Key Stats

- Current price: $7.44 (May 14, 2026)

- Q1 2026 revenue: $648M, +15.9% YoY

- Q1 2026 adjusted EBITDA: $84.4M, +25.2% YoY

- Full-year 2026 revenue guidance: $2.56B to $2.58B

- Full-year 2026 adjusted EBITDA guidance: $328M to $332M

- TIKR model price target: $8

- Implied upside: +11.9% over 5 and a half years (annualized: 2.5%/year)

Aveanna Healthcare Stock Beats on Revenue and EBITDA Across All Three Segments

Aveanna Healthcare Holdings (AVAH) delivered Q1 2026 revenue of $648M, a 15.9% increase over the prior year period, alongside adjusted EBITDA of $84.4M, up 25.2% year over year.

Aveanna Healthcare stock’s top-line growth was broad-based, with all three operating divisions posting double-digit or high-single-digit year-over-year gains for the quarter.

Private Duty Services, the company’s largest segment, generated revenue of approximately $536M in Q1, up 16.4% year over year, driven by 12.1 million hours of care and a 10.7% volume increase.

Revenue per hour in PDS reached $44.43 in Q1, up 5.7% from the prior year quarter, with growth attributed to increased preferred payer volume and updated reimbursement agreements, according to Chief Financial Officer Matt Buckhalter on the Q1 2026 earnings call.

Home Health and Hospice revenue came in at approximately $66.6M for the quarter, up 17.4% year over year, with total episodes of care reaching 14,900, up 23.1% from the prior year quarter.

Episodic mix reached approximately 80% in Q1, above the company’s 75% target, with total admissions of approximately 11,000 representing 13.4% organic growth over the prior year period, according to Chief Executive Officer Jeff Shaner on the Q1 2026 earnings call.

Medical Solutions produced Q1 revenue of $45.7M, up 7.4% year over year, on approximately 93,000 unique patients served and revenue per unique patient served of approximately $491, up 2.9% year over year.

Management flagged approximately $6M in previously reserved accounts receivable that was collected in Q1 and flowed through both revenue and EBITDA, according to Buckhalter on the Q1 2026 earnings call, adding a timing benefit to the headline result.

Based on Q1 strength and continued execution of its preferred payer strategy, Aveanna raised its full-year 2026 revenue guidance to a range of $2.56B to $2.58B and full-year adjusted EBITDA guidance to $328M to $332M, up from the prior outlook; these figures exclude the pending Family First Homecare acquisition.

Aveanna announced the pending acquisition of Family First Homecare, a Florida-based pediatric home care provider, with the transaction expected to close in late Q2 2026; management stated that Family First carries revenue of approximately $120M and was valued at approximately 7.5x post-synergy EBITDA.

The company also addressed a CMS announcement of a 6-month Home Health enrollment moratorium, with Shaner stating on the Q1 2026 earnings call that the development has “absolutely 0 impact” on Aveanna’s 2026 or 2027 business plan given that the company’s Home Health platform was built through M&A and organic growth rather than new Medicare licensure applications.

Net leverage reached approximately 3.8x on an LTM basis at the end of Q1, according to Buckhalter on the Q1 2026 earnings call, down from double-digit levels in prior years.

Aveanna Healthcare Stock: What the Income Statement Shows

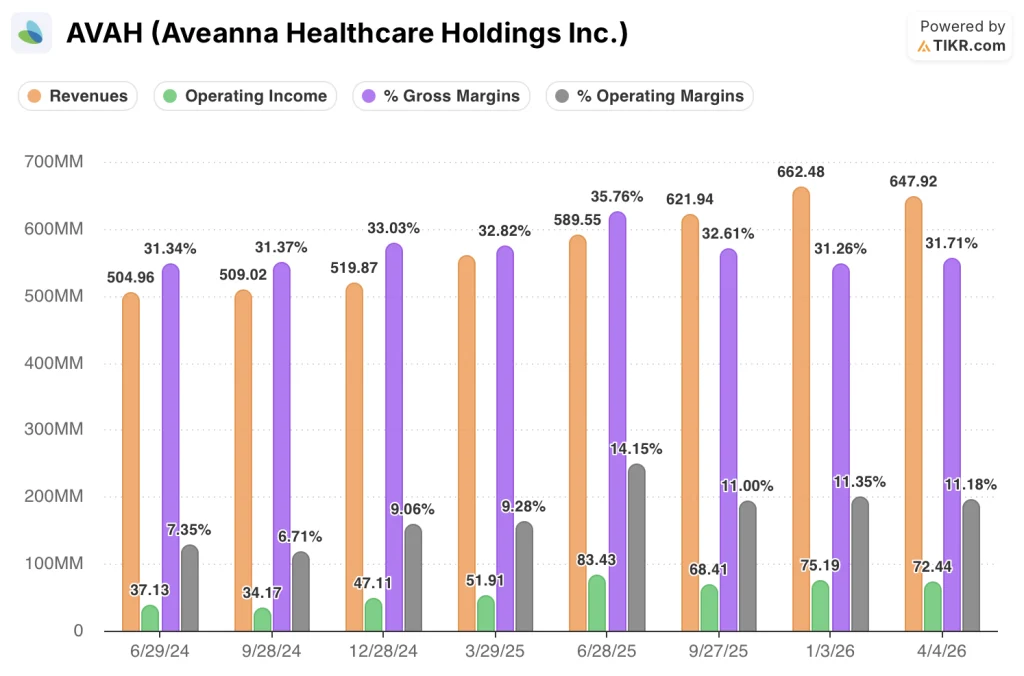

The Q1 2026 income statement reflects a business that has expanded operating leverage steadily across four quarters, even as gross margin plateaued near 32%.

Revenue has climbed from $505M in Q2 2024 to $621M in Q3 2025 and $662M in Q4 2025, before settling at $648M in Q1 2026, with the sequential dip consistent with normal seasonal patterns in the business.

Gross margin held at 31.7% in Q1 2026, roughly flat with the 31.3% reported in both Q2 2024 and Q4 2025, following a peak of 35.8% in Q2 2025.

The more notable trend is operating income, which grew from $37M in Q2 2024 to $83M in Q2 2025, before moderating to $68M in Q3 2025 and recovering to $75M in Q4 2025 and $72M in Q1 2026.

Operating margin reached 11.2% in Q1 2026, up from 7.4% in Q2 2024, reflecting a meaningful structural improvement even with gross margins in a narrower band.

Buckhalter noted on the Q1 2026 earnings call that SG&A discipline has been sustained through automation and AI efforts in revenue cycle management, allowing the company to grow volumes across all three segments without adding proportional overhead.

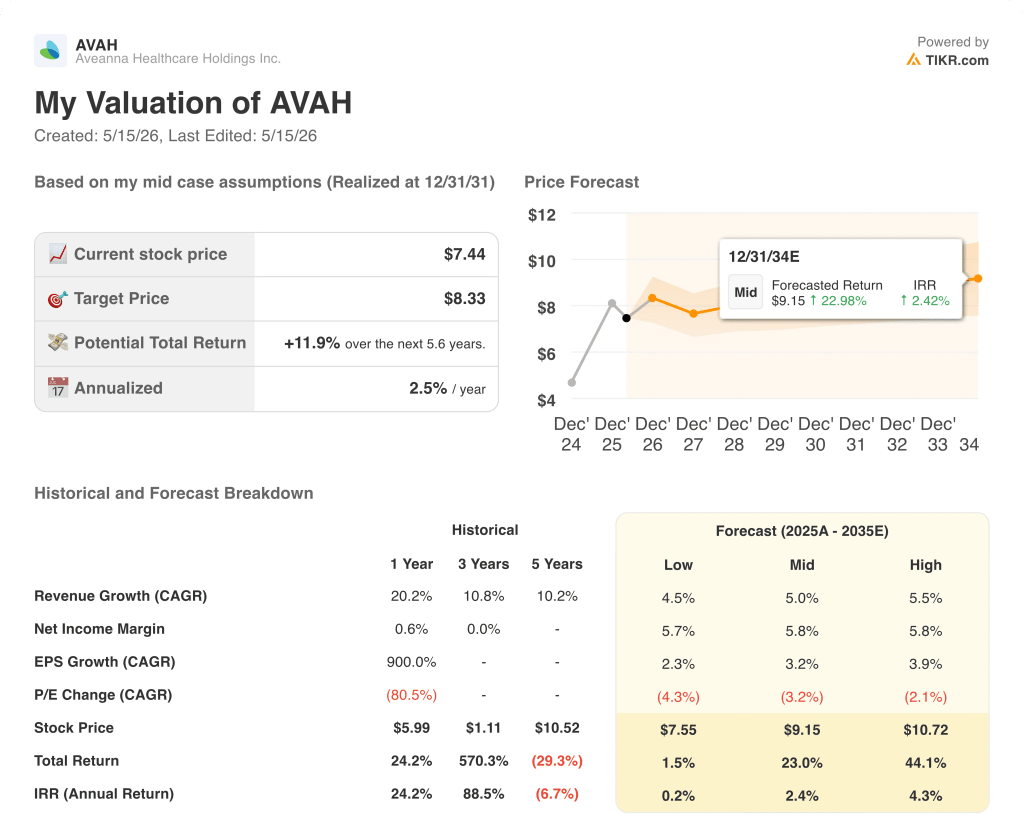

What Does the Valuation Model Say?

The TIKR mid-case model sets a price target of $8.33, representing a total return of 11.9% from the current price of $7.44 over 5.6 years, or 2.5% annualized.

The model’s mid-case assumes a revenue CAGR of 5.0% and a net income margin of 5.8%, with a P/E compression of 3.2% per year embedded in the forecast through 2031.

That P/E compression assumption is the key constraint on the return profile: even with mid-single-digit revenue growth and a net income margin well above current levels, the model prices in a meaningful multiple contraction that caps the annualized return at 2.5%.

Aveanna Healthcare stock’s Q1 result, including the guidance raise and the preferred payer momentum across all three segments, strengthens the revenue growth case but does not materially alter the valuation picture against a mid-case that already prices in multiple compression.

The investment case for Aveanna Healthcare stock hinges on whether operating leverage and preferred payer penetration can sustain margin expansion fast enough to offset the multiple contraction the model embeds over the next five years.

What Has to Go Right

- PDS preferred payer volume, which reached approximately 60% of MCO volumes in Q1 2026 up from 57% at year-end 2025, must continue shifting, with management targeting a long-run mix of 80%+, to sustain revenue per hour growth above the rate of caregiver wage inflation

- Home Health and Hospice episodic mix must hold above 75%, and episode volume growth of 23.1% year over year in Q1 must be sustained for the segment’s 53.7% gross margin profile to anchor the consolidated margin recovery

- Medical Solutions, which produced 4.5% volume growth and 44.7% gross margin in Q1, must execute its preferred payer modernization through the back half of 2026 to deliver the double-digit growth management projected by Q4

- The Family First Homecare acquisition, valued at approximately 7.5x post-synergy EBITDA on approximately $120M in revenue, must integrate within the 6-month window management cited, with full synergies captured before year-end 2026

What Could Still Go Wrong

- Approximately $6M in timing-related AR collections boosted Q1 revenue and EBITDA; backing that out, management characterized the underlying EBITDA run rate as the “high 70s,” meaning Q2 faces a tougher sequential comparison than the headline Q1 number implies

- The CMS 6-month Home Health enrollment moratorium, though management stated it has zero impact on current operations, introduces regulatory uncertainty that could affect M&A optionality in the Home Health segment beyond Family First

- Net leverage of approximately 3.8x remains elevated relative to management’s stated target of at or below 3x, limiting capital allocation flexibility if organic growth or the Family First integration underperform

- PDS spread per hour, currently in the low $12 range, is expected to stay relatively flat as new preferred payer contracts are signed at rates that offset moderated government Medicaid wins rather than expand above them, leaving volume as the primary growth lever

Should You Invest in Aveanna Healthcare Holdings Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Aveanna Healthcare Holdings stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Aveanna Healthcare Holdings stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AVAH stock on TIKR for Free →