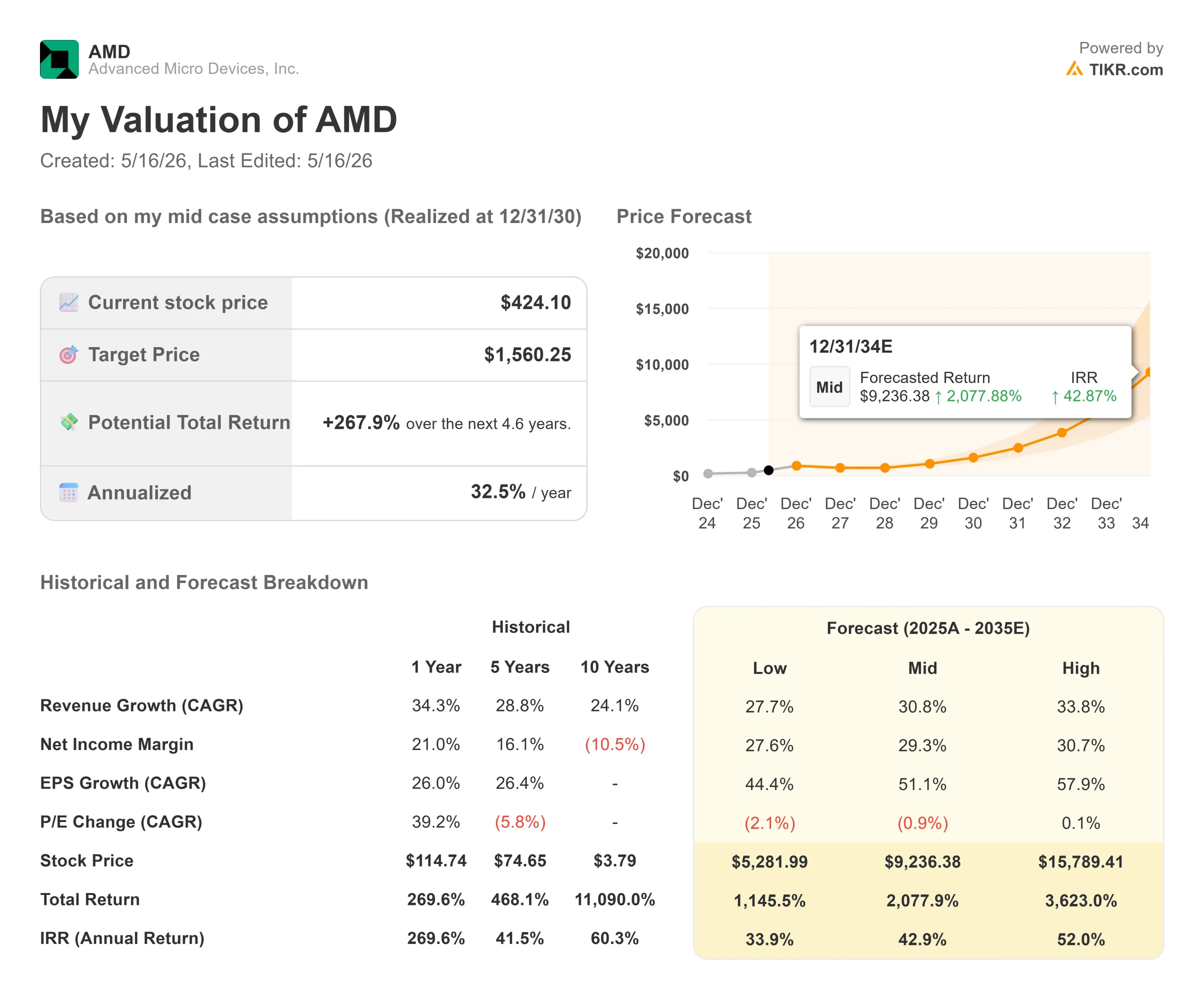

Key Stats for AMD Stock

- Current Price: $424.10

- Target Price (Mid): ~$1,560

- Street Target: ~$458

- Potential Total Return: ~268%

- Annualized IRR: ~33% / year

- Earnings Reaction: +18.61% (5/5/26)

- Max Drawdown: -27.76% (3/3/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Advanced Micro Devices (AMD) just delivered one of the most significant forecast revisions in recent semiconductor history, and investors focused only on the GPU story are missing the bigger trade.

On the May 5 earnings call, CEO Dr. Lisa Su told analysts that AMD now expects the server CPU total addressable market (TAM, the total revenue opportunity for companies selling data center processors) to grow at greater than 35% annually and reach over $120 billion by 2030. That is more than double the $60 billion TAM AMD projected at its Financial Analyst Day just six months earlier. The driver is agentic AI (AI systems that autonomously execute multi-step tasks requiring massive CPU compute), which is reshaping the architecture inside every major data center.

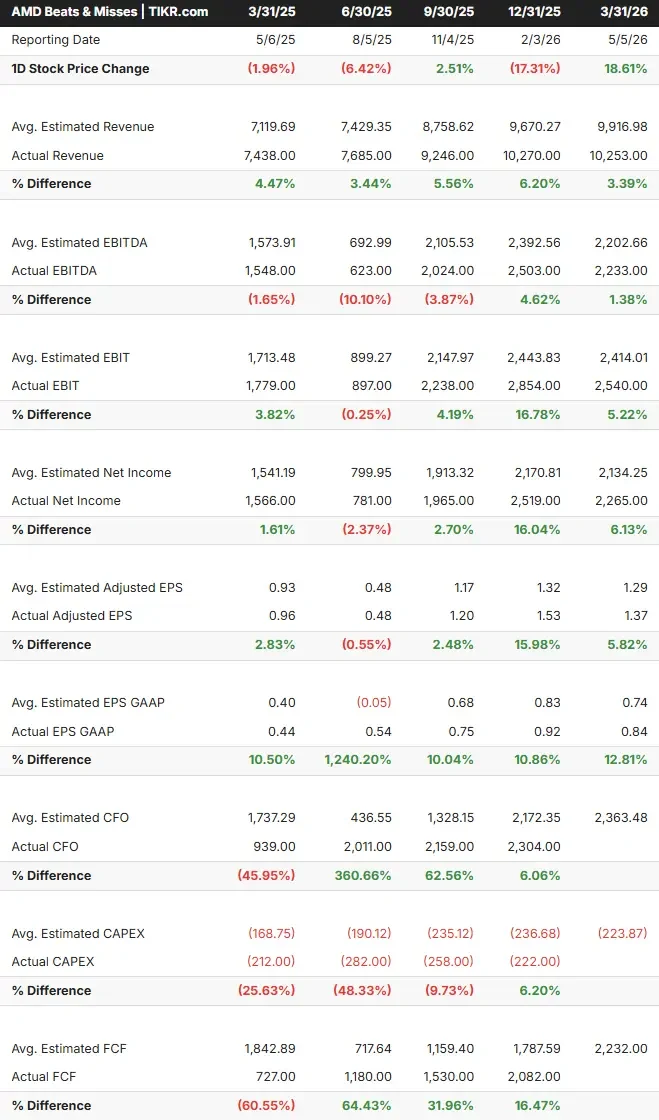

AMD surged 18.61% on May 6 after the Q1 report and has climbed more than 110% year to date. The central question is whether the earnings growth that justifies the move has arrived, or is still coming. Per the TIKR data, most of it ships in the second half of 2026.

Why Agentic AI Is the CPU Supercycle Nobody Expected

The dominant narrative heading into 2026 was that AMD had to prove itself in AI accelerators. What happened instead was structurally more significant.

As AI agents scale across cloud and enterprise, they require CPUs for orchestration, data movement, and parallel execution in addition to GPU acceleration. The CPU-to-GPU ratio inside a deployed data center, historically around 1:4 or 1:8, is now moving toward 1:1. In extreme agent-dense configurations, Su said on the call, you could see more CPUs than GPUs.

“Over the last few months, as we’ve talked to our customers and we’ve seen how AI adoption is really unfolding, we’re seeing significant more CPU demand from really every major cloud provider as well as enterprise customers,” Su said. The revision came from the order books, not a top-down macro assumption.

AMD’s EPYC server CPU business grew more than 50% year over year in Q1 2026, with cloud and enterprise each growing more than 50% individually. The company has delivered four consecutive quarters of record server CPU revenue, and management is guiding server CPU growth of more than 70% year over year in Q2, with strong growth continuing into 2027.

Looking ahead, AMD’s next-generation EPYC Venice processor, built on 2-nanometer process technology, is on track to launch later this year. It includes Verano, AMD’s first EPYC CPU purpose-built for AI infrastructure, and management described customer validation momentum as stronger than any prior EPYC generation at the same stage.

See historical and forward estimates for AMD stock (It’s free!) >>>

The GPU Ramp

Data Center AI GPU revenue was down modestly on a sequential basis in Q1, entirely because of lower China revenue following export control restrictions that had boosted Q4 2025 sales. Strip out the China transition, and the underlying GPU business was growing. Management guided Data Center AI to double-digit sequential growth in Q2.

The more important signal is MI450 and Helios. Helios is AMD’s rack-scale AI platform, combining Instinct MI450 GPUs with sixth-generation EPYC Venice CPUs into a single integrated infrastructure unit. AMD has begun sampling MI450 GPUs to lead customers, with production starting in Q3 2026 and a significant ramp in Q4.

One detail stands out: MI450 customer forecasts are already exceeding AMD’s initial plans. “Lead customer forecasts now exceeding our initial plans and a growing number of new customers engaging on large-scale deployments, including additional multi-gigawatt opportunities,” Su said. That gives AMD what it calls “strong and increasing confidence” in delivering tens of billions of dollars in annual Data Center AI revenue in 2027.

Two anchor partnerships frame the scale. AMD and OpenAI have a multi-year agreement for 6 gigawatts of Instinct GPU deployments, with the first gigawatt of MI450 GPUs scheduled for H2 2026. AMD and Meta Platforms have an expanded agreement to deploy up to 6 gigawatts of Instinct GPUs across multiple generations, including a custom GPU co-designed on the MI450 architecture, also shipping in H2 2026.

Balance Sheet and Recent Moves

Q1 2026 produced record free cash flow of $2.6 billion, equal to 25% of revenue, on $3 billion in cash from operations. AMD ended the quarter with $12.3 billion in cash and short-term investments, a net cash position of approximately $8.5 billion (per TIKR’s LTM Net Debt of negative $8,476 million), and $9.2 billion remaining on its buyback authorization after repurchasing 1.1 million shares in Q1.

On May 14, 2026, AMD secured a new five-year, $5 billion unsecured revolving credit facility led by JPMorgan Chase, replacing its 2022 agreement and adding financial flexibility as the Helios ramp scales.

Q1 gross margin was 55%, up 170 basis points year over year. AMD guided Q2 gross margin to approximately 56%. MI450 GPU shipments will carry below-corporate-average margins in the second half, but AMD’s long-term gross margin target remains 55% to 58%, and management sees the server CPU mix strength, declining gaming revenue, and Embedded recovery as offsetting tailwinds.

Beyond the data center, Client and Gaming revenue grew 23% year over year to $3.6 billion. Client alone grew 26% to $2.9 billion, driven by Ryzen AI 400 series processors and commercial PC share gains. AMD expects client revenue to grow year over year, even as it plans for softer second-half demand from higher memory costs. Embedded returned to growth at $873 million, up 6% year over year.

On valuation multiples, AMD trades at 41.66x NTM EV/EBITDA, compared to Broadcom at 24.86x and ASML at 29.35x, per TIKR’s Competitors page. At 48.80x NTM P/E, the valuation is pricing in execution, not hope. The Street mean target is approximately $458, implying about 8% near-term upside from current levels, with 36 Buys, 4 Outperforms, and 11 Holds among covering analysts.

See how AMD performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $424.10

- Target Price (Mid): ~$1,560

- Potential Total Return: ~268%

- Annualized IRR: ~33% / year

See analysts’ growth forecasts and price targets for AMD stock (It’s free!) >>>

The mid-case model’s two revenue drivers are EPYC server CPU share gains inside a TAM AMD now pegs above $120 billion by 2030, and the Instinct MI450 ramp through contracted pipelines with Meta and OpenAI. The margin driver is mix shift: as Data Center revenue (which ran a 28% operating margin in Q1 2026) grows as a share of the total, operating leverage expands toward a net income margin of approximately 29%.

The upside path requires clean Helios execution in H2 2026, MI450 customer base expansion beyond the two anchor partners, and Venice launching on schedule. If those lands, the model’s high-case IRR of approximately 52% is credible. The primary risk is specific: a Helios ramp delay, a pause in hyperscaler AI capex, or tighter export controls would pressure both the 2026 and 2027 estimates, on which the current multiple depends.

The TIKR model’s mid-case target of approximately $1,560 sits well above the Street’s approximately $458 mean because the model runs to 12/31/30, capturing the full earnings ramp. Near-term analyst targets and a 5-year model answer different questions. Both are worth understanding.

Conclusion

The single catalyst to watch is the Helios production ramp in Q4 2026. Management guided initial volume in Q3 and a significant acceleration in Q4. When AMD reports Q2 results on August 4, 2026, the most important data point will be Q3 Data Center AI guidance. Sequential acceleration from Q2 confirms that contracted demand with Meta and OpenAI is converting to recognized revenue. A flat or declining Q3 guide is the warning sign.

The TAM revision came from customer conversations, not from a macro model. Named hyperscalers, CPU-to-GPU ratios moving toward 1:1, and multi-year capacity planning discussions are what drove it. Whether AMD’s stock rewards that signal depend on what ships between now and December 31.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in AMD?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMD, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AMD alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!