Key Stats for SMCI Stock

- Past-Week Performance: -12%

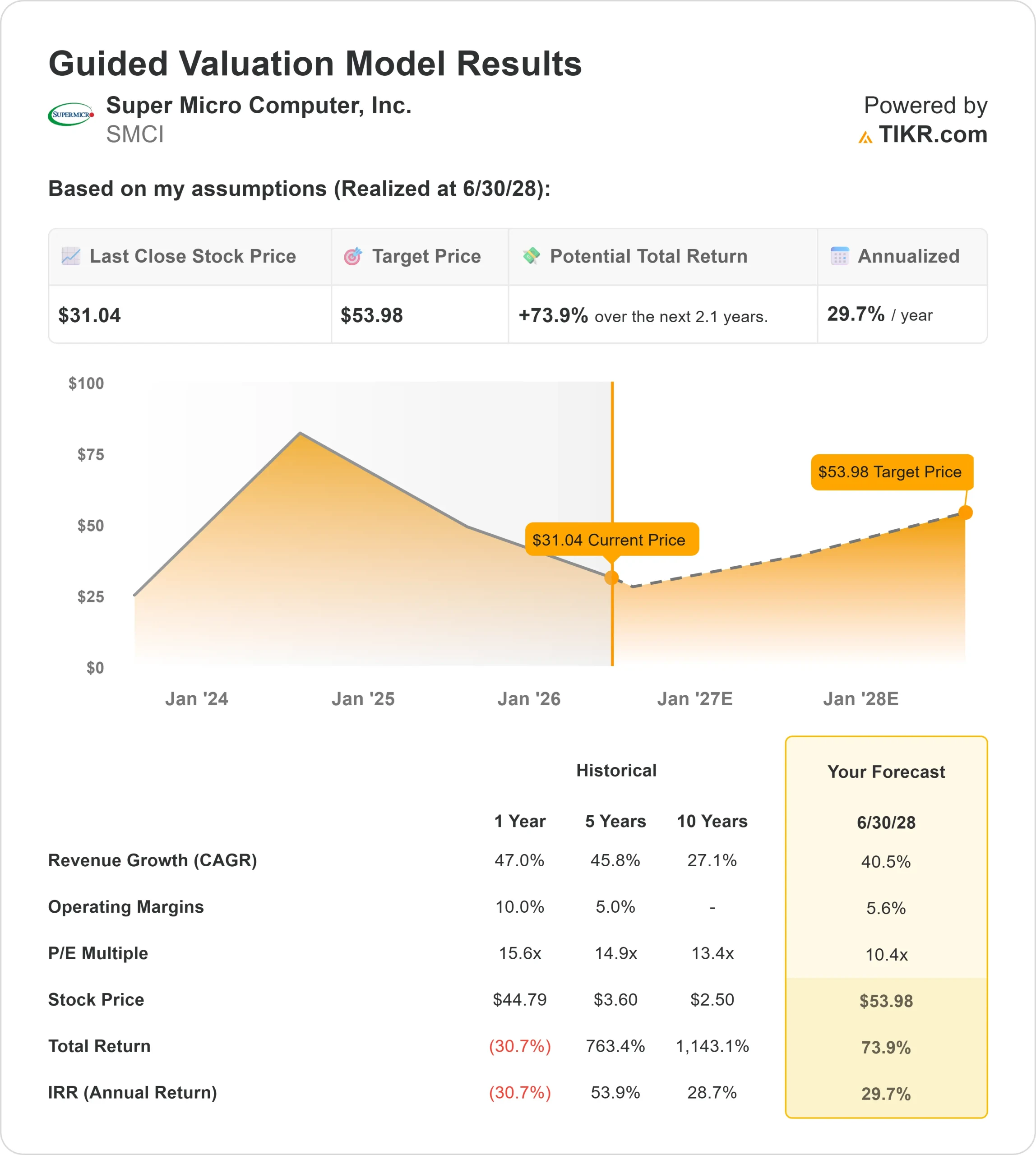

- 52-Week Range: $19 to $62

- Valuation Model Target Price: around $54

- Implied Upside: about 74%

Analyze your favorite stocks like Super Micro Computer with TIKR (It’s free) >>>

What Happened?

Super Micro Computer, Inc. stock fell about 12% this week, finishing near $31 per share as investors looked past strong AI server demand and focused on mixed analyst updates, customer delivery delays, rising competition, and margin durability. SMCI remains one of the clearest hardware plays tied to AI data center spending, but the market is no longer rewarding revenue growth by itself.

The stock moved lower because Wall Street stayed cautious after Super Micro’s Q3 update, even as some firms raised their price targets. Goldman Sachs raised its target to $30 from $27 but kept a Sell rating, Barclays cut its target to $34 from $38 and kept an Equal Weight rating, while Rosenblatt lifted its target to $40 from $32 and kept a Buy rating.

The mixed reaction captured the main debate around SMCI: AI demand remains strong, but margins, customer concentration, execution, and competition from Dell Technologies, Hewlett Packard Enterprise, and Lenovo remain key concerns.

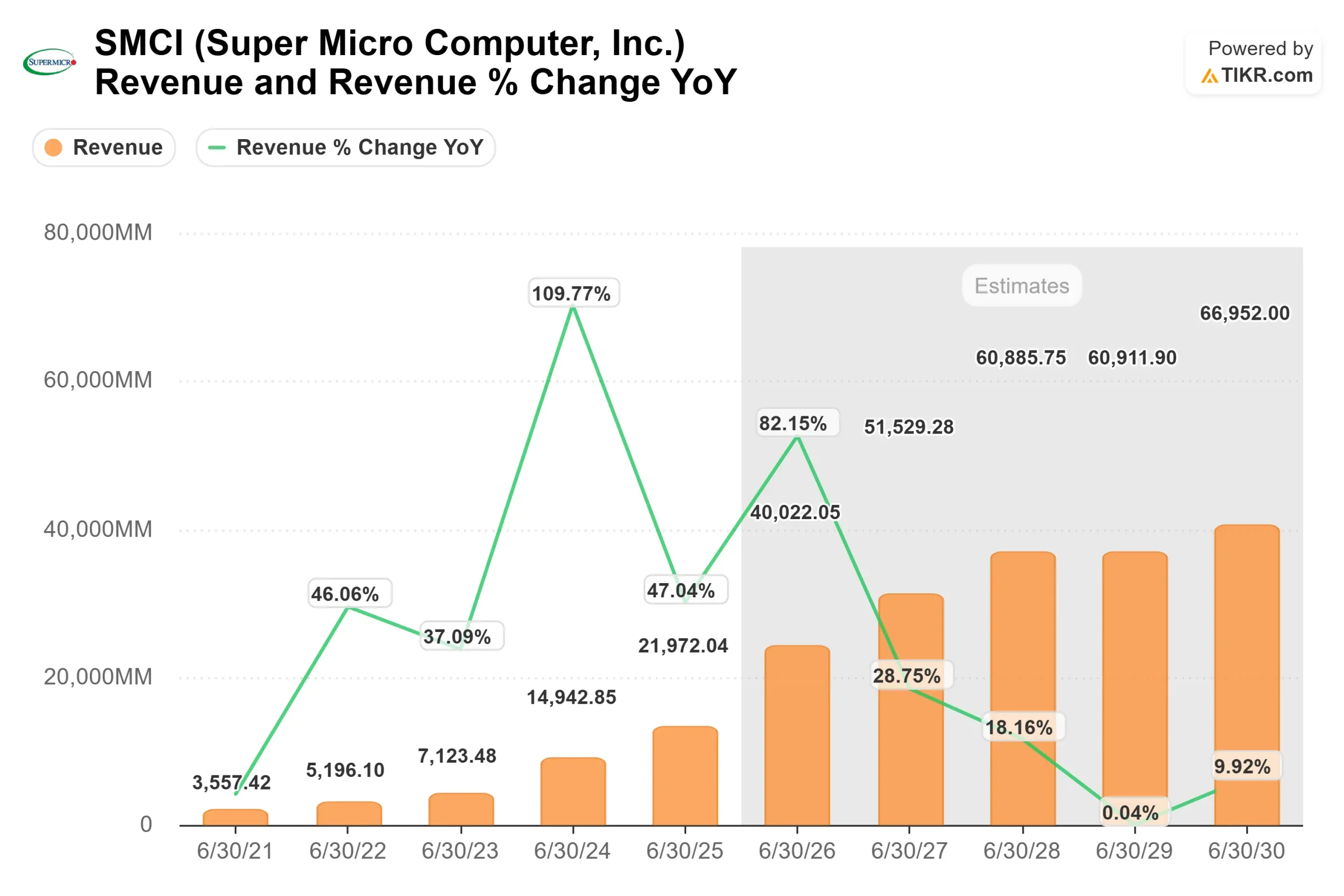

The Q3 update reinforced both sides of that debate. Fiscal Q3 revenue reached $10.2 billion, up 123% year over year, with AI GPU-related platforms contributing more than 80% of revenue, while non-GAAP gross margin improved to 10.1% from 6.4% in Q2.

CEO Charles Liang said “our business fundamentals are stronger than ever,” and management guided for Q4 net sales of $11 billion to $12.5 billion, with full-year fiscal 2026 revenue expected between $38.9 billion and $40.4 billion.

Recent institutional filings also pointed to mixed positioning rather than a clear vote of confidence. Some large holders trimmed exposure while others added to or opened positions, suggesting institutions remain involved but selective.

This week’s decline showed investors want better proof that Super Micro can convert AI server growth into durable profits, steadier cash flow, and more consistent execution.

Value Super Micro Computer instantly (Free with TIKR) >>>

Is SMCI Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): around 41%

- Operating Margins: around 6%

- Exit P/E Multiple: about 10x

Revenue growth is the main driver of the SMCI setup. The model shows revenue rising from about $15 billion in fiscal 2024 to about $67 billion by fiscal 2030, supported by AI server demand, rack-scale deployments, and growing interest in liquid-cooled data center infrastructure.

Liquid cooling matters because AI servers generate far more heat than traditional data center equipment. Super Micro’s liquid-cooled rack systems can help customers run higher-density AI workloads more efficiently, which becomes more important as data centers add larger clusters of power-hungry GPUs.

The harder question is profitability. The model assumes operating margins of around 6%, reflecting the thin-margin reality of AI server hardware, where component costs, competitive pricing, and large customer deals can pressure profits even when revenue is growing quickly.

That makes the next year more about execution than demand. Stronger results could come from faster conversion of delayed customer deployments into shipments, better supply availability for CPUs, GPUs, and memory, and stronger pricing discipline on large AI infrastructure orders.

See analysts’ growth forecasts and price targets for Super Micro Computer (It’s free) >>>

Competition also matters. Dell Technologies, Hewlett Packard Enterprise, and Lenovo are all competing for the same AI server budgets. Super Micro’s edge is speed, customization, and liquid-cooling leadership, but the company needs to prove those advantages can support margins as competition rises.

DCBBS, or Data Center Building Block Solutions, is another key driver. Instead of only selling servers, Super Micro is trying to sell more complete data center infrastructure, including cooling, networking, power systems, software, and services. That could deepen customer relationships and create better profit streams over time.

Based on these inputs, the model estimates a target price of around $54, implying about 74% total upside. That suggests SMCI appears undervalued at current prices, but the 10x exit P/E multiple shows the market is still discounting the stock for execution risk, thin hardware margins, customer concentration, and governance-related concerns.

At current levels, SMCI appears undervalued under the model, with future performance driven by AI server demand, liquid cooling adoption, DCBBS growth, and the company’s ability to turn fast revenue growth into steadier profits.

How Much Upside Does SMCI Stock Have From Here?

Investors can estimate Super Micro Computer’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Super Micro Computer in under 60 seconds with TIKR (It’s free) >>>