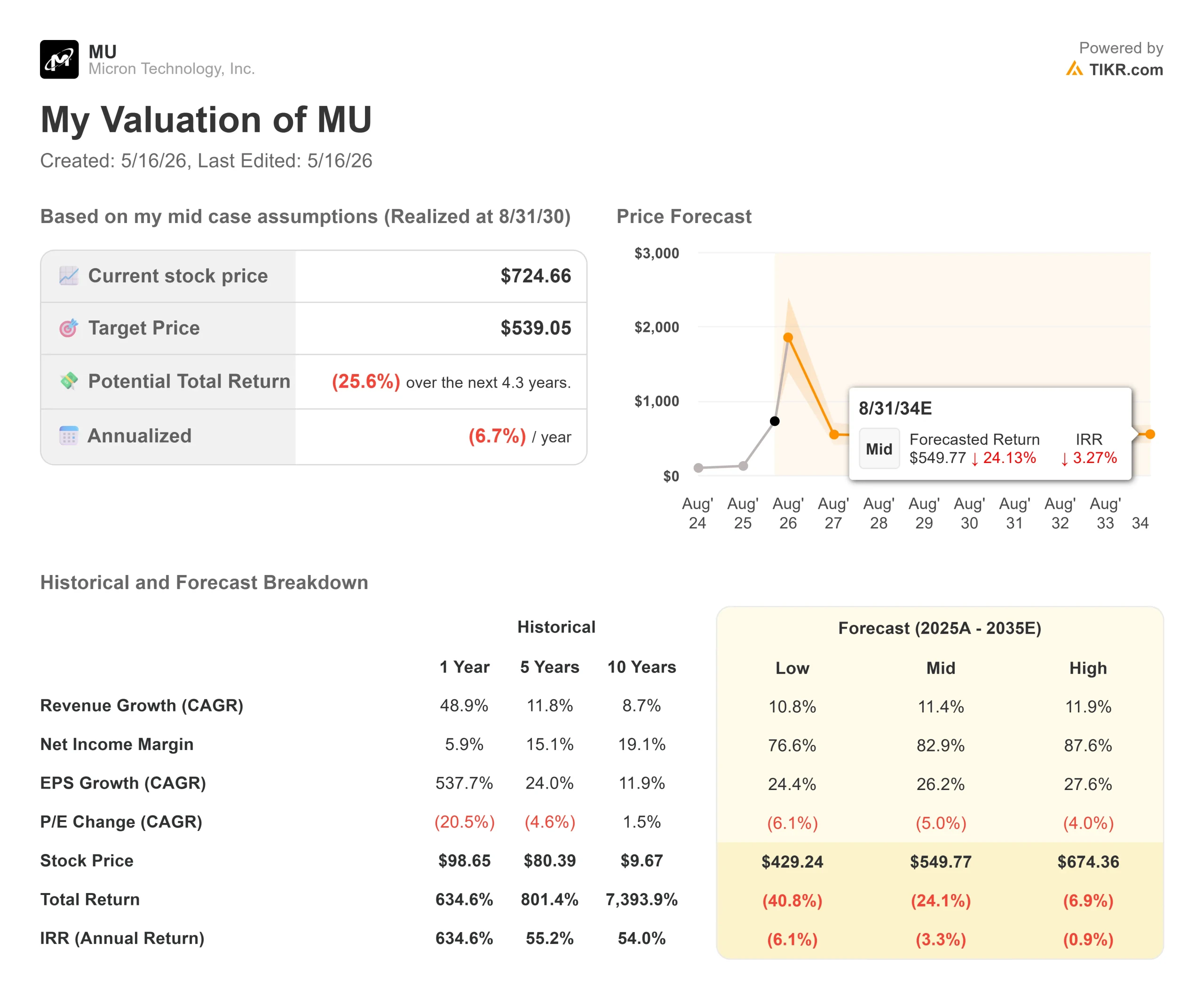

Key Stats for Micron Stock

- Current Price: $724.66

- Target Price (Mid): ~$539

- Street Target: ~$584

- Potential Total Return: ~(26%)

- Annualized IRR: ~(7%) / year

- Earnings Reaction: (3.78%) on March 18, 2026

- Max Drawdown: 30.31% on March 30, 2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Micron Technology (MU) hit $818.67 this week, an all-time high, then gave back 11% in three sessions. For a stock that sat at a 52-week low of $90.93 just twelve months ago, that kind of turbulence at the top is either a normal exhale after a nearly 700% run, or a signal the market has gotten ahead of the fundamentals. The answer depends on a question Micron’s own management admitted it cannot yet answer with confidence: when does memory supply finally catch up to AI demand?

That tension sits at the center of the most aggressive analyst repricing in semiconductors this year. Deutsche Bank and DA Davidson each set $1,000 price targets this week. Bank of America raised its target to $950 after lifting its estimate of the 2030 AI data center total addressable market to approximately $1.7 trillion. The Street consensus per TIKR sits at approximately $584. The TIKR mid-case model implies a target of ~$539 and a negative total return. That gap between the bull case and the model is what this article addresses.

How MU Got Here

The move has been extraordinary. Micron climbed from a 52-week low of $90.93 to an all-time high of $818.67, a nearly sevenfold gain in twelve months. It did not travel in a straight line. The stock surged into March earnings, fell 3.78% on the day results were reported despite Q2 revenue of $23.86 billion nearly tripling year-over-year, and then crashed to a max drawdown of 30.31% by March 30 as a Google Research compression algorithm rattled the AI memory trade. It then more than doubled from that trough through mid-May as analysts rebuilt their models around structurally higher demand.

What changed the narrative? Investors concluded this is not just a cycle. Chief Business Officer Sumit Sadana told analysts on Micron’s March 19 post-earnings call that demand for its Gen6 SSD is something the company is “not able to completely even come close to meeting.” On high-bandwidth memory (HBM), a specialized type of DRAM that sits alongside AI processors to deliver data at extreme speeds, he confirmed that pricing locked in late 2025 for calendar 2026 carried “robust ROI and profitability,” and that upside supply volumes since then have been sold at “even more robust levels of pricing.” The fiscal 2026 numbers may still be understating Micron’s current pricing power.

See historical and forward estimates for Micron stock (It’s free!) >>>

What the Q2 Call Reveals That Headlines Missed

The post-earnings press cycle focused on the $23.86 billion revenue headline and Q3 gross margin guidance of approximately 81%. But the post-earnings analyst call contained details that deserve more attention.

On NAND, Manish Bhatia, EVP of Global Operations, confirmed that Micron is expanding cleanroom space at an existing Singapore site, not a new greenfield location, driven by technology transition requirements and a decision to co-locate NAND R&D closer to manufacturing. Sadana added that the new Singapore capacity will not contribute meaningful supply until the second half of 2028. NAND’s undersupply window stretches as far as DRAM.

On capital and costs, CFO Mark Murphy confirmed that the Idaho and Tongluo (Taiwan) facilities will not produce meaningful revenue-contributing supply until Micron’s fiscal 2028. The fiscal 2026 capital expenditure plan rose to over $25 billion, up from the prior $20 billion guidance. Start-up costs from both sites are expected to add roughly $100 million to $200 million per quarter beginning Q3 FY2026, and fiscal 2027 operating expenses are projected at approximately a $1.7 billion quarterly run rate. These are real near-term costs landing against a stock price that has already priced in the upside.

On HBM yield, Bhatia said HBM4 is tracking “an even faster yield ramp than HBM3E 12-high.” Better yield means lower cost per bit, which provides a structural floor under margins even if pricing eventually normalizes.

The Competitor Picture

Per TIKR Competitors data, SK Hynix trades at an NTM EV/EBITDA of 3.80x against Micron’s 5.94x, and an NTM P/E of 5.57x against Micron’s 7.81x. Micron trades at a meaningful premium to its closest AI memory peer, reflecting its status as the only U.S.-domiciled advanced memory manufacturer and Wall Street’s growing conviction that this cycle is structural. Whether that premium holds depends on whether Micron sustains the gross margins embedded in current consensus estimates.

See how Micron performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $724.66

- Target Price (Mid): ~$539

- Potential Total Return: ~(26%)

- Annualized IRR: ~(7%) / year

See analysts’ growth forecasts and price targets for Micron stock (It’s free!) >>>

The TIKR mid-case model uses an approximately 11% revenue CAGR from fiscal 2025 through fiscal 2030, with net income margins modeled at around 83%. Even under those favorable assumptions, the model implies a negative total return of approximately 26% from $724.66, with an annualized IRR of roughly negative 7% per year through 8/31/30. That is not a forecast of collapse. It is the model saying the stock has priced in a great deal of good news already.

The upside path requires Micron to sustain gross margins in the mid-to-high 70s through the next several years, the point at which multiple compression assumptions break down. HBM4’s faster-than-expected yield ramp, confirmed by Bhatia on the Q2 call, supports that possibility by keeping cost per bit falling even as pricing eventually moderates.

The downside path is the classic memory playbook: new greenfield DRAM capacity from multiple players arriving simultaneously around fiscal 2028, coinciding with a potential demand air pocket. Murphy acknowledged this risk directly, capital expenditure “could go down after ’27, but we’re not making that call.” A $25 billion-plus CapEx commitment for fiscal 2026 alone means this investment is being made before anyone can confirm demand sustains.

Of 46 analysts covering MU, 30 rate it Buy and 9 Outperform, but the Street’s mean target of ~$584 sits well below the current price of $724.66. The divergence reflects a genuine valuation debate: has Micron structurally escaped the memory cycle, or has the cycle simply not arrived yet?

Conclusion

The single most important data point for MU investors over the next 90 days is the Q3 fiscal 2026 gross margin, expected around June 24, 2026. Management guided approximately 81%. At or above that level, HBM pricing power is intact and the near-term cost headwinds are being absorbed cleanly. Below 80%, the gap between the TIKR model and the stock price gets much harder to defend.

Sadana’s own words on the Q2 call carry more weight than any price target: Micron does not yet have a “high confidence view” on when supply catches up to demand. That uncertainty is why the stock can trade at $724 today and fall from $818 to $724 in three sessions. Watch the June gross margin.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Micron?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Micron, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Micron alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!