Key Stats

- Current price: ~$42 (May 15, 2026)

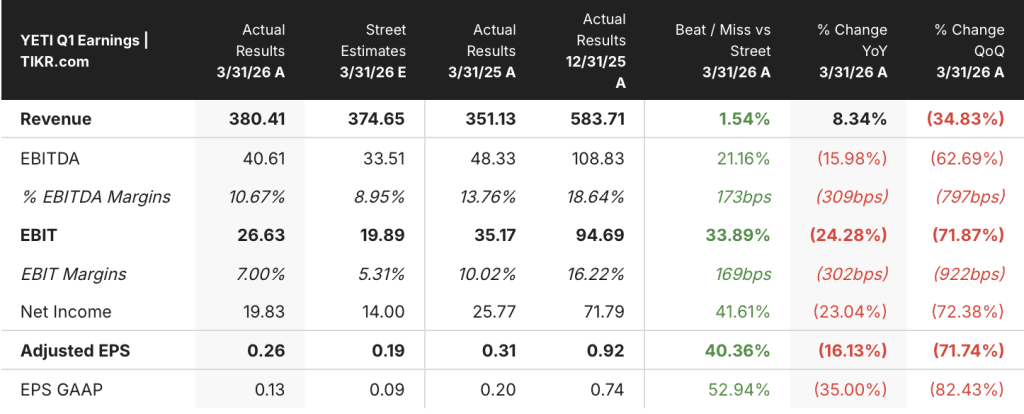

- Q1 2026 revenue: $380M, +8% YoY

- Q1 2026 adjusted EPS: $0.26, down from $0.31 in Q1 2025

- Full-year 2026 revenue growth guidance (raised): 7% to 8% (prior: 6% to 8%)

- Full-year 2026 adjusted EPS guidance (raised): $2.83 to $2.89, +14% to +17% YoY (prior: $2.77 to $2.83)

- Full-year 2026 adjusted operating income growth guidance (raised): 8% to 10% (prior: 6% to 8%)

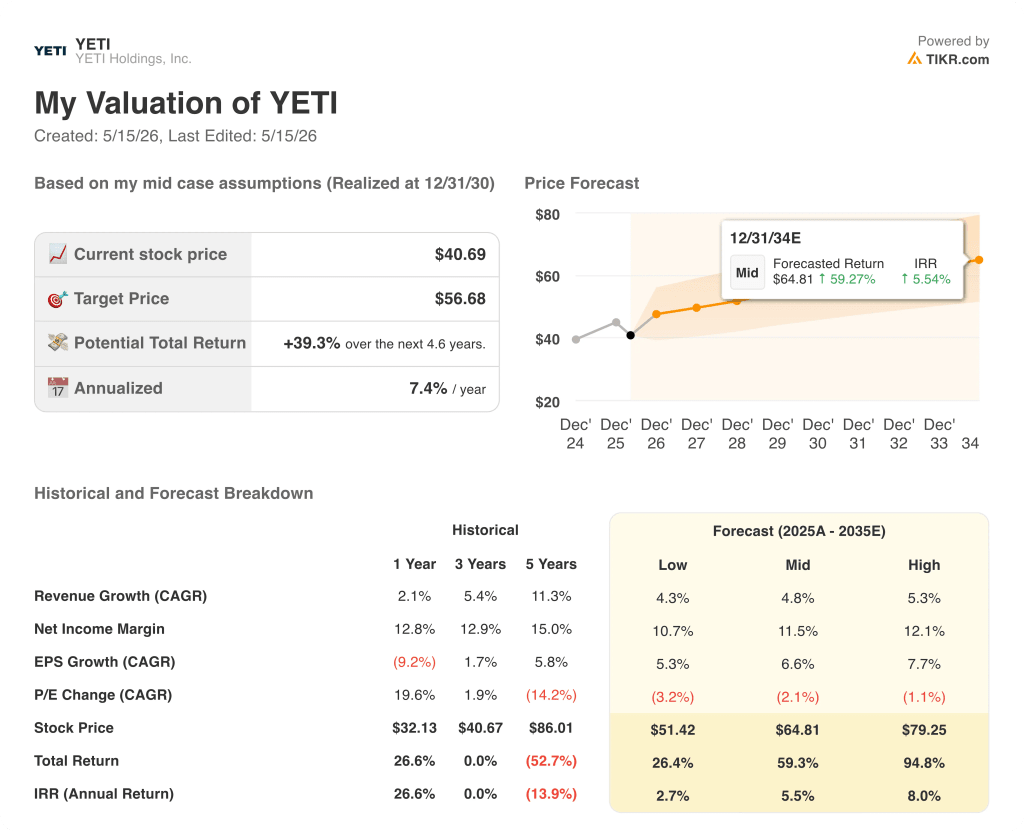

- TIKR model price target (mid case): ~$57, implied upside: ~39% over 4 and a half years

YETI Stock Earnings Breakdown: Q1 2026

YETI stock (YETI) opened its 2026 account with $380M in Q1 revenue, up 8% year-over-year and coming in at the top end of its initial full-year guidance range of 6% to 8% growth.

Wholesale drove the headline, growing 19% to $184M, the strongest wholesale quarter YETI has delivered in more than three years, driven by double-digit sell-through growth in the U.S. and healthy channel inventory heading into the year’s seasonally larger quarters.

Coolers & Equipment grew 11% to $156M, led by soft coolers, bags, hard coolers, cases, and storage, with demand continuing to outpace supply in soft coolers and bags specifically — a constraint management expects additional capacity in the second half to resolve.

Drinkware posted 5% growth to $217M, the second consecutive quarter of mid-single-digit growth, and the first return to growth in the U.S. Drinkware business after prior-year inventory corrections, supported by new launches including stackable cups, chug bottles, ceramic mugs, and the Yonder Shaker bottle.

Direct-to-consumer sales came in flat at $197M, with strength in e-commerce, Amazon Marketplace, and YETI retail stores offset by a year-over-year decline in corporate sales tied to order timing, a tougher year-over-year comparison, and softer demand from corporate buyers, according to CFO Scott Bomar on the Q1 earnings call.

YETI stock’s adjusted EPS declined to $0.26 from $0.31 in the prior-year quarter, reflecting an incremental unfavorable net tariff impact of approximately $0.09, according to Bomar.

Tariffs are the defined headwind for the first half of the year: gross margins declined 200 basis points year-over-year to 55.3%, including a 280 basis point drag from higher tariff costs, partially offset by lower product costs and FX favorability.

YETI raised both ends of its full-year guidance: adjusted EPS guidance moved to $2.83 to $2.89 from $2.77 to $2.83, reflecting a higher operating margin outlook of approximately 14.6%, up 20 basis points from the prior guidance of 14.4%; full-year gross margin guidance was tightened to 56.5% to 57% from 56% to 57%.

Management projects year-over-year gross margin to decline roughly 200 basis points in the first half, followed by approximately 50 basis points of year-over-year expansion in the second half as tariff pressures from late 2025 roll off.

The Board expanded YETI’s share repurchase authorization by $350M, bringing the total remaining authorization to $500M, building on roughly $300M in repurchases executed during 2025 and a planned additional $100M in 2026.

YETI Stock Financials: Margin Pressure Running on a Clock

YETI stock’s income statement tells a margin compression story that is front-loaded by design, with a second-half recovery built into the company’s own guidance.

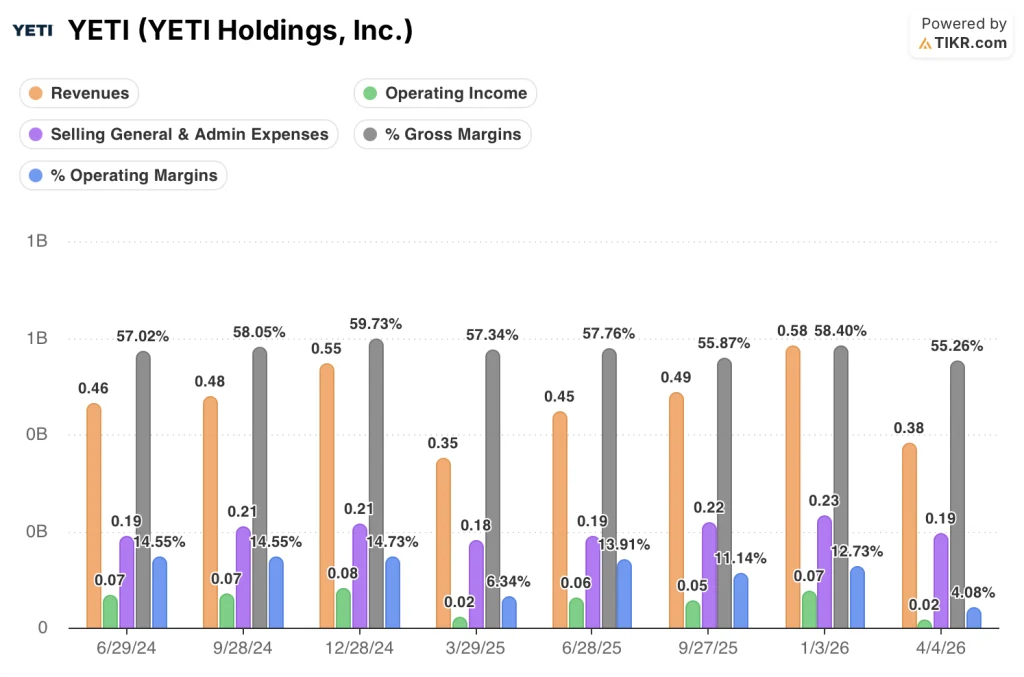

Revenue grew from $350M in Q1 2025 to $380M in Q1 2026, continuing a trend of sequential re-acceleration after a soft Q1 2025 that showed only 2.9% year-over-year growth at that point in the cycle.

Gross margin has moved in a band across the trailing quarters: 57.3% in Q1 2025, 57.8% in Q2 2025, 55.9% in Q3 2025, 58.4% in Q4 2025, and 55.3% in Q1 2026, with the current-quarter reading the softest in the trailing eight periods shown.

Operating margin followed the same arc: 14.5% in Q2 2024, 14.6% in Q3 2024, 14.7% in Q4 2024, then falling to 6.3% in Q1 2025 before recovering to 13.9%, 11.1%, and 12.7% across Q2 through Q4 2025 — and pulling back again to 4.1% in Q1 2026.

The Q1 pattern reflects the seasonal reality that Q1 is structurally YETI’s smallest revenue quarter, which amplifies the fixed-cost burden on margins relative to the larger back-half quarters.

Adjusted SG&A grew 10% to $184M in Q1 2026, with management attributing the increase to new store investments, international headcount, and technology spending to support digital businesses — costs that are expected to moderate as a percentage of revenue in the second half, according to Bomar.

Adjusted operating income declined 24% to $27M, or 7% of sales, with management guiding to approximately 350 basis points of operating margin improvement in the second half to offset the roughly 450 basis point first-half decline.

What Does the Valuation Model Say?

The TIKR model places YETI stock’s mid-case price target at $57 against a current price of approximately $41, implying ~39% total return over 4 and a half years, or a 7.4% annualized rate.

The mid case assumes a revenue CAGR of 4.8% and a net income margin of 11.5%, with EPS growing at a 6.6% CAGR, alongside P/E multiple compression of 2.1% per year.

That P/E compression assumption is the constraint: even with EPS growing at 6.6% annually, the model is pricing in a shrinking earnings multiple over time, which limits the price appreciation available to investors who buy at today’s level.

The Q1 beat and guidance raise strengthen the near-term execution case, but the 7.4% annualized return on the mid case is a measured outcome — not a re-rating story.

YETI stock’s investment case is incrementally stronger after Q1: the top-line raise, the tariff headwind framed as transient, and the wholesale momentum are all signals the operational thesis is intact, but the return profile still requires patience and multiple compression tolerance.

YETI stock’s Q1 demonstrated clear demand durability, but the full-year case rests on second-half margin recovery that has not yet materialized.

What Has to Go Right

- Gross margin must recover to the 56.5% to 57% full-year guide as tariff comps ease in the back half, closing the ~200 basis point year-over-year gap from Q1

- Soft cooler and bag supply constraints must resolve with additional capacity arriving in H2 2026 as guided, converting identified demand backlog into recognized revenue

- International growth must sustain in the high teens to 20% range for the full year, with corporate sales lumpiness in Q1 not repeating at scale across Q2 to Q4

- Corporate sales must continue the early-Q2 improvement management flagged on the call, recovering from the order-timing softness that suppressed D2C growth in Q1

What Could Still Go Wrong

- The Section 122 tariff arrangement is temporary, and management’s base case assumes IEEPA rates return to approximately 20% in July, restoring the cost headwind and potentially eroding the guidance raise if realized tariff rates deteriorate further

- Gross margin declined to 55.3% in Q1 2026, the softest reading in the trailing eight quarters; if the H2 recovery underdelivers, full-year operating margin of 14.6% is at risk and the EPS guide range of $2.83 to $2.89 compresses toward its floor

- D2C was flat at $197M with corporate sales acting as the drag; if corporate buyers remain cautious into Q2 and Q3, the channel mix shift toward wholesale (which carries lower margins than DTC) could pressure gross margin recovery further

- The TIKR mid-case assumes P/E compression of 2.1% annually: if execution stumbles in any of the above scenarios, multiple compression accelerates and the ~39% total return projection over 4.6 years shrinks materially

Should You Invest in YETI Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up YETI Holdings, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track YETI Holdings, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze YETI stock on TIKR for Free →