin assumption of approximately 37% reflects the Sanofi development balance clearing mid-2026. The primary risk is DUPIXENT pricing pressure if the MFN framework eventually expands to cover alliance products, a scenario that falls largely beyond the 2030 model horizon.

Free cash flow supports the thesis. TIKR estimates show 2025A FCF of $4,080.50 million growing to approximately $5.2 billion in 2026, driven by the same collaboration revenue unlocking event.

The 30 Street analysts covering REGN as of May 13 break down as 18 Buys, 4 Outperforms, 7 Holds, 1 Underperform, and 0 Sells, per TIKR’s Street Targets data. The mean price target of approximately $875 implies roughly 22% upside from current levels a gap that reflects how much of the pipeline the Street has already begun pricing in, while fianlimab uncertainty keeps a ceiling on consensus.

Conclusion

The fianlimab metastatic melanoma readout is the event that will move this stock in the next several weeks. Watch median PFS and complete response rate. A median PFS materially above Opdualag’s 10 months with a complete response rate near 20% would establish a best-in-class profile and likely force a rerating. A result that merely matches Opdualag would raise questions about the commercial opportunity, even if it leads to an eventual FDA filing.

The base business is in better shape than the stock price reflects. DUPIXENT sits outside the current MFN agreement, EYLEA HD is ahead of its transition targets, and the Sanofi development balance clearing in Q3 is a hard-dated earnings catalyst. Whether the market rewards all of that now, or waits for the melanoma data, will be answered within weeks.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Regeneron?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Regeneron, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Regeneron alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Regeneron on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!