Key Takeaways:

- Simon Property Group (SPG) raised its full-year FFO guidance after Q1 2026 net income rose 15.9% to $479.6 million.

- The company is navigating a CEO transition following the passing of founder David Simon; Eli Simon has been named the new CEO.

- SPG stock trades near $203, close to its 52-week high of $208, and yields around 4.5% annually from its dividend.

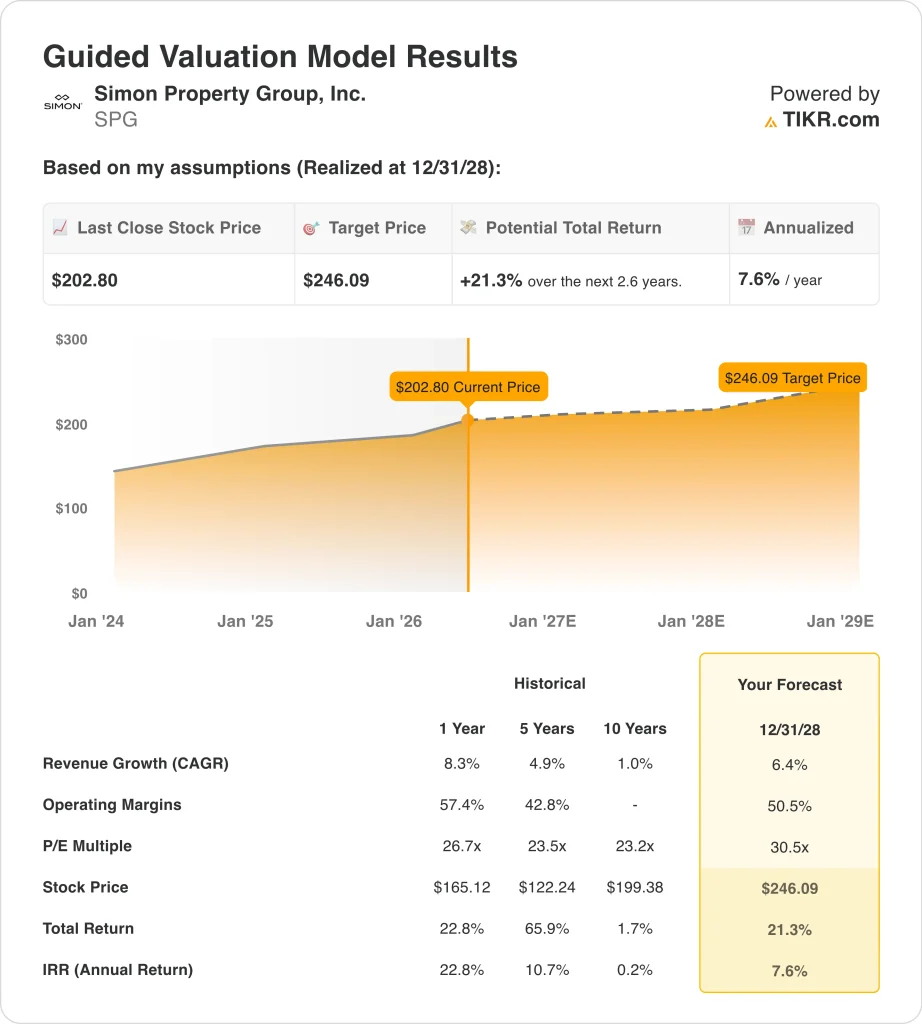

- SPG stock could rise from $203 to around $246 per share by December 2028.

- That implies a total return of around 21%, or around 8% annualized over 2.6 years, not including the dividend yield.

What Happened?

Simon Property Group (SPG) reported first-quarter 2026 net income of $479.6 million, up 15.9% year over year. Real estate FFO per share also rose during the quarter. FFO is the main profit metric for REITs because it adjusts net income for depreciation and other non-cash charges. Management raised full-year FFO guidance, citing steady leasing demand across its premium mall and outlet center portfolio.

Simon Property Group is also managing a major leadership transition. Founder and longtime CEO David Simon passed away on March 23, 2026, at age 64 after a battle with cancer. Eli Simon became the new CEO, while Larry Glasscock was appointed non-executive chairman of the board. First quarter results under the new leadership team showed strong operational continuity and solid execution.

The company also strengthened its capital position and signaled confidence in the stock. Management secured a new $5 billion revolving credit facility in March 2026 and launched a $2.0 billion common stock repurchase program in February 2026. Several directors bought SPG shares in open market transactions in April 2026. SPG’s annual dividend yield of around 4.5% remains a meaningful and consistent contributor to total return.

Here’s why Simon Property Group stock could provide consistent total returns through 2028 as its premium portfolio generates steady leasing income, growing dividends, and modest capital appreciation.

What the Model Says for SPG Stock

We analyzed the upside potential for Simon Property Group stock based on its premium retail real estate portfolio, steady leasing demand trends, and consistent dividend growth history.

Based on estimates of 6.4% annual revenue growth, 50.5% operating margins, and a normalized P/E multiple of 30.5x, the model projects Simon Property Group stock could rise from $203 to around $246 per share.

That would be a 21.3% total return, or a 7.6% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for SPG stock:

1. Revenue Growth: 6.4%

Simon Property Group grew its 2025 annual revenue to $6.36 billion, and portfolio NOI rose 4.7% to $6.1 billion. Management raised its full-year 2026 FFO guidance on the back of steady leasing demand. Premium outlet and mall properties continue to attract quality retail tenants, supporting consistent rental income growth.

Analysts project a two-year forward revenue CAGR of around 7.3%. Simon’s collaboration with digitally-native brands like Bombas, expanding through the Leap and Shopify partnership, shows ongoing retailer demand for premium physical locations. Long-term lease structures and annual rent escalators built into tenant contracts provide consistent revenue visibility.

Based on analysts’ consensus estimates, we used 6.4% annual revenue growth. This reflects SPG’s strong leasing momentum and pricing power in premium retail real estate. Near-term risks include shifts in consumer spending patterns and the potential for retailer stress in a softer economic environment.

2. Operating Margins: 50.5%

Simon Property Group operates with some of the highest REIT margins in its category. The last twelve-month EBIT margin was 48.3%, reflecting efficient management of a large and highly productive property portfolio. Q1 2026 net income growth of 15.9% shows that these already-strong margins are continuing to expand.

High tenant retention rates and long-term leases provide predictable income streams and reduce tenant turnover costs. Premium outlets and malls command materially higher rents than traditional retail real estate, supporting sustainable margin leadership. Operating leverage on a growing NOI base allows margins to improve even with moderate revenue growth.

Based on analysts’ consensus estimates, we used 50.5% operating margins. This reflects gradual expansion from current levels, driven by leasing growth and cost discipline. SPG’s consistent track record of margin management gives confidence in this long-term forward assumption.

3. Exit P/E Multiple: 30.5x

Simon Property Group trades at a next twelve-month P/E of around 30x. For a REIT, this metric is more usefully understood as a P/FFO multiple (Price to Funds from Operations). Premium REITs with strong balance sheets and consistent dividend growth typically command premium multiples relative to the broader real estate sector.

SPG’s 4.5% dividend yield provides an additional return not captured in a price-only model. The company has consistently paid and grown its dividend, and the June 2026 quarterly payment of $2.25 per share continues that track record. Investors in high-quality REITs often value income alongside capital appreciation when assessing total return potential.

Based on analysts’ consensus estimates, we used an exit multiple of 30.5x. This is in line with current levels, assuming the premium mall REIT category maintains its relative valuation over the period. Any meaningful deterioration in retail leasing demand or a significant rise in interest rates could compress the multiple.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for SPG stock through 2030 show varied outcomes based on leasing demand, retail sector health, and NOI growth (these are estimates, not guaranteed returns):

- Low Case: Leasing demand softens, and NOI growth disappoints → 2.2% annual returns

- Mid Case: Portfolio leasing stays steady, and NOI grows in line with historical trends → 4.3% annual returns

- High Case: Premium retail demand strengthens, and NOI growth accelerates meaningfully → 6.1% annual returns

Going forward, Simon Property Group stock will likely deliver returns primarily through its 4.5% dividend yield alongside modest capital appreciation from the price model. The dividend meaningfully boosts total return potential beyond what the price-only projection suggests.

Investors focused on income and steady capital preservation may find SPG’s premium portfolio, growing dividend, and consistent track record compelling through 2028.

See what analysts think about SPG stock right now (Free with TIKR) >>>

Should You Invest in Simon Property?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SPG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SPG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!