Key Stats

- Current price: ~$87 (May 14, 2026)

- Q1 2026 total revenue: $1.1B (+17% YoY)

- Q1 2026 adjusted EBITDA: $105M (+44% YoY)

- Q1 2026 adjusted EPS: ($0.11), improved from ($0.24) in Q1 2025

- 2026 season: 92% booked, $6.2B in advanced bookings (+13% YoY)

- 2027 season: 38% booked, $3.4B in advanced bookings (+31% vs. same point last year)

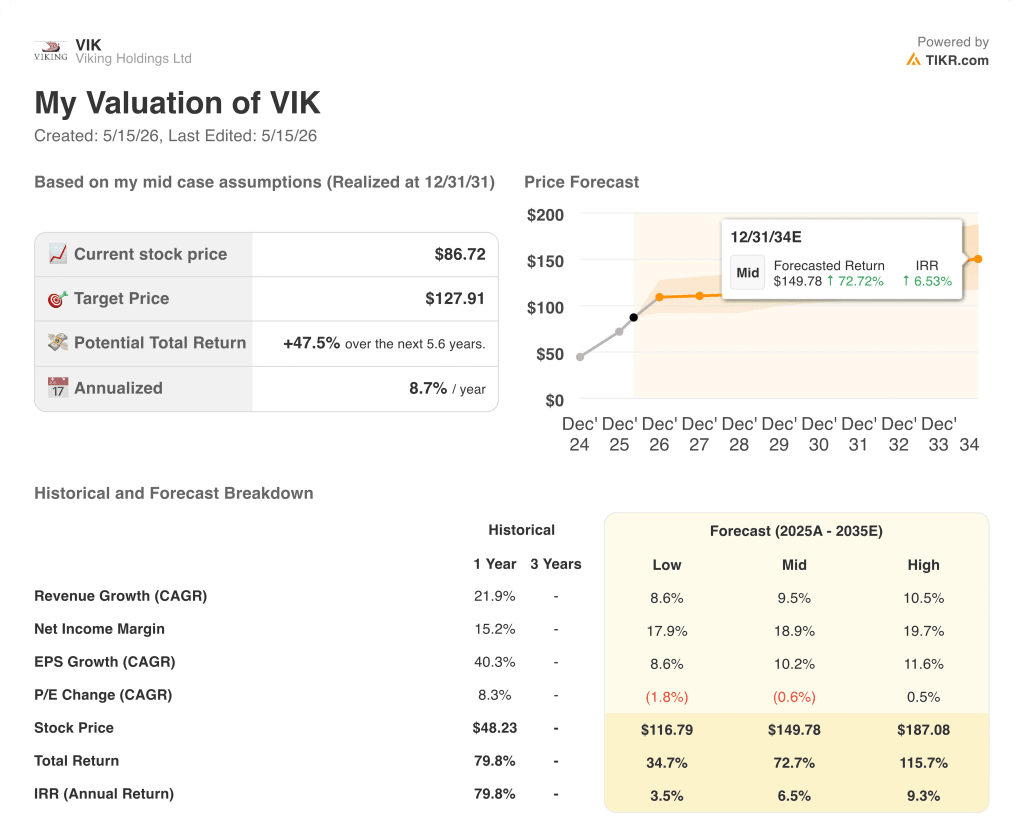

- TIKR model price target (mid-case): ~$128

- Implied upside: ~47%

Viking Holdings Q1 2026 Earnings: Revenue Tops $1 Billion as Demand Proves Resilient

Viking Holdings stock (VIK) opened its 2026 fiscal year with Q1 revenue crossing $1.1B, up 17% year-over-year, as the cruise operator delivered its first quarterly result under new CEO Leah Talactac.

Adjusted EBITDA reached $105M, a 44% improvement over Q1 2025, according to CFO Linh Banh on the Q1 2026 earnings call.

Adjusted gross margin came in at $717M, up 17% year-over-year, as capacity growth and higher revenue per passenger cruise day (PCD) drove the headline.

Net yield for the consolidated business was $596, up 10% versus the same quarter last year, according to Banh on the Q1 earnings call.

The net loss for the quarter was $54M, an improvement of more than $51M from Q1 2025, reflecting the inherent seasonality of the business, with Q1 historically being the weakest quarter in Viking’s fiscal year.

Ocean capacity grew 10% year-over-year following the delivery of the Viking Vesta in July 2025, with occupancy at 95% and Ocean net yield at $527, up 6% versus the prior-year period, according to Banh.

River capacity declined 8% year-over-year as the company deliberately removed lower-yielding winter capacity in Europe, while adding higher-yielding itineraries in Egypt and Vietnam; River net yield jumped to $761, up 28% year-over-year.

Vessel expenses, excluding fuel per capacity PCD, rose 11% year-over-year in Q1, driven by repair and maintenance costs, which Banh noted vary between quarters depending on maintenance schedules.

With 2026 largely sold, Viking Holdings stock’s forward visibility depends heavily on the 2027 booking curve: as of May 3, 2026, the 2027 season was 38% booked with capacity growing 15%, and advanced bookings 31% ahead of where the 2026 season stood at the same point in 2025.

Ocean 2027 bookings are 46% sold with rates at $882 per PCD, compared to $786 for the 2026 season at the same point in 2025; River 2027 bookings are 26% sold with rates averaging $1,108, up from $992 for the prior year’s equivalent stage, according to Tor Hagen, Executive Chairman, on the Q1 earnings call.

The company noted a brief softening in River bookings for 2026 following recent macroeconomic developments, but Talactac confirmed on the earnings call that demand rebounded after the company deployed targeted direct marketing, with cancellations remaining within historical averages.

Fuel cost exposure was flagged as a developing headwind: River operations are largely covered by fixed-price contracts set in 2025, but Ocean has greater sensitivity to market movements; Talactac noted that fuel represented approximately 4% of adjusted gross margin in 2025, limiting overall exposure.

Net leverage also improved from 1.1x as of December 31, 2025, to 1x as of March 31, 2026.

A leadership transition was also formalized during the quarter: Hagen stepped into the Executive Chairman role, Talactac was appointed CEO after nearly 20 years with the company, and Banh was named CFO.

Viking Holdings Stock Financials: Margins Compressed Sequentially but Recovery Trend Intact

The income statement for Viking Holdings stock shows a business with a clear seasonal rhythm and a multi-quarter margin recovery that Q4 2025 confirmed before the expected Q1 step-down.

Revenue followed the seasonal pattern, peaking at $2.0B in Q3 2025 before declining to $1.7B in Q4 2025 and $1.1B in Q1 2026.

Gross margin compressed from 46% in Q3 2025 and Q4 2025 to 34% in Q1 2026, with the sequential drop driven by the lower-revenue off-season quarter, not a structural cost shift.

Operating income fell to $12M in Q1 2026, down sharply from $360M in Q4 2025, with operating margin at 1%, consistent with Q1’s historically thin-margin profile.

The YoY operating income trend is the more relevant measure here: Q1 2026’s $12M compares to a Q1 2025 operating loss of ($9M), a swing of more than $21M that reflects the compounding effect of revenue growth on a largely fixed cost base.

Gross profit grew 19% year-over-year in Q1 2026, from $302M to $360M, tracking ahead of revenue growth and indicating that the higher-yielding itinerary mix in Egypt and Vietnam is beginning to show at the margin line.

What Does the Valuation Model Say?

The TIKR mid-case model sets a price target of ~$128 for Viking Holdings stock, implying approximately 47% total upside from the current price of ~$87 over the next 5.6 years.

The mid-case assumes a revenue CAGR of 9.5% and a net income margin of 19%, the latter representing a meaningful step up from the 15% net income margin recorded over the trailing year.

Q1’s 44% EBITDA growth and the 31% advance in 2027 bookings relative to the same point in 2025 strengthen the revenue growth leg of that assumption, though fuel and SG&A headwinds will test the margin expansion path as the year progresses.

Viking Holdings stock’s investment case is modestly stronger after this report: forward visibility improved, the demand rebound after the brief Q1 softening was confirmed, and the balance sheet remains well-positioned with $4B in cash and net leverage at 1x.

Viking Holdings stock’s investment thesis rests on whether 15% capacity growth in 2027 translates into double-digit yield growth, or whether macro headwinds compress the net yield gains that the early booking data suggests.

What Has to Go Right

- The 2027 booking curve holds its 31% year-over-year advance in advanced bookings as the remaining 62% of capacity comes to market, supported by mid-single-digit yield growth targets management has reiterated

- Ocean net yield, currently running at $882 per PCD for 2027 versus $786 at the same point in 2025, continues to reflect real pricing strength rather than a mix effect from early high-yield bookings

- SG&A efficiencies from digital and LLM-optimization tools Talactac referenced on the earnings call materialize as the company scales marketing for a 15% capacity growth year

- Fuel cost exposure, currently approximately 4% of adjusted gross margin, remains manageable; Ocean’s fleet fuel efficiency and River’s fixed-price 2026 contracts limit the downside

What Could Still Go Wrong

- The River segment’s 8% capacity decline in Q1 and brief demand softening following macroeconomic events show that Viking’s forward bookings, while sticky, are not immune to near-term disruption

- The net income margin expansion to 19% required by the TIKR mid-case depends on operating leverage that has not yet materialized at scale: Q1 2026 operating margin was 1%, with vessel maintenance costs up 11% year-over-year

- Ocean air cost volatility remains an open exposure: Banh acknowledged on the earnings call that transatlantic pricing increases will present some headwind to adjusted gross margin in 2026

- Egypt capacity, representing 8 ships with approximately 80 guests per ship on average, is a high-yield but operationally sensitive itinerary, with two 2026 sailing weeks already canceled following recent geopolitical developments

Should You Invest in X?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up X stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track X alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VIK stock on TIKR for Free →