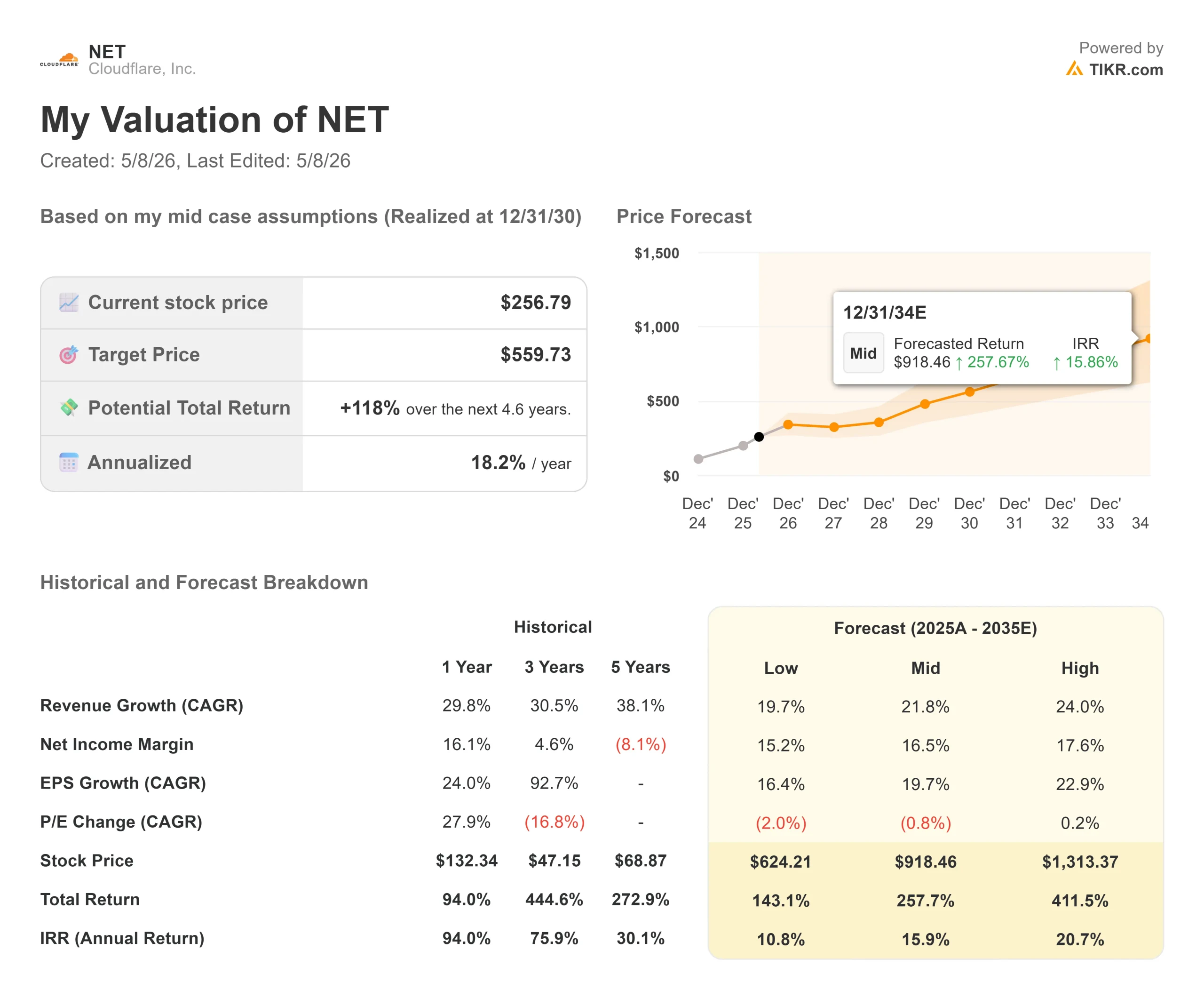

Key Stats for Cloudflare Stock

- Current Price: $256.79

- Target Price (Mid): ~$560

- Street Target: ~$232

- Potential Total Return: ~118%

- Annualized IRR: ~18% / year

- Earnings Reaction (Q1 2026, reported 5/7/26): +3.30%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

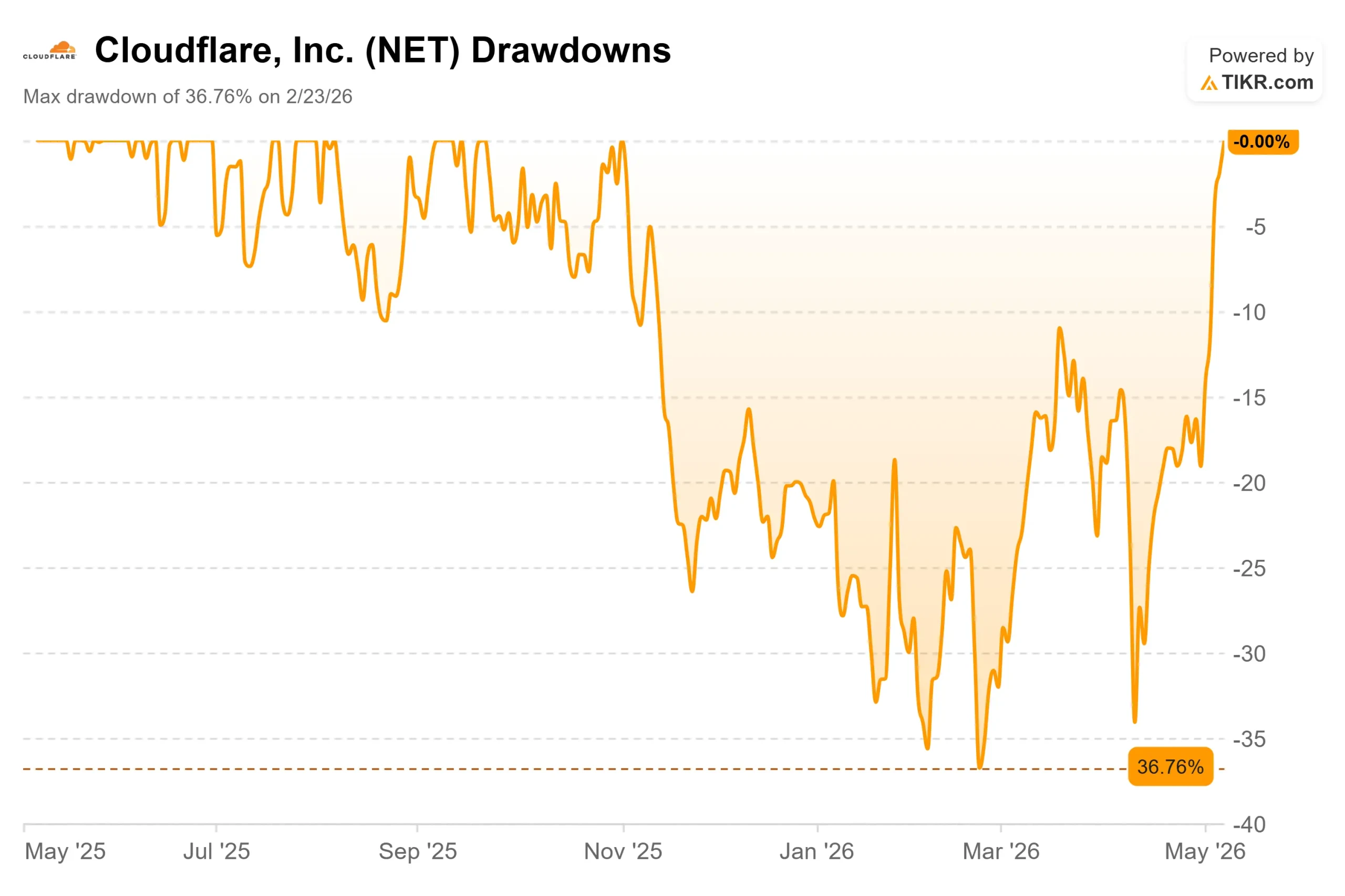

High-multiple software stocks rarely survive a 20% workforce cut without a brutal after-hours session, and Cloudflare (NET) was no exception on May 7. The stock fell as much as 18% in extended trading after the company announced it was eliminating over 1,100 positions, roughly 20% of its global headcount, alongside Q1 2026 results that beat Wall Street on every metric that matters. By the close of the May 7 session, NET was back at $256.79, up 3.30% on the day. Bulls read that recovery as confirmation that the AI-first restructuring narrative holds. Bears pointed to gross margin compression and a Q2 revenue guide that came in just below some estimates. The key question for the rest of 2026 is whether Cloudflare is genuinely ahead of the industry on agentic AI adoption, or whether execution risk will resurface every time the stock gets tested.

See historical and forward estimates for Cloudflare stock (It’s free!) >>>

What Cloudflare Actually Reported

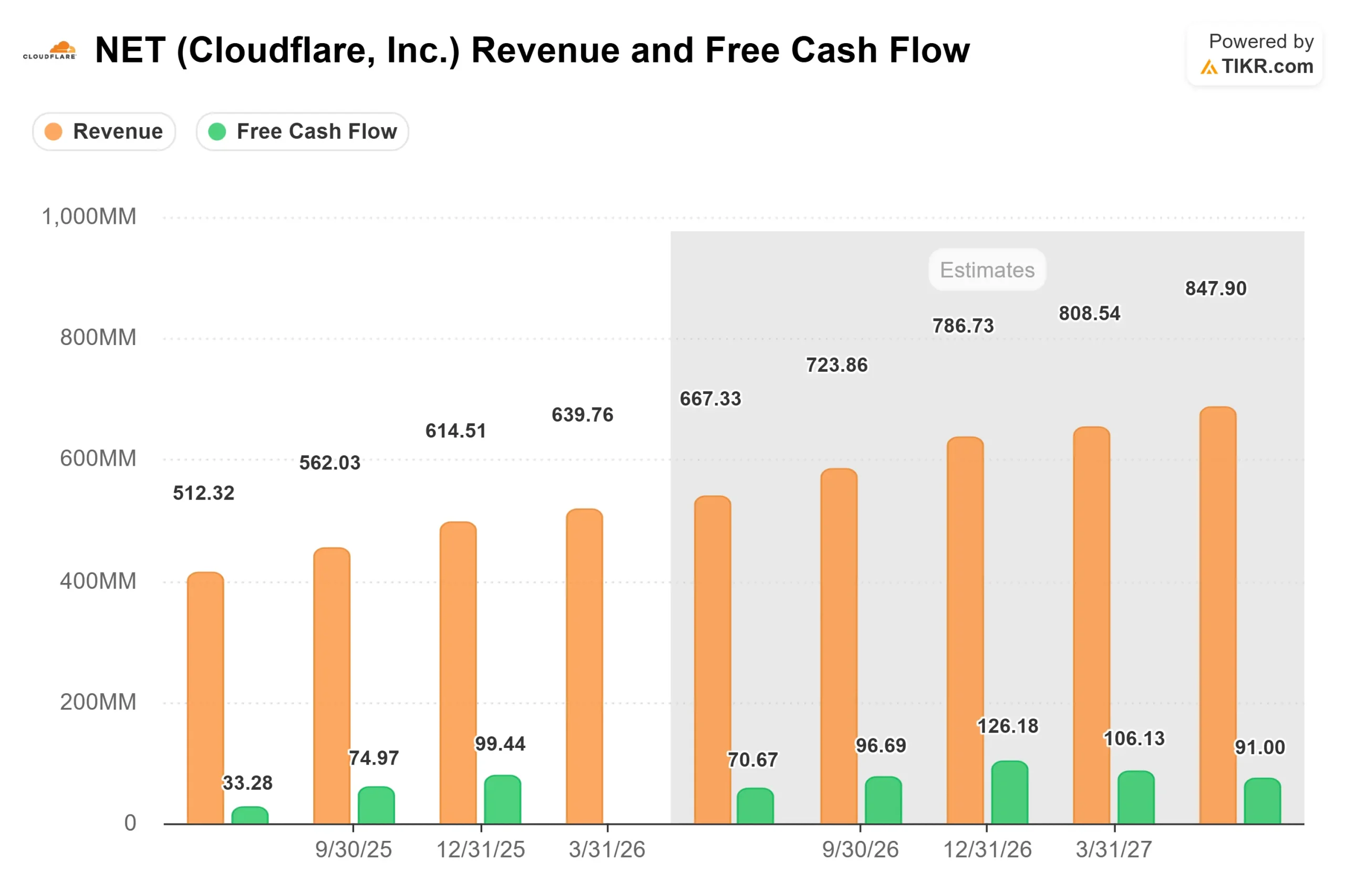

The Q1 numbers are straightforward. Revenue came in at $639.8 million, up 34% year-over-year and ahead of the Wall Street consensus of $622.8 million by 2.72%, per TIKR’s Beats and Misses data. Non-GAAP operating income was $73.1 million, an operating margin of 11.4%, and a 31% increase year-over-year from $56 million in the same period last year. Free cash flow reached $84.1 million, or 13% of revenue, up from 11% a year ago. EBITDA of $130.91 million beat the $124.39 million consensus by 5.24%, per TIKR.

The large customer numbers were even stronger. The company ended Q1 with 4,416 customers paying more than $100,000 annually, up 25% year-over-year, and that group now accounts for 72% of total revenue, up from 69% a year ago. Deals over $1 million grew 73% year-over-year. Customers spending more than $5 million annually grew 50% year-over-year, and Cloudflare added as many of those accounts in Q1 alone as it did in all of 2025.

Dollar-based net retention, which measures how much existing customers expand their spending over time, came in at 118%. That is down 2 percentage points sequentially from Q4 2025 but up 7 points year-over-year. CFO Thomas Seifert explained the sequential dip on the call: new customer additions accelerated at the highest rate since 2023, which temporarily dilutes the retention metric. Remaining performance obligations, or RPO (the total value of contracted revenue not yet recognized), reached $2.543 billion, up 36% year-over-year.

What the Layoffs Are Actually About

The restructuring overshadowed the earnings beat in after-hours trading, but context matters. Revenue grew 34%, and the company simultaneously raised full-year guidance on both revenue and earnings per share. This was not a cost-cutting response to a deteriorating business.

CEO and Co-Founder Matthew Prince was direct on the May 7, 2026 earnings call: “We are reimagining every internal process from engineering to finance to sales to run on an agentic AI backbone on our Workers platform. This isn’t a cost-cutting exercise or an assessment of the individual’s performance. It’s about defining how a world-class, high-growth company operates and creates value in the agentic era.”

The specifics are concrete. Cloudflare has built what it calls Cloudflare OS, an internal agentic workflow system running on its own Workers developer platform, that allows teams across the company to deploy AI-driven processes against shared data systems. Prince disclosed that 97% of the R&D team now uses AI coding tools, that 100% of contributions to production codebases are reviewed by autonomous AI agents, and that internal AI usage increased by more than 600% in the three months before the announcement.

The restructuring charges total $140 million to $150 million for full-year 2026, with approximately $40 million non-cash and the majority hitting in Q2. Cloudflare left its full-year free cash flow outlook unchanged. Seifert confirmed on the call that quota-carrying sales headcount, the team directly responsible for generating revenue, was the one area the cuts did not meaningfully touch.

See how Cloudflare performs against its peers in TIKR (It’s free!) >>>

Cloudflare’s Position in the Agentic Traffic Wave

The earnings call offered the clearest picture yet of how Cloudflare is benefiting from AI-driven internet traffic growth. Prince described processing hundreds of billions of agentic requests per month, a number he said is growing exponentially. The dynamic is simple: a human browsing for a product might visit five websites; an AI agent completing the same task might interact with thousands. Each of those interactions passes through networks and security layers that Cloudflare already sits in front of.

“Not all traffic is created equal,” Prince said on the call. Cloudflare deliberately built its Act 1 business, which covers application services and security, including its content delivery network (CDN) and API protection products, around high-value API and application traffic rather than commodity video streaming. As agentic traffic scales, that positioning is showing its value.

The Workers developer platform, where developers run code directly on Cloudflare’s global network edge, is where the growth inflection is clearest. The platform added one million new developers in Q1 alone, nearly matching the 1.5 million added in all of 2025. Prince noted on the call that one large AI studio went from essentially zero to over one million dynamic Workers on the platform within a fifteen-day window. More than three-quarters of the Workers platform’s growth is coming from new customers.

The gross margin compression that spooked investors is a direct result of this growth. Workers’ products carry a lower profit margin than Cloudflare’s corporate average, and the conversion of previously free traffic to paid products moves costs from sales and marketing into cost of revenue. Seifert addressed the optics directly on the call: “Our operating margin becomes a better measure for the competitiveness of products than gross margin.” He added that Cloudflare is already tracking above 46% on a Rule of 40 basis (revenue growth rate plus free cash flow margin, a standard software health benchmark) and sees a path above 50% in 2027.

Prince also described a potential fourth business line: helping content owners control and charge AI companies for bot access to content on Cloudflare-protected websites. It is not yet a revenue line, but Prince named it as one of Cloudflare’s six stated priorities for 2026, noting the company has moved from low penetration in media to a dominant position. Cloudflare operates across more than 350 cities in more than 120 countries, per Prince’s comments on the call, giving it the infrastructure scale to serve both sides of that market.

From a valuation standpoint, Cloudflare trades at roughly 30x NTM EV/Revenue and around 135x NTM EV/EBITDA, per TIKR Multiples data as of May 7, 2026. Peers Akamai Technologies and Fastly trade at 4.59x and 4.24x NTM EV/Revenue, respectively, per TIKR Competitors data. The gap reflects a different business model: Akamai and Fastly are primarily bandwidth businesses, while Cloudflare’s network functions as programmable infrastructure for AI workloads, Zero Trust security, and developer compute. Whether that distinction justifies roughly 7x the peer multiple is the valuation question every NET investor has to answer for themselves.

TIKR Advanced Model Analysis

- Current Price: $256.79

- Target Price (Mid): ~$560

- Potential Total Return: ~118%

- Annualized IRR: ~18% / year

See analysts’ growth forecasts and price targets for Cloudflare stock (It’s free!) >>>

The mid case targets 12/31/30 at an entry price of $256.79. The two primary revenue CAGR drivers are Workers developer platform expansion, where new customer additions are growing at the fastest pace since 2023, and sustained enterprise deal momentum, with $1 million-plus deals growing 73% year-over-year in Q1. The margin driver is operating leverage as headcount costs decline and revenue scales. The mid case assumes a revenue CAGR of around 22% and a net income margin expanding to around 17%, per TIKR model inputs.

The upside is a world where agentic traffic growth accelerates, the content monetization opportunity generates real revenue, and Cloudflare OS delivers structurally higher free cash flow margins ahead of schedule. The downside is gross margin pressure that outpaces operating leverage, restructuring friction at a moment when enterprise customers want stability, and a Q2 guide of $664 million to $665 million that proves to be a ceiling rather than a floor.

The Street mean price target sits at around $232, below the current trading price. 17 analysts rate NET Buy, 7 Outperform, 9 Hold, 1 Underperform, and 1 Sell, per TIKR Street Targets data as of May 7, 2026. These ratings were set before the Q1 print and may not yet reflect post-earnings revisions.

Conclusion

The metric to watch at Cloudflare’s Q2 2026 earnings (expected late July 2026) is dollar-based net retention. A reading at or above 118% confirms the expansion flywheel is intact despite the restructuring. A slip below 116% would indicate the workforce disruption is creating friction with existing customers, making the current premium harder to justify. Q1 showed the business is executing. The restructuring is the best that the next chapter is stronger still.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Cloudflare?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Cloudflare, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cloudflare alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Cloudflare on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!