Key Stats for Altria Stock

- 52-Week Range: $55 to $75

- Current Price: $72

- Street Mean Target: $69

- Street High Target: $82

- Analyst Consensus: 4 Buys / 0 Outperforms / 7 Holds / 1 Underperform / 1 Sell

- TIKR Model Target (Dec. 2030): $85

What Happened?

Altria Group (MO) is the parent company of Philip Morris USA, the maker of Marlboro cigarettes, and it controls one of the most durable cash-generation engines in the consumer staples universe.

On April 30, the company delivered a first-quarter earnings beat that sent shares up as much as 8.3% intraday, hitting their highest level since December 2017.

Revenue came in at $5.43 billion, ahead of the $4.58 billion analysts expected.

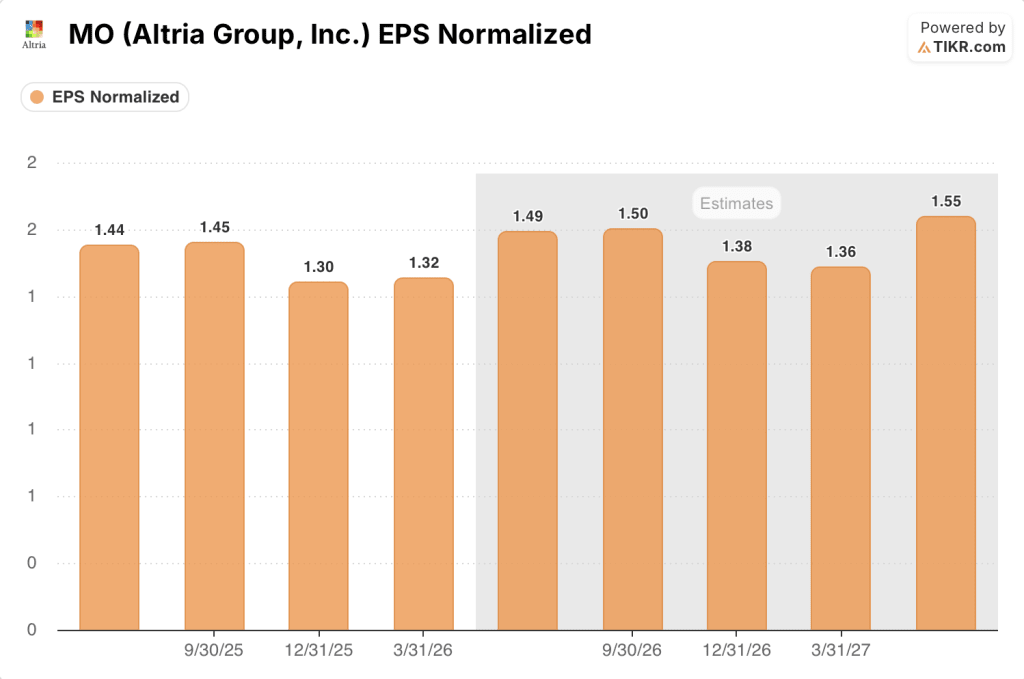

Adjusted EPS of $1.32 beat the $1.25 consensus and represented 7.3% growth over the same quarter a year ago.

The beat was not cost-driven. It was volume and pricing together, a combination the market had stopped expecting from a tobacco company.

CEO Billy Gifford, in his final earnings call (Q1 2026) before stepping down in mid-May, credited “disciplined execution” across the smokeable segment and called out a clear shift in the competitive landscape: illicit flavored e-vapor products, which had been taking share from cigarettes for years, appear to be hitting a saturation ceiling.

“We began to see signs of moderation in the back half of 2025,” Gifford said on the April 30 call, adding that “early indications” suggest the category’s prior growth trajectory “may be evolving.”

That moderation pulled some consumers back toward cigarettes, slowing Altria’s domestic cigarette volume decline to 2.4% and helping Marlboro expand its premium segment share to 59.5%, up 0.2 share points sequentially.

The discount segment told a parallel story: Basic, Altria’s lower-priced brand, gained 2.4 share points year-over-year as price-sensitive smokers traded down under elevated gas prices tied to the Iran conflict, and PM USA captured that movement rather than ceding it to competitors.

Beyond cigarettes, Altria’s FDA-authorized nicotine pouch on! PLUS began shipping nationally in March, reaching approximately 100,000 stores covering 85% of nicotine pouch category volume, with on! and on! PLUS together holding 7.8% of total oral tobacco retail share.

The company reaffirmed its full-year adjusted EPS guidance of $5.56 to $5.72, implying around 4% growth at the midpoint from a $5.42 base in 2025, and now expects that growth to be more balanced between the first and second halves of the year than it originally guided in February.

Wall Street’s Take on MO Stock

The Q1 beat landed at a moment when the market had written Altria off as a slow-declining cash cow with minimal upside, and the 7%-plus opening jump signaled a rapid reassessment of that assumption.

EPS Normalized for Q1 came in at $1.32, up 7.3% year-over-year, against a Street estimate of $1.25. Consensus now projects $1.49 for Q2 and $1.50 for Q3, implying a full-year NTM run rate of around $5.80 on continued mid-single-digit growth.

With 11 analysts covering the stock, Wall Street sits at 4 Buys / 0 Outperforms / 7 Holds / 1 Underperform / 1 Sell, with a mean price target of $69.36, implying modest downside from the current $72 price. The Street’s median target of $71.00 sits just below the current price as well, leaving the stock in territory where incremental upgrades could matter meaningfully.

The spread between the $50 low target (Jefferies, Underperform) and the $82 high target (Panmure Liberum, Buy) reflects a genuine strategic disagreement: bulls see on! PLUS and the e-vapor enforcement cycle as a credible smoke-free transition, while bears are skeptical that nicotine pouch share gains can offset cigarette volume declines fast enough to matter.

The signal worth watching is the FDA’s posture on nicotine pouch authorizations. Altria’s on! PLUS was the first product approved under the agency’s fast-track pilot, and management has submitted applications for 6 additional flavors across 3 nicotine strengths, with Gifford asserting the science is “compelling” and should clear the 180-day statutory timeline.

Sustained cigarette volume declines steeper than the current 4% adjusted rate remain the clearest threat to the model, particularly if trade-down pressure from the Iran conflict’s energy cost pass-through persists into the second half.

The Q2 earnings call, expected in late July, will reveal whether the cross-category moderation from illicit e-vapor holds or reverses. The specific figure to watch is the domestic cigarette volume decline rate relative to the current 4% adjusted Q1 read.

What Does the Valuation Model Say?

TIKR’s model puts MO’s mid-case target price at $85, supported by a net income margin assumption of 47.7% over the forecast period and around 2% EPS growth CAGR through 2030.

Against a current price of $72, that implies around 17% total return before dividends, or about a 3.4% annualized IRR excluding the dividend yield.

At 12.63x NTM earnings against a 3-year mean of 9.92x, and with EPS growth guided at only 2.5% to 5.5% for 2026, MO stock is slightly overvalued relative to the pace at which the underlying earnings can grow into the current price.

The investment case hinges entirely on whether the smokeable volume decline stabilizes near current levels or re-accelerates as macroeconomic pressure on lower-income consumers deepens.

The Opportunity / The Risk

Bull case: volume decline moderates structurally.

- Domestic cigarette volumes declined only 2.4% reported and 4% adjusted in Q1, the fourth consecutive quarter of year-over-year sequential improvement.

- Illicit disposable e-vapor market share appears to be plateauing, with Altria estimating the adult vaper count roughly flat year-over-year at around 20.5 million.

- On! PLUS national expansion reached 100,000 stores at launch, and premium retail positioning has been secured at outlets covering approximately 90% of Helix volume.

- Cowboy Cut, a competitively priced Marlboro variant targeting price-sensitive premium smokers, expands distribution in Q2, providing a tool to defend Marlboro’s 59.5% premium segment share.

- Full-year EPS guidance of $5.56 to $5.72 was reaffirmed after a quarter that came in well above expectations, with management now expecting growth to be more balanced between halves.

Bear case: macro and competitive pressures override the positive signals.

- Marlboro retail share declined 1.4 share points year-over-year as consumers traded down to discount, a trend that could accelerate if gas prices from the Iran conflict remain elevated through 2H 2026.

- FDA uncertainty around nicotine pouch authorizations is real: while on! PLUS cleared the pilot, applications for competing brands from PMI and BAT are stalled, and the regulatory environment for additional on! PLUS flavors is not guaranteed.

- The Jefferies $50 price target reflects a scenario where EPS growth stalls and the P/E multiple contracts back toward 10x, which is exactly where the stock sat three months ago.

- NJOY’s e-vapor re-entry remains IP-constrained, and management has signaled no urgency to accelerate that timeline while 70% of e-vapor volume remains illicit.

Should You Invest in Altria Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Altria Group, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Altria Group, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MO stock on TIKR for Free →