Key Takeaways:

- General Motors beat Q1 2026 adjusted EPS estimates with $3.70, versus the analyst estimate of $2.62. GM stock has surged around 56% over the past year, trading near $78, close to its 52-week high of $88

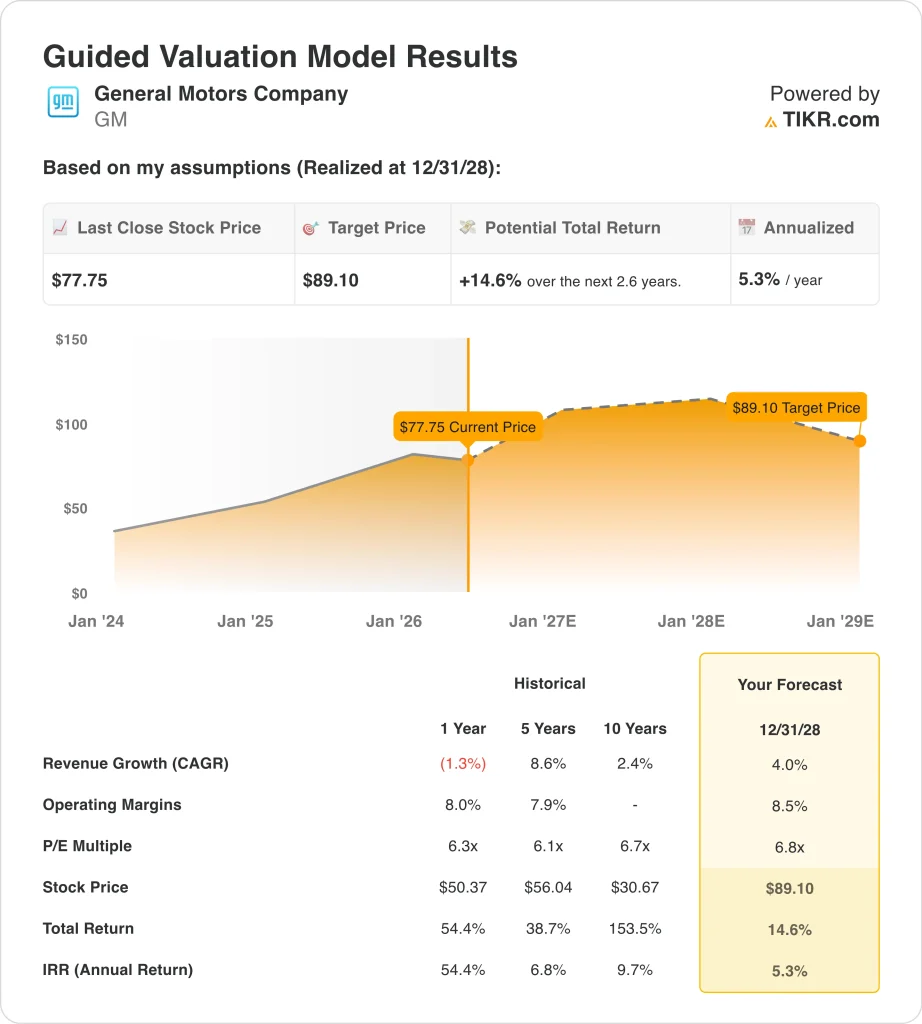

- GM stock could rise from $78 to around $89 per share by December 2028

- That implies a total return of around 15%, or around 5% annualized over the next 2.6 years

What Happened?

General Motors Company (GM) posted one of its strongest earnings beats in recent memory. Q1 2026 adjusted earnings per share came in at $3.70, far above the analyst estimate of $2.62. That beat is large by any standard, and it drove significant buying interest in the stock.

Q1 US vehicle deliveries reached 626,429 units, demonstrating solid demand across GM’s lineup. Management also highlighted that deferred revenue from software and services is expected to reach approximately $7.5 billion by year’s end, up nearly 40% from 2025 levels.

That software narrative matters because it signals GM is evolving beyond a traditional automaker toward a technology-driven mobility company with more recurring revenue.

But the picture beyond the earnings headline is more complex. GM is cutting hundreds of white-collar workers, according to Bloomberg News, as it works to trim costs across its corporate structure. The company’s joint venture with LG Energy Solution at its Ohio battery plant faces an uncertain restart timeline, which could delay EV production capacity expansion.

And GM recently settled a California driver privacy probe for $12.75 million. On the macro side, tariff uncertainty continues to weigh heavily on the auto sector. GM and other automakers are banking on future tariff refunds totaling billions of dollars, and any policy shifts could meaningfully affect cost structures.

The EPA is also proposing to delay enforcement of Biden-era vehicle pollution rules, which reduces near-term compliance costs but introduces longer-term regulatory uncertainty. GM invested $830 million across three US propulsion plants in April 2026 and committed over $690 million in Canada for next-generation engine production.

Here’s why GM stock could deliver modest returns over the next several years even after its impressive 12-month rally.

What the Model Says for GM Stock

We analyzed the upside potential for General Motors stock based on its near-term earnings strength, gradual EV and software monetization progress, and steady volume from its core North American truck and SUV markets.

Based on estimates of 4.0% annual revenue growth, 8.5% operating margins, and a normalized P/E multiple of 6.8x, the model projects General Motors’ stock could rise from $78 to around $89 per share by December 2028.

That would be a 14.6% total return, or a 5.3% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for GM stock:

1. Revenue Growth: 4%

General Motors generated 626,429 US vehicle deliveries in Q1 2026, demonstrating solid consumer demand. But overall revenue growth faces significant headwinds. The company’s 1-year revenue growth was actually negative at around 1.3%, reflecting the impact of slower EV adoption and shifts in vehicle mix. The 5-year compound annual growth rate stands at 8.6%, but the 10-year rate is only around 2.4%.

Based on analysts’ consensus estimates, we used a 4.0% annual revenue growth rate. This reflects expectations for steady growth in GM’s truck and SUV business, partially offset by EV transition costs and ongoing production adjustments. The forward 2-year consensus revenue compound annual growth rate is around 1.7%, suggesting near-term revenue growth may be modest before recovering.

Management’s target of approximately $7.5 billion in deferred software and services revenue by year-end is the key upside driver. This segment could add incremental growth well beyond traditional vehicle sales as it scales.

2. Operating Margins: 8.5%

General Motors generates an LTM operating margin of around 6.6%, and its gross margin sits near 11%. These are thin margins by most comparisons but are typical for large-scale auto manufacturers operating in a capital-intensive, competitive industry. And the company is investing heavily in US production capacity, with $830 million committed to propulsion plants in 2026 alone.

Based on analysts’ consensus estimates, we used an 8.5% operating margin target. This assumes GM successfully manages its transition costs while growing higher-margin software and services revenue over time. Cost-cutting measures, including the white-collar workforce reduction, should also contribute to margin improvement through 2028.

Tariff risk is the biggest potential headwind to reaching this margin target. Any sustained increase in input costs from trade policy changes could pressure margins significantly below our assumption.

3. Exit P/E Multiple: 6.8x

General Motors trades at a low P/E multiple of around 6x on a next-twelve-months basis. That reflects the market’s caution about cyclical auto demand, EV transition costs, and broader macro risks facing the industry. Based on analysts’ consensus estimates, we used a 6.8x exit multiple.

This is a very modest multiple by most market standards. It assumes the market will continue to discount GM’s earnings due to cyclical concerns and EV uncertainty. But it also means there is limited downside from multiple compressions if earnings remain stable.

The consensus analyst target of around $94 per share sits above the current price of $78. So analysts see some upside. But the model suggests that at current margin levels and growth rates, the long-term return potential is modest rather than exceptional.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

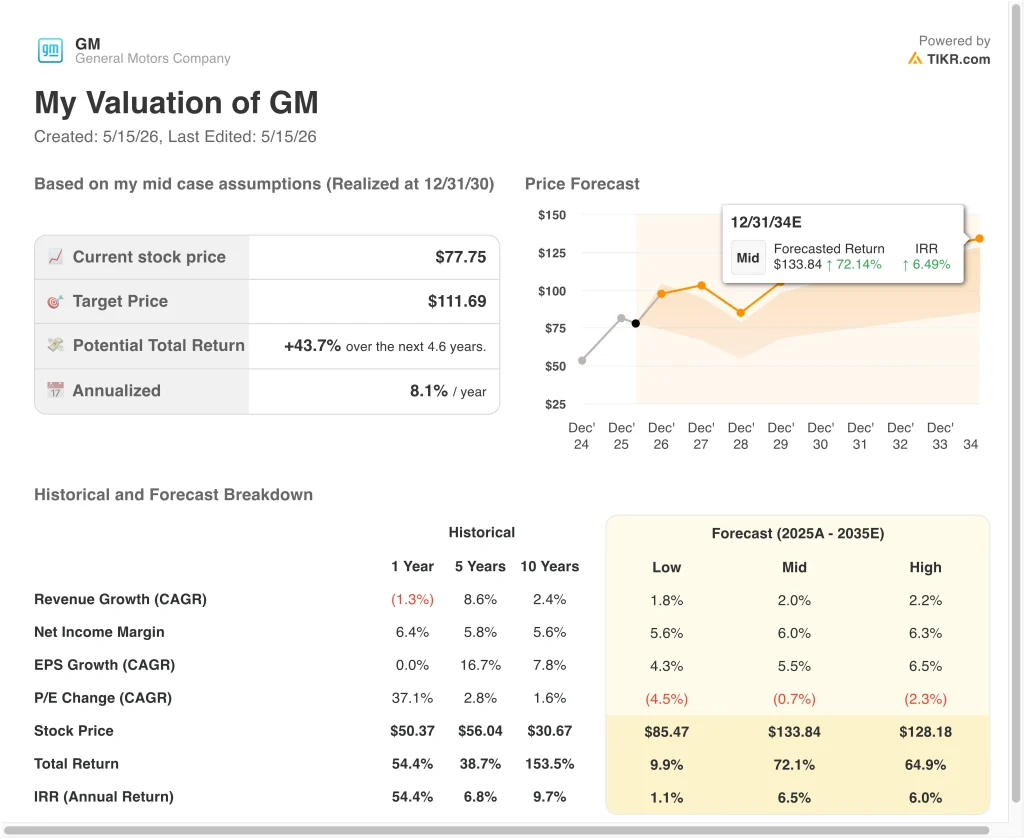

Different scenarios for GM stock through 2035 show varied outcomes based on revenue growth, margin performance, and software monetization progress (these are estimates, not guaranteed returns):

- Low Case: Revenue grows slowly, and margins face pressure from tariffs and EV transition costs → 1.1% annual returns

- Mid Case: Steady volume growth and cost discipline deliver moderate compounding → 6.5% annual returns

- High Case: Software services scale faster, and truck margins remain resilient through the cycle → 6.0% annual returns

Going forward, General Motors faces a complex but potentially rewarding path. The company’s strong earnings beat and its significant stock rally over the past year show the market is recognizing real operational improvements.

But the model’s projected returns suggest the stock may already reflect much of the near-term good news, and investors should weigh the ongoing risks from tariffs, EV costs, and macro uncertainty carefully before building a position.

See what analysts think about GM stock right now (Free with TIKR) >>>

Should You Invest in General Motors?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GM, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GM alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!