Key Stats for RTX Stock

- 52-Week Range: ~$115 to ~$176

- Current Price: $175.68

- Street Mean Target: ~$200

- TIKR Target Price (Mid): ~$210

- TIKR Annualized IRR (Mid): ~4% per year

- Q1 2026 Revenue: $22.1B (up 9% YoY)

- Q1 2026 Adjusted EPS: $1.78 (beat $1.51 estimate)

- FY2026 Adjusted EPS Guidance: $6.70 to $6.90

- FY2026 FCF Guidance: $8.25 to $8.75B

- Total Backlog: $271B

Value your favorite stocks like RTX with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

How RTX Makes Money and What the Powder Metal Issue Actually Was

RTX (RTX) operates two core businesses, as Pratt & Whitney designs and manufactures jet engines for commercial aircraft and military platforms, including the F-35. Collins Aerospace makes avionics, aircraft systems, and defense electronics used on virtually every major commercial and military platform flying today. A third segment, Raytheon, produces missiles, air defense systems, and radar technology for the US military and allied governments globally.

The Powder Metal issue dominated the RTX narrative from 2023 through 2024. A manufacturing defect in a small number of Pratt & Whitney GTF engines required an FAA-mandated inspection and repair program, which pulled hundreds of engines from service and cost significant cash. The charges were real, but the program was finite. By the end of 2025, it was largely behind the company, and the financial results have since reflected that.

See historical and forward estimates for Raytheon stock (It’s free!) >>>

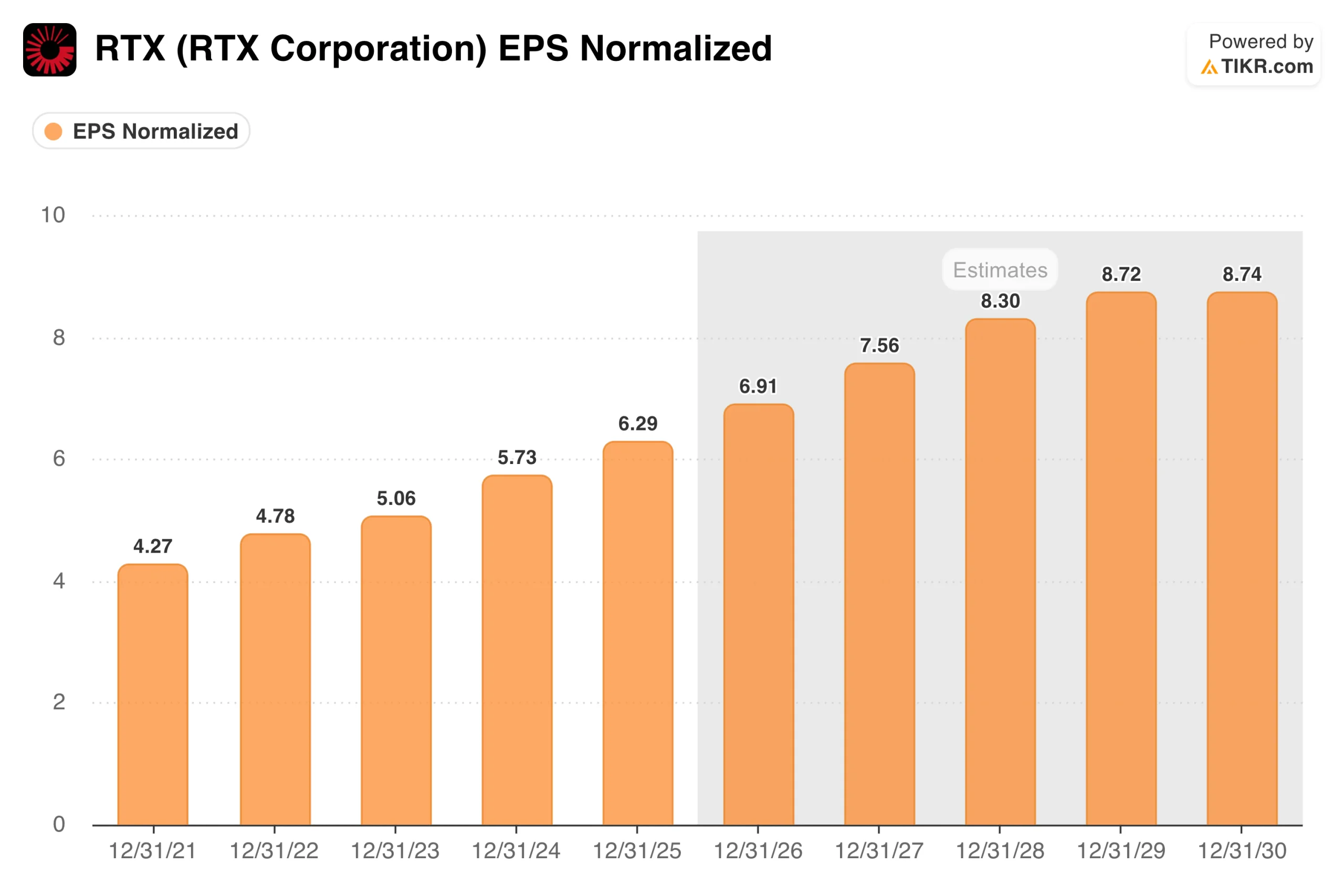

What the EPS Chart Shows About the Underlying Earnings Power

The EPS chart shows something important: the Powder Metal issue barely registered on normalized earnings. Adjusted EPS grew steadily from $4.27 in 2021 through $5.06 in 2023 and $5.73 in 2024, reaching $6.29 in 2025. The charges were real cash costs, but they were largely excluded from the normalized figures that analysts and the company use to evaluate the underlying business.

Consensus projects the compounding continues from here: around $7 in 2026, around $7.50 in 2027, and around $8.30 in 2028. The drivers are durable. Commercial aviation continues to grow, which means more Pratt & Whitney engines on order and more Collins avionics on new aircraft.

Global defense budgets are expanding, with European NATO commitments accelerating and US demand for missile systems showing no signs of slowing. RTX’s current backlog of $271 billion provides years of visibility into contracted revenue behind those estimates.

Why the Free Cash Flow Chart Is the Most Important Visual in This Piece

Free cash flow is where the Powder Metal program actually showed up. RTX generated around $4.9 billion in FCF in 2021 and 2022, then saw it dip to $4.5 billion in 2024 as cash went out the door for inspections, repairs, and customer compensation, before jumping to $7.94 billion in 2025 as the program wound down.

Management confirmed this is not a one-year anomaly. Full-year 2026 FCF guidance is $8.25 to $8.75 billion, implying the 2025 level was the beginning of a new baseline, not a catch-up. RTX raised its 2026 outlook for adjusted EPS to $6.70 to $6.90 while reaffirming free cash flow guidance of $8.25 to $8.75 billion following a strong Q1.

A defense and aerospace business generating $8 to $9 billion in annual FCF at a $175 stock price yields meaningful cash, funding a growing dividend and ongoing buybacks.

See what analysts think about RTX stock right now (Free with TIKR) >>>

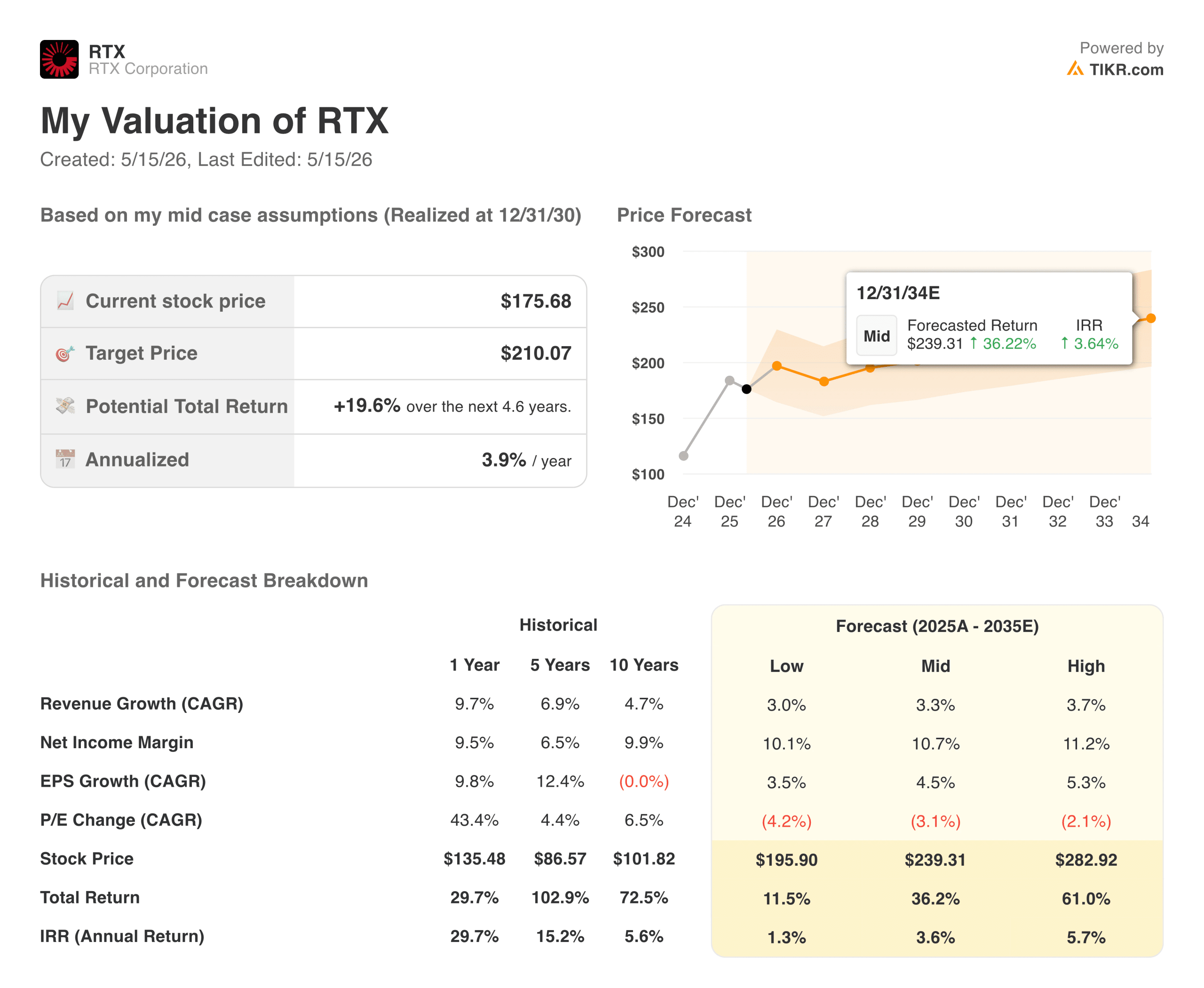

What the TIKR Model Implies at the Current Price

The TIKR model targets around $210 per share in the mid case, implying a total return of roughly 20% over about 4.6 years, or about 4% annually. Revenue growth of around 3% per year, net income margins of around 11%, and EPS growth of around 4.5% are the underlying assumptions.

Like Marriott, this is a situation where the business quality is not in question, but the current price already reflects much of it. The low case targets around $196, barely above where the stock trades today. The high case reaches around $280 at roughly 6% annually. The honest read is that RTX looks fairly valued at the current price, not deeply discounted.

The Case for RTX: Backlog Visibility, FCF Normalization, and Defense Tailwinds

The $271 billion backlog is the foundation of the long-term thesis. That number represents years of contracted revenue, with $162 billion in commercial and $109 billion in defense, giving RTX earnings visibility that most industrial companies cannot match. New awards keep adding to it: the $6.6 billion F135 engine sustainment contract, awarded earlier this year, is one of many multi-year programs that extend the revenue runway.

Defense spending is structurally growing across NATO. European allies are rebuilding inventories, the Middle East is expanding air defense capabilities, and the US is investing in next-generation radar and missile systems where RTX holds leading positions. The dividend has been raised consistently, and the FCF recovery funds continue to return capital.

The Risks: Fixed-Price Contracts, Tariff Exposure, and a Modest Return Profile

Defense contractors live on execution. Fixed-price contracts mean cost overruns come directly out of RTX’s margin. Collins Aerospace has navigated this with discipline, but it remains a structural risk on any new program award.

Tariff exposure is a near-term concern as well. CEO Hayes cited tariffs, supply chain disruptions, and geopolitical risks as key challenges heading into the back half of 2026, with some pressure already visible in Q1.

And the valuation is the honest risk. A mid-case return of 4% annually means the market needs flawless execution just to reach the model target. There is not much cushion for disappointment at the current price.

Is RTX Worth Buying at $176?

RTX is a high-quality aerospace and defense business with a massive backlog, accelerating free cash flow, and durable demand on both sides of its portfolio. The Powder Metal overhang that defined the past two years is effectively resolved. EPS compounding from $6.29 toward an estimated $8.30 by 2028 reflects real earnings growth, and $8 to $9 billion in annual FCF is a compelling cash generation profile at any price.

The question is whether that profile justifies the current multiple. The TIKR model says the stock is close to fair value, with mid-case upside of around 20% over 4.6 years. For investors seeking quality defense and aerospace exposure, with a growing dividend and clear earnings visibility, RTX is a reasonable hold.

For investors looking for a meaningful discount to intrinsic value, the numbers suggest the better entry was a year ago, when the stock was closer to $135.

See analysts’ growth forecasts and price targets for RTX stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!