Key Stats for Carvana Stock

- 52-Week Range: $54 to $97

- Current Price: $70

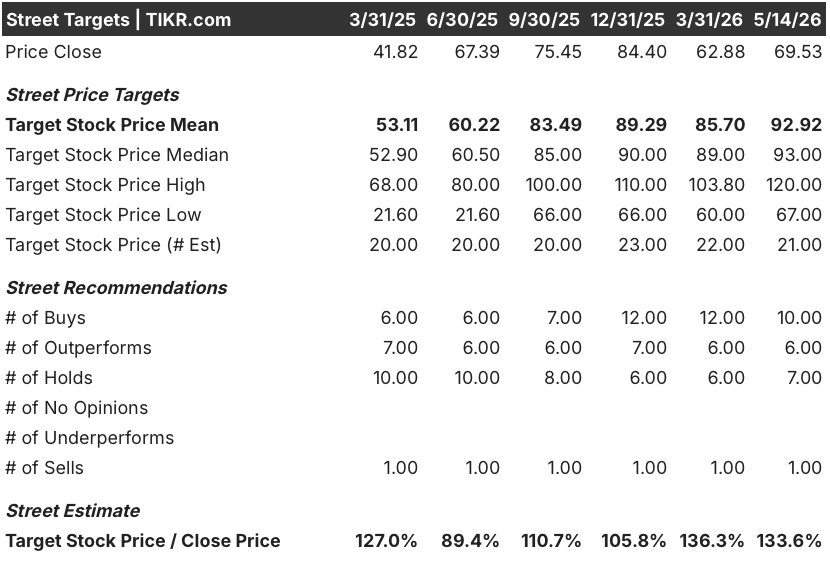

- Street Mean Target: $93

- Street High Target: $120

- Analyst Consensus: 10 Buys / 6 Outperforms / 7 Holds / 0 Underperforms / 1 Sell

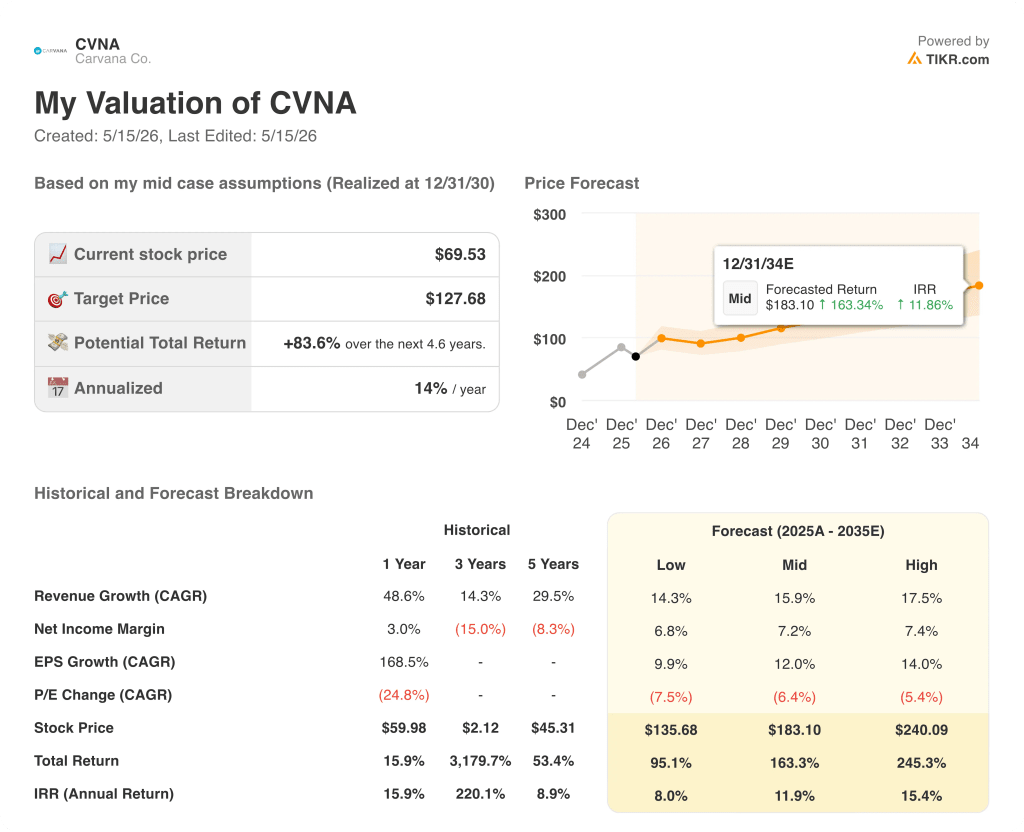

- TIKR Model Target (Dec. 2030): $128

What Happened?

Carvana (CVNA) is the largest online used-car retailer in the United States, selling vehicles entirely through its digital platform and a network of inspection, reconditioning, and logistics infrastructure built to move cars at a scale no traditional dealer can match.

The company’s first quarter of 2026 was, by almost every metric, a record.

Retail units sold reached 187,393, a 40% year-over-year increase and the sixth straight quarter of at least 40% growth.

Revenue came in at $6.43 billion, up 52% from $4.2 billion in the same period a year ago, beating the analyst consensus of $6.08 billion by more than $350 million.

Adjusted EBITDA hit $672 million, a record and a beat against the $649 million consensus, with an adjusted EBITDA margin of 10.4%.

“The first quarter was another outstanding quarter for Carvana,” CEO Ernie Garcia said on the Q1 2026 earnings call, noting the company set records across retail units sold, GAAP operating income, and adjusted EBITDA simultaneously for the ninth consecutive quarter.

The result came after a difficult fourth quarter of 2025, when higher-than-expected vehicle reconditioning costs squeezed gross profit per unit and sent Carvana stock down sharply in February 2026.

Reconditioning operations drove the Q4 miss, specifically labor inefficiency at several facilities during a period of rapid capacity expansion.

The recon team responded by building new manager-facing tools inside Carvana’s proprietary CARLI software, enabling faster real-time staffing decisions, optimized flow through paint lines, and a productivity tracker to catch performance gaps before they compound.

Garcia confirmed on the earnings call that by April 2026, labor efficiency across the network had recovered to just shy of the company’s all-time best.

Carvana is also expanding its physical footprint through ADESA integration, adding inspection and reconditioning capability at wholesale auction sites in Chicago and Syracuse, with the Chicago buildout expected to add around 100 jobs over time and the Syracuse site around 200.

The company’s long-term target remains 3 million retail units per year at 13.5% adjusted EBITDA margins, a goal management set for achievement by 2030 to 2035.

At its current pace and with 20% of its real estate capacity still unused, the path to 3 million units is as much an execution challenge as a capital one.

Wall Street’s Take on CVNA Stock

The Q1 beat reframed the February reconditioning narrative cleanly: the Q4 miss was operational, not structural, and the recon team’s response proved it.

CVNA’s adjusted EBITDA grew to $672 million in Q1 2026, up from $488 million a year earlier, with consensus now projecting around $760 million for Q2 as the company guides to sequential all-time records on both units and EBITDA.

Coverage sits at 10 Buys / 6 Outperforms / 7 Holds / 0 Underperforms / 1 Sell, with a mean price target of $92.92, implying around 34% upside from the current price of $70; BTIG raised its target to $485 pre-split (around $97 split-adjusted), citing unit growth, margin upside, and lean inventory discipline, while J.P. Morgan moved to $465 pre-split, noting the quarter delivered on both quality and quantity.

The spread between the $67 floor target and the $120 high is wide enough to matter: the bear case anchors to continued gross profit per unit pressure from narrower wholesale-to-retail spreads and elevated reconditioning costs, while the bull case prices in the full operating leverage benefit of 40% unit growth flowing through a largely fixed cost base.

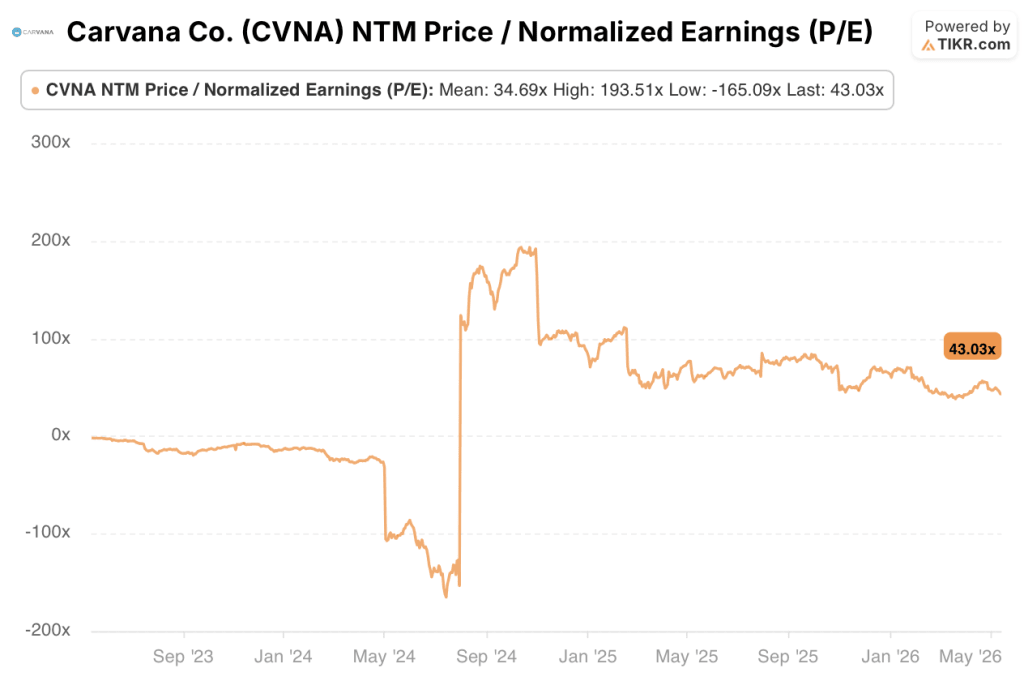

Trading at 43x next twelve-month earnings against a 5-year historical mean of around 35x, Carvana stock appears fairly valued on a P/E basis, though consensus projecting EBITDA growth of around 27% in Q2 and around 28% in Q3 makes that premium increasingly defensible as operating leverage compounds.

The primary risk is a reversion in reconditioning efficiency: if the April recovery in labor hours per unit does not hold as the company accelerates ADESA integrations, Q2 retail GPU compression could overshoot the $100 to $200 tariff-related headwind the company has already guided to.

Q2 2026 earnings, expected in late July, will confirm whether sequential unit records and EBITDA records materialized as guided, with adjusted EBITDA above $672 million as the number to watch.

Carvana Financials

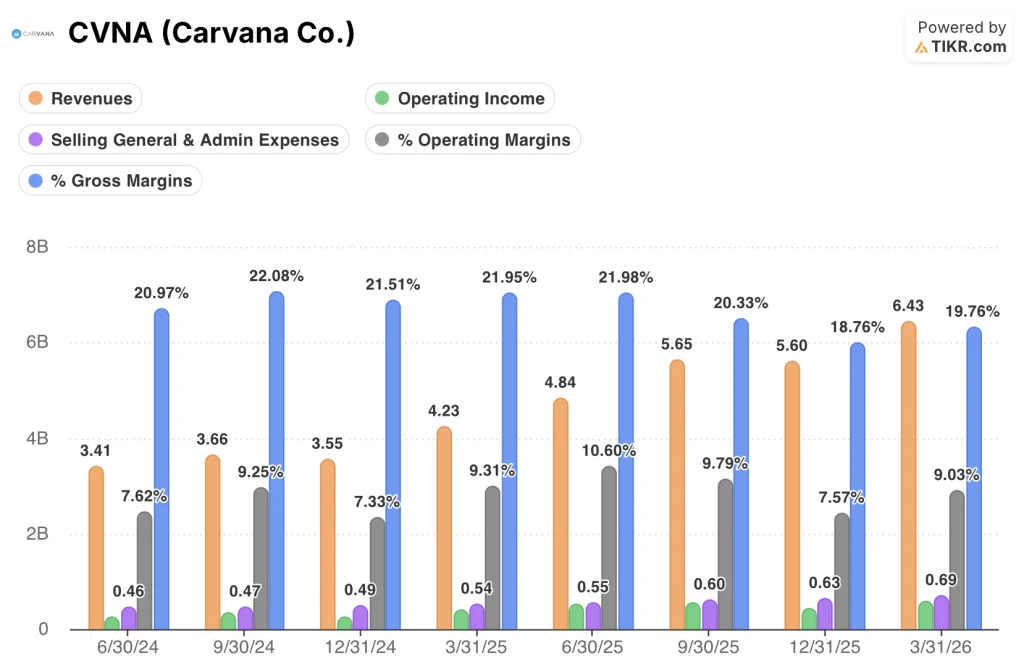

Carvana’s revenue surged to $6.43 billion in Q1 2026, a 52% increase from $4.23 billion a year earlier, marking an acceleration from the 41.9% and 54.5% growth rates posted in the prior two quarters.

Operating income reached $581 million in Q1, up from $390 million in Q1 2025, as operating margins expanded to 9.0% from 9.3% a year ago despite the significant revenue ramp.

The gross margin trajectory tells a more nuanced story: gross margins compressed from 22.0% in Q1 2025 to 19.8% in Q1 2026, primarily driven by higher reconditioning costs and lower shipping fees as Carvana passed logistics savings directly to customers.

SG&A expenses grew to $690 million in Q1 2026 from $540 million a year earlier, but fell meaningfully on a per-unit basis as the 40% unit growth drove operating leverage across the fixed cost base, with overhead expenses expected to hold near Q1 levels for the rest of the year.

What Does the Valuation Model Say?

The TIKR mid-case model prices Carvana at around $128 per share by December 2030, anchored to around 16% revenue CAGR and a net income margin expanding toward 7.2%, assumptions that track closely to management’s own 3-million-unit, 13.5%-EBITDA-margin framework.

At $70 today against a mid-case model target of around $128, the gap looks compelling on paper, but the NTM P/E of 43x against a 5-year historical mean of around 35x says the market is already pricing in meaningful execution: Carvana stock is fairly valued at current levels, with the upside to $128 earned only if unit growth holds at 40% and margin expansion toward 13.5% adjusted EBITDA materializes on schedule.

The investment case hinges on a single question: can Carvana sustain 40% unit growth while actually improving reconditioning efficiency, not just recovering from a one-quarter slip?

What Has to Go Right

- Retail unit growth holds at or above 40% through Q2 2026, producing sequential EBITDA records as guided, with adjusted EBITDA above $672 million confirming the recon recovery was structural

- The CARLI manager tools rolled out across facilities drive a measurable collapse in the performance spread between top-quartile and bottom-quartile reconditioning centers, which management noted remained at approximately $200 per unit as of Q1

- ADESA Chicago and Syracuse integrations add production capacity on a CapEx-light basis as the company moves toward full buildouts of existing ADESA facilities, extending the runway to 3 million units without greenfield spend

- Used EV mix continues to rise as a percentage of retail units sold, supporting a broader inventory pool and higher financing attach rates as Carvana builds out EV-specific monitoring and charging infrastructure

What Could Go Wrong

- Narrower wholesale-to-retail spreads deliver $100 to $200 of Q2 retail GPU compression on top of the tariff-related headwinds already guided to, pushing adjusted EBITDA below the sequential record threshold and reigniting the structural efficiency debate

- Fuel and diesel cost increases flow through logistics expense in Q2 at a magnitude larger than management’s current “not particularly large” characterization, adding another headwind to an already compressed per-unit economics quarter

- Short interest, still elevated at roughly 10.7% of float as of February 2026, creates asymmetric downside risk if any single data point in Q2 disappoints, given how quickly Carvana stock moved on the February earnings miss

Should You Invest in Carvana Co.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Carvana Co. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Carvana Co. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CVNA stock on TIKR for Free →