Key Stats

- Current price: ~$13 (May 14, 2026)

- Q1 2026 revenue: $128M, +19% YoY

- Q1 2026 ARR: $493M, +21% YoY

- Q1 2026 adjusted EBITDA: $30.6M, +29% YoY; margin 24%

- Q1 2026 GAAP net income: $30.6M; diluted EPS: $0.12

- Q2 2026 revenue guidance: $130M to $133M (+15% to +17%)

- Q2 2026 ARR guidance: $510M to $513M

- Q2 2026 adjusted EBITDA guidance: $29M to $31M

- TIKR model price target: ~$26 | Implied upside: ~99%

Cellebrite Stock Posts 19% Revenue Growth as Genesis AI Enters Final Sprint to GA

Cellebrite stock (CLBT) rose more than 8% on May 14 after the company reported Q1 2026 revenue of $128M, up 19% year over year.

ARR grew 21% to $493M, with sequential net new ARR of $12M representing a second consecutive quarter of stable additions following three quarters of headwinds, according to CFO David Barter on the Q1 2026 earnings call.

Adjusted EBITDA reached $30.6M, up 29% year over year, with margin expanding 190 basis points to 24%.

Growth products, including Guardian, Pathfinder, Corellium, and drone forensics, doubled on a year-over-year basis, according to Barter.

Total subscription revenue grew 23%, partially offset by an anticipated decline in nonrecurring training, hardware, and professional services, according to Barter.

The most consequential development of the quarter was the Genesis AI launch trajectory: announced on March 16 and made available to a select early-adopter group with no marketing or pricing, Genesis attracted more than 500 registered users across more than 15 countries in eight weeks, according to CEO Tom Hogan on the Q1 2026 earnings call.

Hogan confirmed that Genesis will reach general availability in mid-June, approximately 30 days from the call date.

Management had originally modeled zero AI product-specific revenue in the 2026 plan; Hogan stated directly that this assumption “will now obviously not be the case.”

Guardian Investigate, the company’s AI-powered case management platform, moved into general availability at the end of Q1 and is expected to see steady growth in the second half of 2026, according to Hogan.

On May 6, Cellebrite announced FedRAMP High authorization to operate, sponsored by the U.S. Department of Justice, opening U.S. federal agencies to the full Guardian platform and cloud offerings, a certification Hogan noted fewer than 100 companies hold.

The U.S. federal segment, which was essentially flat in 2025, is rebounding with a growth rate Hogan described as “clearly headed back to the 20s,” supported by a 35% year-over-year increase in the U.S. Fed pipeline, according to Hogan.

EMEA ARR growth accelerated 10 percentage points year over year to 25%, driven by defense and intelligence sector growth in the mid-30% range, according to Barter.

For Q2 2026, management guided ARR of $510M to $513M, revenue of $130M to $133M, and adjusted EBITDA of $29M to $31M, with approximately 2 percentage points of FX headwind factored into the outlook.

Cellebrite Stock Financials: Gross Margin Holds, Operating Margin Compresses

Cellebrite stock’s income statement tells a software scaling story interrupted by deliberate investment acceleration.

Gross profit in Q1 2026 was $110M, up 18% year over year, with gross margin at 83% compared to 84% in Q1 2025 and 85% in Q3 2024.

Gross margin has held in a narrow band between 83% and 86% across the eight quarters shown in the income statement, reflecting the stability of Cellebrite’s subscription-weighted revenue base.

Operating income fell to $10M in Q1 2026, down 26% year over year, with operating margin compressing sharply to 7% from 11% in Q1 2025.

Total operating expenses rose to $100M in Q1 2026 from $80M in Q1 2025, as SG&A and R&D both expanded in line with the company’s product and go-to-market investment cycle.

Barter noted on the Q1 2026 earnings call that the Q1 result absorbed a full quarter of Corellium costs, which was not the case in the prior-year period.

The operating margin compression is a function of deliberate spend timing rather than structural degradation: adjusted EBITDA margin expanded 190 basis points in the same quarter where GAAP operating margin fell, reflecting the gap between stock-based compensation, acquisition-related charges, and underlying profitability.

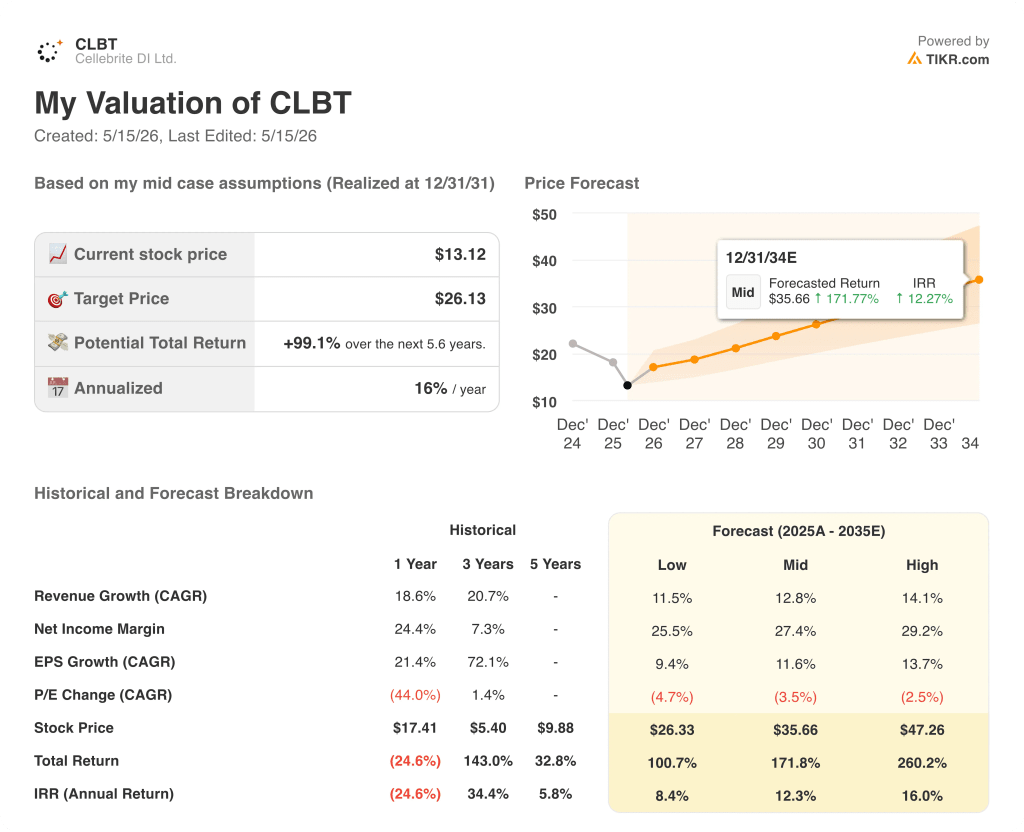

What Does the Valuation Model Say?

The TIKR model prices Cellebrite stock at ~$26 under mid-case assumptions, implying roughly 99% upside from the current price of ~$13.

The mid-case builds on a revenue CAGR of 13% from 2025 through 2035, with net income margin expanding to 27%.

The model also embeds a P/E multiple compression of 3.5% annually, meaning the price target is reached despite meaningful devaluation of the earnings multiple over time.

Q1’s results are broadly consistent with the mid-case assumptions: 19% revenue growth and expanding EBITDA suggest the model’s trajectory is intact at minimum, with Genesis monetization representing unmodeled upside.

The investment case for Cellebrite stock is stronger after this quarter: ARR growth reaccelerated sequentially, the AI product suite crossed into GA readiness, FedRAMP High certification removes a major barrier to federal cloud revenue, and management’s own 2026 AI revenue assumption of zero is already being revised upward.

Genesis GA launched in mid-June, but converting 500 free beta users to paying customers at scale, without prior pricing experience, is the execution variable that determines whether the AI TAM estimate of $12.5 billion translates to near-term ARR.

What Has to Go Right

- Genesis reaches GA in mid-June as guided and early adopters convert to paid subscriptions, validating management’s view that the 2026 AI revenue assumption of zero is now too conservative

- The U.S. federal segment sustains its rebound into the 20%-plus growth range, supported by the 35% year-over-year pipeline increase and FedRAMP High authorization that gives Cellebrite stock a structural advantage as federal agencies finalize fiscal year 2027 technology budgets

- Growth products, including Guardian, Pathfinder, Corellium, and drone forensics, which doubled year over year in Q1, continue compounding as platform deals replace point-product renewals across both EMEA and federal accounts

- The TIKR mid-case revenue CAGR of 13% proves conservative if Genesis penetrates even a fraction of the estimated 500,000-investigator addressable market at the $20,000 to $30,000 per-user pricing management sketched on the call

What Could Still Go Wrong

- Genesis monetization pricing is untested: management acknowledged on the Q1 2026 earnings call that any initial pricing figure “is going to be wrong,” and aggressive seeding could suppress near-term ARR contribution even as adoption scales

- Q1 2026 operating margin compressed to 7% from 11% a year earlier, and continued R&D and go-to-market investment in AI and cloud could sustain this pressure longer than the adjusted EBITDA trend suggests

- The Corellium acquisition remains subject to pending CFIUS approval, leaving a material growth asset in a regulatory holding pattern with no confirmed timeline

- Net new ARR of $12M in Q1 was flat year over year, with management attributing the shortfall partly to deal push and an unusually small pool of expiring contracts; if Q2 does not deliver the guided step-up to $17M to $20M in net new ARR, the reacceleration narrative weakens

Should You Invest in Cellebrite DI Ltd.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Cellebrite DI Ltd. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cellebrite DI Ltd. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CLBT stock on TIKR for Free →