Key Stats for Home Depot Stock

- Current Price: $297.51

- Street Target (Mean): ~$401

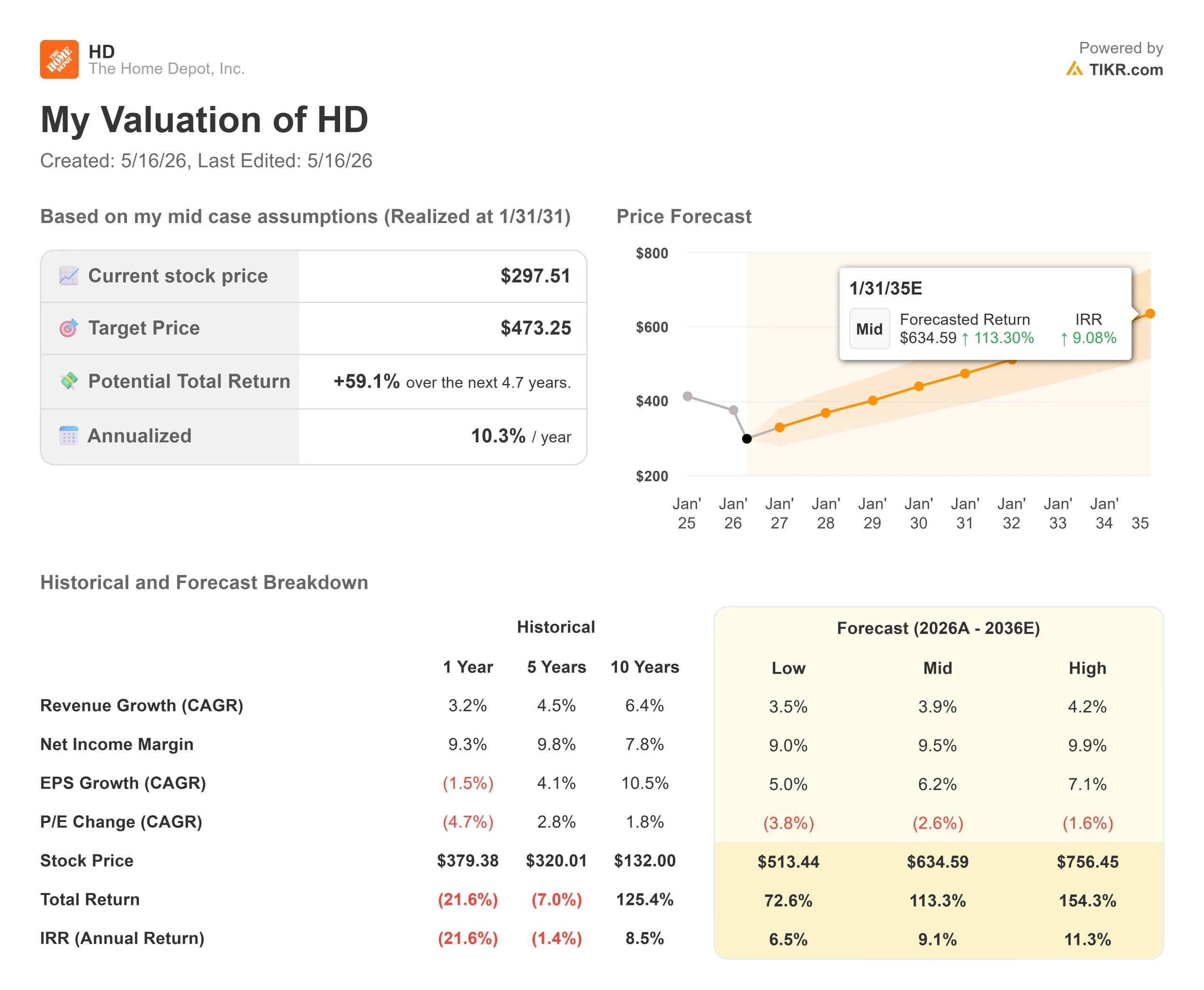

- TIKR Target Price (Mid): ~$473

- Potential Total Return: ~59%

- Annualized IRR: ~10% / year

- Earnings Reaction: -2.32% (2/24/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

The Home Depot (HD), the world’s largest home improvement retailer, is trading near its lowest price in over two years. From its 52-week high of $426.75, HD has fallen nearly 30% to $297.51. The slide has not come from a single bad quarter. It has been built over months of a U.S. housing market that refuses to move.

The pressure accelerated this week as analysts trimmed targets ahead of Q1 fiscal 2026 earnings on May 19. Truist Financial cut its price target from $424 to $394, maintaining a Buy rating while flagging macroeconomic and housing headwinds. Citi separately lowered its target from $450 to $400, also keeping a Buy. Nobody abandoned the thesis. Both firms are resetting near-term expectations while holding long-term conviction. The question worth asking now: Is a stock down nearly 30% from its peak finally pricing in enough pain?

What the Housing Freeze Actually Means

CFO Richard McPhail addressed this directly at the J.P. Morgan Retail Roundup Forum in April. U.S. existing home sales have been stuck near 3% of all homes changing hands for nearly four years, well below the historical 4% to 5% norm. “We have never seen housing activity this slow for this long,” McPhail said.

The critical nuance: this is a confidence problem, not a balance sheet problem. Homeowners have seen home equity values rise 80% to 90% over six years. Employment is full. Incomes are growing. McPhail described what Home Depot’s professional contractors hear from clients: “It’s not that I don’t have the ability to spend. It just doesn’t feel like the right time.” That separates deferred demand from destroyed demand, and it matters for how this eventually resolves.

The pressure is concentrated in large discretionary projects like kitchen renovations, flooring, and lighting. Smaller repair and maintenance spending has held up, which is why HD posted positive U.S. comparable sales for five consecutive quarters through Q4 fiscal 2025.

See historical and forward estimates for Home Depot stock (It’s free!) >>>

The Acquisition Nobody Is Talking About

On May 11, SRS Distribution, a wholly owned Home Depot subsidiary, completed the acquisition of Mingledorff’s, a leading wholesale HVAC (heating, ventilation, and air conditioning) equipment distributor with 42 locations across five southeastern states. The deal adds HVAC distribution as a new vertical for SRS and expands Home Depot’s total addressable market to $1.2 trillion, with HVAC alone representing approximately $100 billion of that figure.

Mingledorff’s is SRS’s fifth vertical, alongside roofing, pool, landscape, and wallboard through GMS. A specialty contractor dealing with a roofing job that uncovers HVAC problems can now source both through a single distributor relationship, backed by jobsite delivery, outside sales reps, and trade credit. McPhail called HVAC “a fantastic vertical” that the company had been planning since before acquiring SRS. The stock barely moved on the close. The market was focused on Tuesday’s earnings print. But this deal is directly relevant to the long-term thesis: SRS now covers more of the professional contractor’s project spend than any competitor can match through a single relationship.

Is the Valuation Finally Cheap?

At $297.51, HD trades at 14.11x NTM EV/EBITDA, down from 16.59x a year ago. Peers with no housing exposure trade at a significant premium on the same metric: TJX Companies sits at 19.24x and Ross Stores at 19.19x, per TIKR’s Competitors page. That roughly 5-turn discount reflects the housing cycle, not a structural disadvantage.

The Street target mean of $401.39 implies around 35% upside from current levels, and 22 of 33 covering analysts carry a Buy or Outperform rating on the stock.

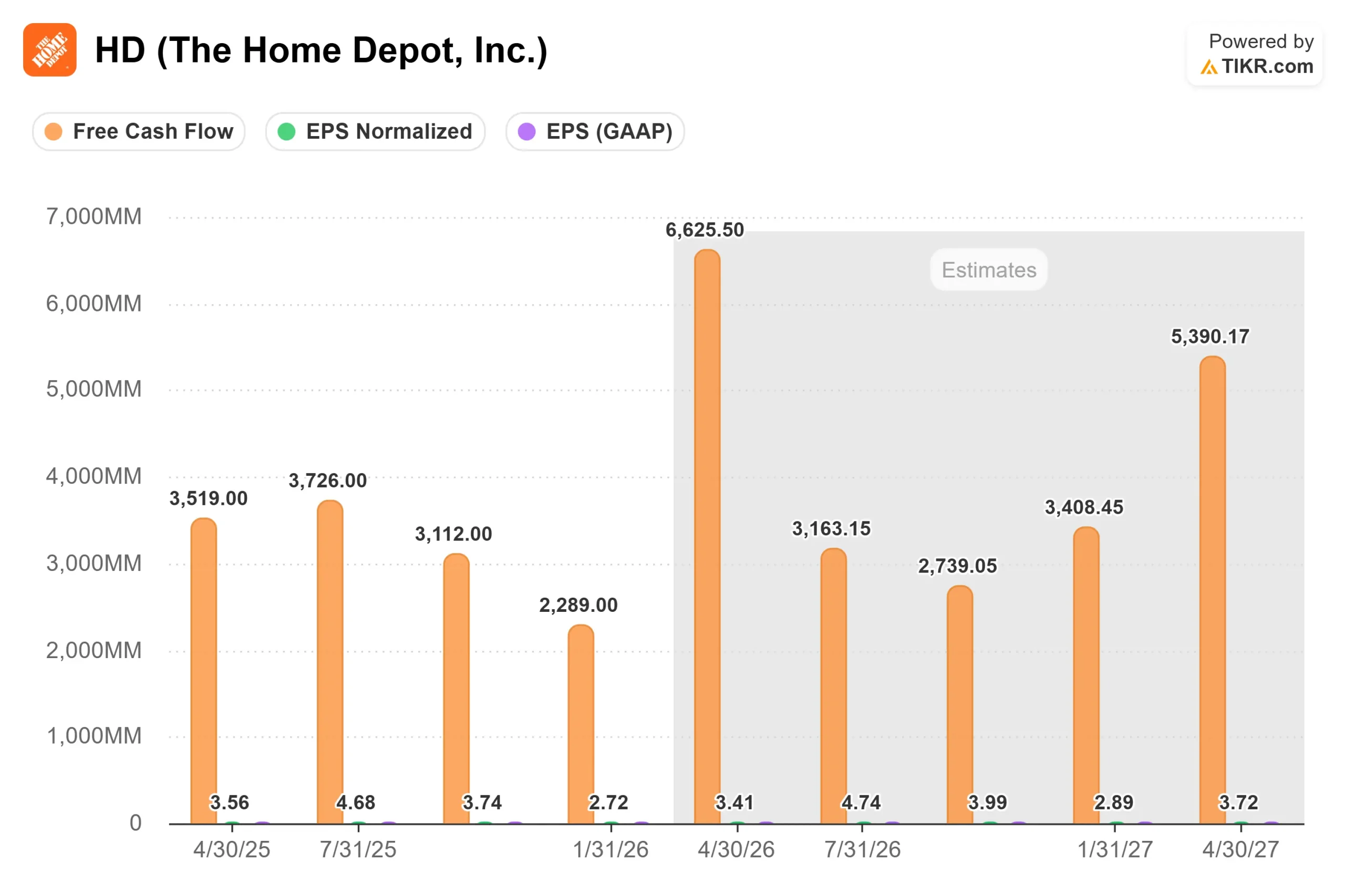

Near-term earnings are under pressure. Analysts expect Q1 fiscal 2026 EPS of $3.41, a 4.2% decline year over year, with revenue forecast to grow around 4.2% to $41.5 billion. Management had already guided for the first-half EPS to be negative year over year due to GMS acquisition annualization effects, so a decline is expected. Full-year fiscal 2026 guidance calls for flat to 4% EPS growth off the $14.69 reported in fiscal 2025. Free cash flow came in at $12.6 billion for fiscal 2026, and TIKR estimates point to recovery toward around $16 billion by fiscal 2028 as those headwinds roll off. The 3.1% dividend yield, supported by current cash flow levels, provides a floor for income-oriented holders.

See how Home Depot performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $297.51

- Target Price (Mid): ~$473

- Potential Total Return: ~59%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Home Depot stock (It’s free!) >>>

The mid-case TIKR model assumes a revenue CAGR of around 4%, driven by continued Pro ecosystem expansion through SRS and gradual recovery in big-ticket renovation demand as housing turnover normalizes. Net income margin is modeled at around 9.5%, consistent with gross margin stability and modest operating leverage as the GMS acquisition headwind clears. This is not a boom scenario. It assumes steady share gains in a recovering market, nothing more.

If housing turnover moves back toward historical norms, Home Depot’s own Investor Day framework points to 4% to 5% comp sales, 5% to 6% total revenue growth, and EPS expanding faster than revenue. That case would put earnings power well above the current consensus. The low-case TIKR model, which assumes a slower recovery and tighter margins, targets approximately $513 by 1/31/31. The primary downside risk is that consumer uncertainty deepens, large project deferrals become cancellations, and SRS integration costs weigh on margins before the cross-sell revenue materializes.

Conclusion

Tuesday’s Q1 earnings call is the first hard data on the spring selling season. Watch U.S. comparable sales against the flat-to-2% full-year guidance range and whether management holds or cuts its EPS guide. A print at or above the midpoint with guidance intact gives the stock a credible catalyst to recover from current levels. A guidance cut likely sends HD toward the low $280s.

For longer-horizon investors, the setup is cleaner. At roughly 14x forward EBITDA with a $700 billion Pro market still largely uncaptured, a 3.1% dividend yield, and a TIKR mid-case pointing to around 59% total return by 1/31/31, the stock is pricing in a lot of bad news. The housing cycle will eventually turn. The question is whether the current price already pays you enough to wait.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Home Depot?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Home Depot, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Home Depot alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Home Depot on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!