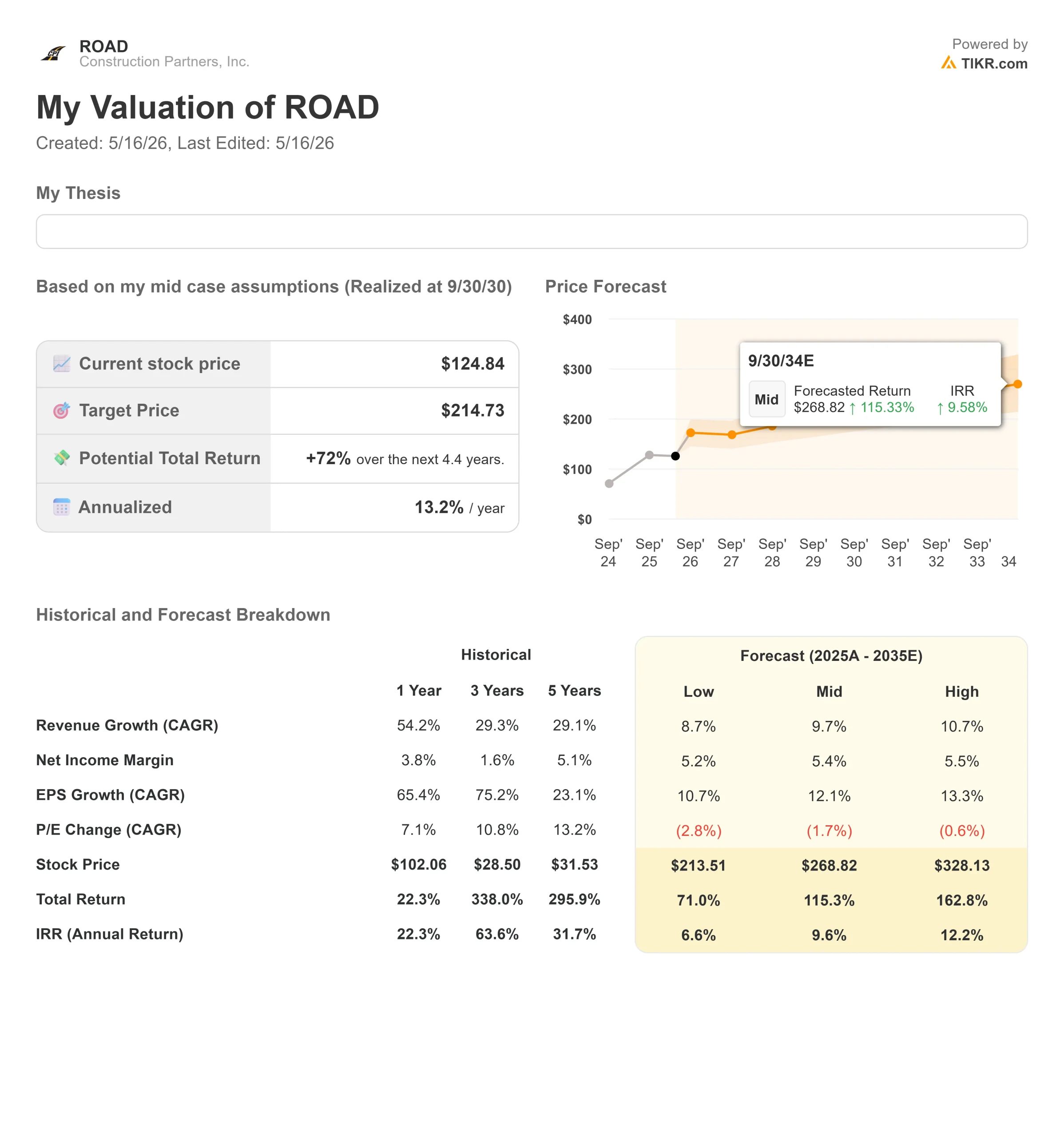

Key Stats for Construction Partners Stock

- Past-Week Performance: -5%

- 52-Week Range: $93 to $151

- Valuation Model Target Price: Around $215

- Implied Upside: About 70%

Analyze your favorite stocks like Construction Partners with TIKR (It’s free) >>>

What Happened?

Construction Partners, Inc. stock fell about 5% this week, finishing near $118 per share as investors reassessed the stock after a strong post-earnings run. ROAD had already traded near the high end of its 52-week range, so the pullback looked less like a reaction to weak fundamentals and more like profit-taking after a big rally.

The stock moved lower because the market appeared to treat ROAD’s strong quarter as already priced in, not as a fresh catalyst. The company raised guidance, grew backlog, and showed strong acquisition momentum, but the stock had already rallied toward the high end of its 52-week range before the pullback. That created a higher bar for the earnings update, especially because ROAD still trades at a premium valuation for an infrastructure contractor.

When a stock is priced for strong execution, even good results can lead to selling if investors start questioning whether the next leg of upside will require faster backlog conversion, stronger margins, or more acquisition-driven growth than the market already expected.

On its May 8 earnings call, Construction Partners showed the business is still gaining momentum, with revenue up 35% year over year to $769 million, adjusted EBITDA up 35% to $93 million, and backlog reaching a record $3.14 billion, covering about 80% to 85% of the next 12 months of contract revenue.

CEO Jule Smith said the company is “executing on a record backlog,” helped by strong public infrastructure demand, commercial projects, data center work, and recent acquisitions including Four Star Paving.

Analyst, institutional, and peer context added more depth to the move. Robert W. Baird raised its price target on ROAD to $169 from $129 and kept an Outperform rating, showing that some analysts still see upside after the Q2 report.

At the same time, recent institutional updates were mixed, with some holders trimming positions while others added exposure. ROAD also competes in the infrastructure and construction materials market alongside Granite Construction, Sterling Infrastructure, Vulcan Materials, Martin Marietta, and CRH, which makes backlog conversion, margins, and acquisition execution important as investors compare ROAD’s growth profile against larger and more diversified peers.

Value Construction Partners instantly (Free with TIKR) >>>

Is ROAD Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth: Around 10%

- Net Income Margin: Around 5%

- EPS Growth: Around 12%

Revenue growth is the main driver of the ROAD setup. The model shows revenue rising from about $3.6 billion in fiscal 2026 to about $6.0 billion by fiscal 2030, supported by Sunbelt population growth, public infrastructure spending, acquisitions, and steady demand for road construction in high-growth markets.

The near-term setup has strong visibility. Construction Partners ended Q2 with a record $3.14 billion backlog, covering about 80% to 85% of the next 12 months of contract revenue, while Four Star Paving expands its commercial paving presence in Nashville.

That matters because commercial paving gives ROAD more exposure to private development work, including warehouses and data centers, while public road projects provide a steadier base of recurring infrastructure demand.

See analysts’ growth forecasts and price targets for Construction Partners (It’s free) >>>

Margin performance is another key lever. Construction Partners sources more than 50% of its liquid asphalt needs internally, and management said liquid asphalt index protection covers more than 80% of total revenue. That gives the company more protection when energy and material costs move around, helping ROAD protect profitability better than less vertically integrated contractors.

The acquisition strategy also supports the long-term case. ROAD operates in a fragmented road construction market, and its deal strategy gives it a way to expand share without relying only on organic growth. The company has completed 17 acquisitions since the beginning of fiscal 2024, and management said it still has a robust pipeline of opportunities.

Based on these inputs, the model estimates a target price of around $215, implying about 70% total upside over the next 4 years. That suggests the stock appears undervalued if ROAD keeps converting backlog into revenue, integrates acquisitions well, and continues improving margins as it scales.

At current levels, Construction Partners appears undervalued, with future performance driven by backlog conversion, disciplined acquisitions, margin improvement, and steady road infrastructure demand across high-growth Sunbelt markets.

How Much Upside Does ROAD Stock Have From Here?

Investors can estimate Construction Partners’ potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Construction Partners in under 60 seconds with TIKR (It’s free) >>>