Key Takeaways:

- Diamondback Energy (FANG) beat Q1 2026 estimates with $4.24 billion in revenue and raised its full-year production guidance.

- The company boosted its quarterly dividend to $1.10 per share, reflecting strong near-term cash generation.

- FANG stock trades near $200, up around 33% year-to-date and approaching its 52-week high of $215.

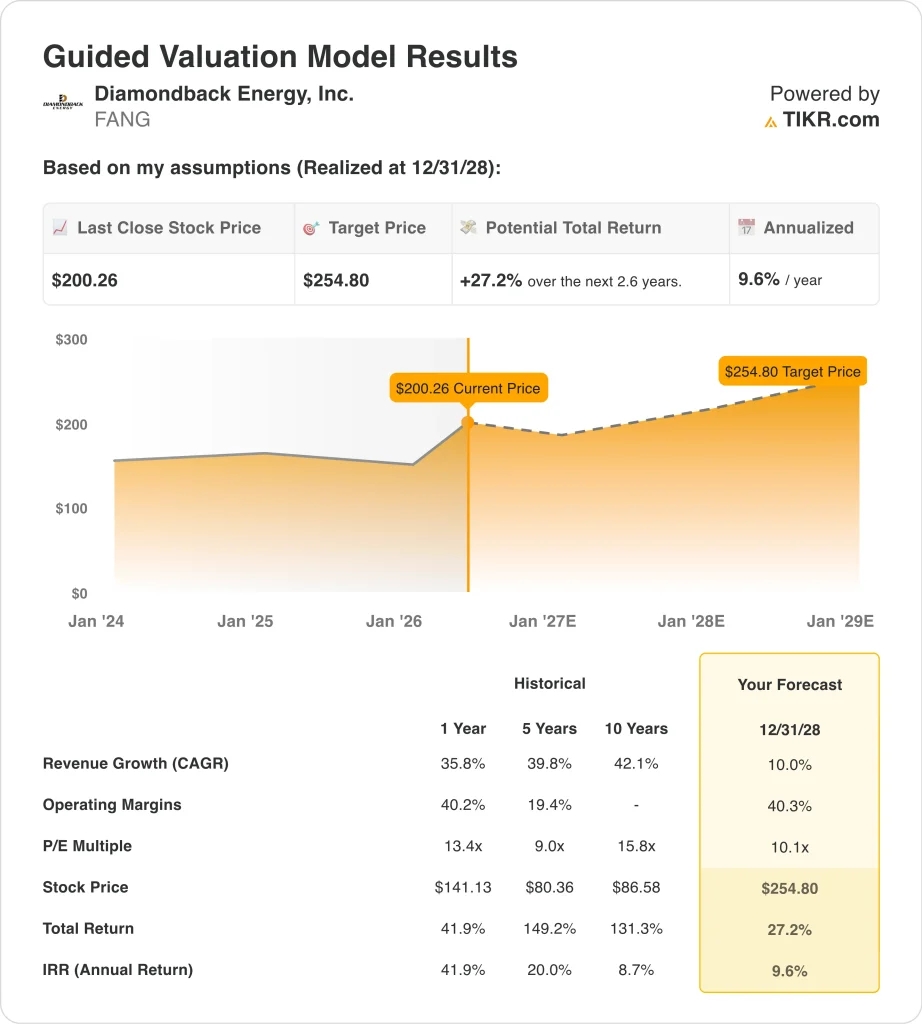

- FANG stock could rise from $200 to around $255 per share by December 2028.

- That implies a total return of around 27%, or around 10% annualized over the next 2.6 years.

What Happened?

Diamondback Energy (FANG) delivered strong first-quarter 2026 results that beat analyst expectations. Revenue came in at $4.24 billion, up 4.7% from the prior year period. Net income turned positive at $25 million, recovering from losses in the year-ago period.

Management raised the quarterly dividend to $1.10 per share, up from $1.05 in the prior quarter. Shares have gained around 33% year to date, and the stock is approaching its 52-week high of $215. Analyst consensus still projects around 15% further upside to the $230 price target.

Diamondback navigated a volatile oil price environment during the first quarter. Iran-related geopolitical tensions drove sharp swings in crude oil prices throughout the period. Energy stocks broadly tracked these oil price movements.

Reuters reported that Diamondback is “betting on a wider WTI-Brent spread,” meaning the company expects U.S. crude oil prices to stay relatively elevated versus international benchmarks. WTI refers to West Texas Intermediate, the main U.S. crude benchmark, while Brent is the global standard.

The company also worked to reduce its debt load, tendering for $777 million in senior notes in April 2026. A lock-up agreement on around 281 million shares also expired on May 10, 2026, creating some near-term selling pressure.

But the year-to-date rally remained broadly intact after the lock-up expiry. Oil price volatility tied to Middle East tensions remains the most significant near-term risk for the stock. Investors in the energy sector will need to monitor geopolitical developments alongside Diamondback’s quarterly production reports.

Diamondback also took portfolio management actions during the period. The company completed an 11 million share secondary offering in March 2026. Its subsidiary, Viper Energy, divested non-Permian Basin assets to sharpen the company’s focus on its most productive acreage.

On the Q4 2025 earnings call, management stated the company should spend more on its existing resources but remains open to future acquisitions. Here’s why Diamondback Energy stock could offer solid capital returns through 2028 as Permian production growth and a growing dividend support overall shareholder value.

What the Model Says for FANG Stock

We analyzed the upside potential for Diamondback Energy stock based on its Permian Basin production trajectory, oil price assumptions, and the company’s consistent capital return discipline.

Based on estimates of 10.0% annual revenue growth, 40.3% operating margins, and a normalized P/E multiple of 10.1x, the model projects Diamondback Energy stock could rise from $200 to around $255 per share.

That would be a 27.2% total return, or a 9.6% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for FANG stock:

1. Revenue Growth: 10%

Diamondback reported Q1 2026 revenue of $4.24 billion, up 4.7% year over year. Management raised its production guidance after the quarter, targeting around 510,000 bpd for 2026. Production volume is the primary driver of revenue for upstream oil companies like Diamondback.

Analysts project a two-year forward revenue CAGR (compound annual growth rate) of around 6.2%. Oil price volatility and Iran-related supply risks create meaningful uncertainty around near-term revenue levels. Revenue is closely tied to WTI crude oil prices, which fluctuated significantly during the first months of 2026.

Based on analysts’ consensus estimates, we used 10.0% annual revenue growth. This is modestly above the near-term consensus, reflecting the potential for higher oil prices and continued production growth to lift revenue. It assumes stable-to-improving crude oil market conditions through 2028.

2. Operating Margins: 40.3%

Diamondback benefits from structurally high operating margins due to its low-cost Permian Basin acreage. Last twelve months’ operating margins were around 40%, and the model uses 40.3% as the forward assumption. Efficient operations allow profitable production across a wide range of oil prices.

Management has focused on reducing costs and improving efficiency across its asset base. The Viper Energy divestiture of non-Permian assets further concentrated the portfolio around its most cost-efficient fields. These structural improvements support sustained high margins through commodity price cycles.

Based on analysts’ consensus estimates, we used 40.3% operating margins. This reflects Diamondback’s track record of disciplined cost management in the Permian Basin. Maintaining these margins through oil price cycles is a key competitive advantage for the company.

3. Exit P/E Multiple: 10.1x

Diamondback trades at a next twelve-month P/E of around 10x. This is a low multiple relative to the broader market but is typical for large U.S. oil and gas producers. Energy companies generally trade at lower multiples because of the commodity-driven and cyclical nature of their earnings.

The company’s $1.10 quarterly dividend provides an additional shareholder return beyond price appreciation. Dividend growth, share buybacks, and debt reduction are all tools management uses to create value even if the stock multiple stays low. A 2.2% dividend yield adds meaningfully to total return potential over a multi-year horizon.

Based on analysts’ consensus estimates, we used an exit multiple of 10.1x. This is roughly in line with current levels, reflecting limited multiple expansion expected for energy producers. Total returns are therefore primarily driven by earnings growth and dividend income rather than a valuation rerating.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

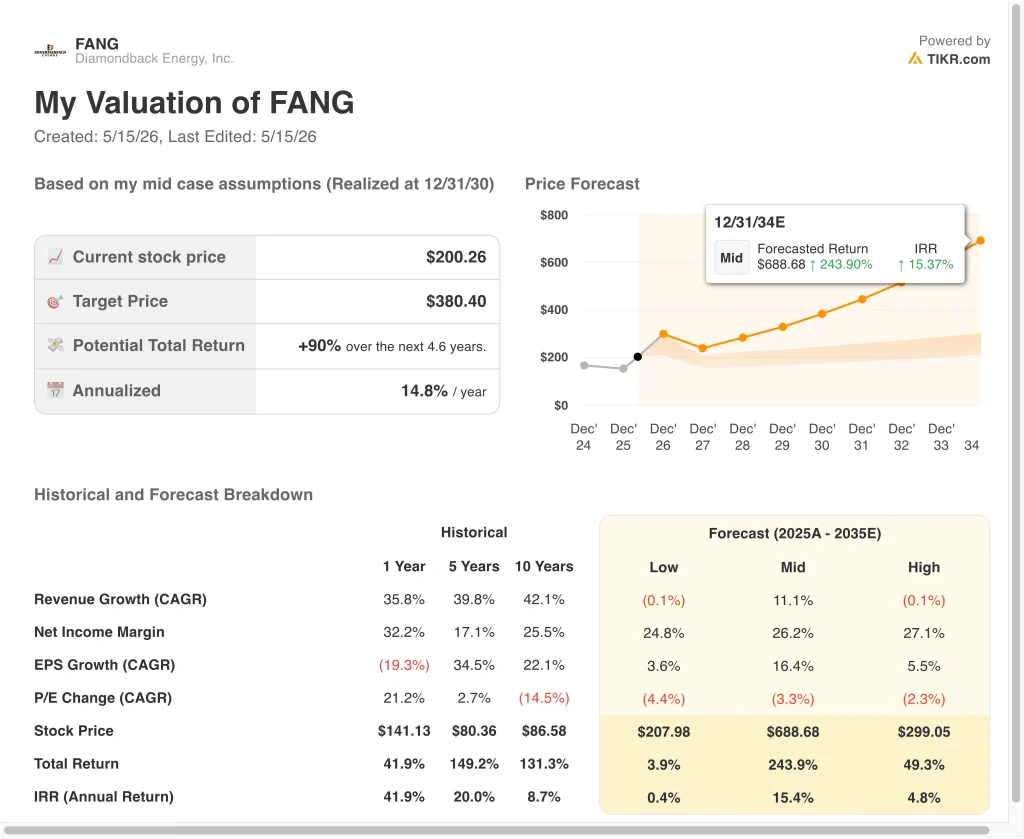

Different scenarios for FANG stock through 2030 show varied outcomes based on oil price levels, Permian Basin production growth, and capital return execution (these are estimates, not guaranteed returns):

- Low Case: Revenue contracts on weaker oil prices and margins stay compressed → 0.4% annual returns

- Mid Case: Production grows steadily at around 11% annually, and oil prices remain supportive → 15.4% annual returns

- High Case: Revenue contracts modestly, but improving margins partially offset the headwind → 4.8% annual returns

Going forward, Diamondback Energy stock will likely move closely with oil prices and its production growth trajectory. The mid case in the model assumes revenue grows around 11% annually, which is the critical driver of meaningful total returns. Investors should monitor WTI crude oil prices and Diamondback’s quarterly production guidance closely through 2028.

See what analysts think about FANG stock right now (Free with TIKR) >>>

Should You Invest in Diamondback Energy?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FANG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FANG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!