Key Takeaways:

- Axon Enterprise (AXON) delivered Q1 2026 revenue of $807 million, up 34% year-over-year, beating analyst estimates while raising its full-year revenue growth forecast.

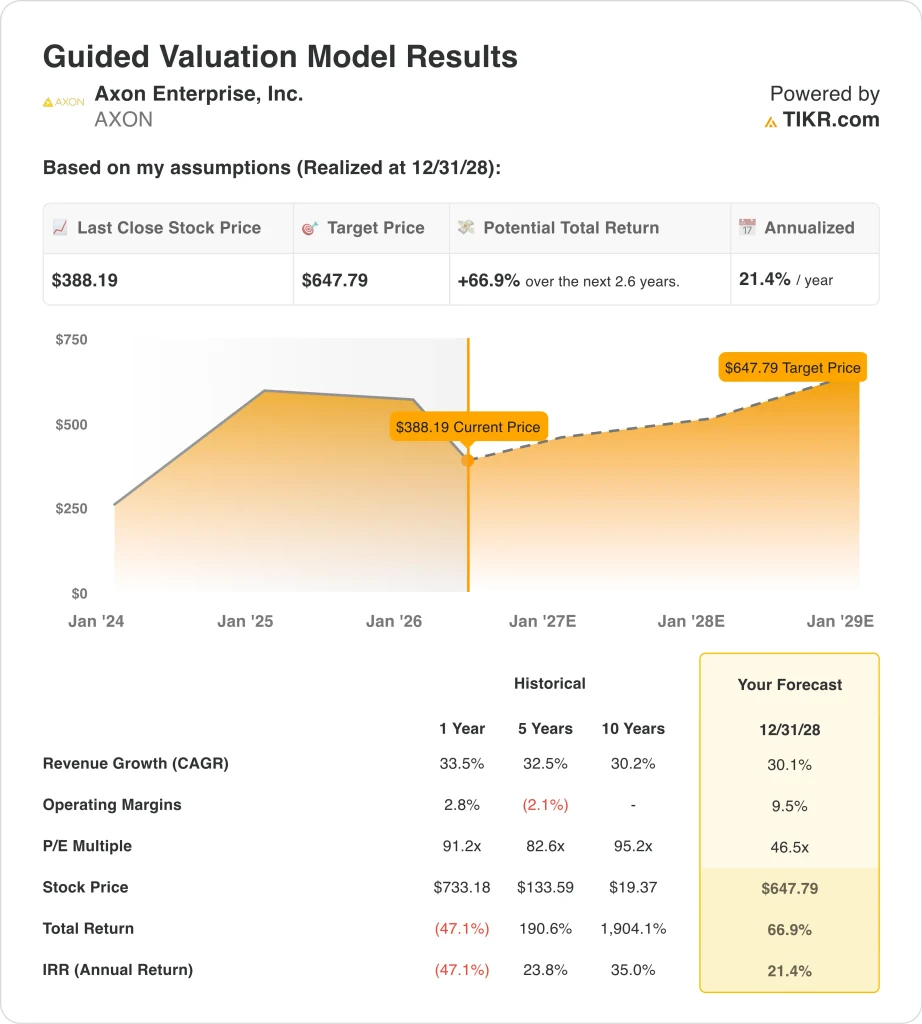

- AXON stock trades at around $388, down roughly 46% from its 52-week high of $886. Analysts maintain a consensus target price of around $662.

- AXON stock could rise from $388 to around $648 per share by December 2028.

- That implies a total return of around 67% and an annualized return of around 21%.

What Happened?

Axon Enterprise (AXON) delivered a strong Q1 2026 earnings report on May 7, 2026. Revenue climbed 34% year-over-year to $807 million, beating analyst estimates. Net income rose to $169 million. Management then raised its full-year revenue growth forecast on stronger-than-expected software and security device demand.

The company makes TASER devices, body cameras, and cloud-based software for law enforcement and enterprise customers. Evidence.com is Axon’s digital evidence management platform used by police agencies across the country.

Software subscriptions generate recurring revenue with high switching costs. And strong Q4 2025 results of $797 million in revenue, up 39% year-over-year, showed consistent momentum heading into 2026.

Axon debuted real-time AI tools at its Axon Week 2026 user conference in April. These tools connect body cameras to cloud workflows and evidence management systems. But TD Cowen trimmed its price target in early April, citing near-term stock weakness before earnings. Investor tone shifted quickly after the Q1 beat and guidance raise, sending shares sharply higher.

AXON stock still sits roughly 46% below its 52-week high of $886. So a wide gap exists between where shares trade today and where analysts see fair value at around $662. Investors are refocusing on whether AI tools can drive faster software adoption and margin improvement.

Here’s why Axon Enterprise stock could deliver strong compounding returns through 2028 as its AI platform and cloud ecosystem continue to scale.

What the Model Says for AXON Stock

We analyzed the upside potential for Axon Enterprise stock based on its expanding AI tools, deepening law enforcement contracts, and growing cloud-based evidence management platform.

Based on estimates of around 30% annual revenue growth, around 10% operating margins, and a normalized P/E multiple of around 47x, the model projects Axon Enterprise stock could rise from $388 to around $648 per share.

That would be a total return of around 67%, or around 21% annualized over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for AXON stock:

1. Revenue Growth: 30.1%

Axon delivered Q1 2026 revenue of $807 million, up 34% year-over-year. This beat analyst estimates and shows continued demand for both hardware and software products. Management raised its FY 2026 guidance on strong software and security device momentum.

Based on analysts’ consensus estimates, we used around 30% annual revenue growth. This reflects Axon’s sustained momentum in cloud software subscriptions, expanding TASER and camera placements, and new AI product launches across law enforcement and enterprise customers. And the company’s forward two-year revenue CAGR of around 30% aligns closely with this figure.

So this growth rate reflects realistic near-term execution. And Axon’s backlog of government contracts provides meaningful visibility into future revenue streams. The 30% assumption is well-grounded in current analyst consensus and observable business trends.

2. Operating Margins: 9.5%

Axon’s last-twelve-month EBIT margin is currently around 0.3%, but gross margins are strong at around 60%. The low EBIT margin reflects heavy R&D spending, AI development investment, and international expansion costs. But software and cloud revenue carry structurally higher margins than hardware.

Based on analysts’ consensus estimates, we used around 10% operating margins. This assumes Axon successfully grows its software mix as a share of total revenue. And it assumes management maintains investment discipline while scaling its AI tools and enterprise security business.

The 60% gross margin base gives Axon strong underlying economics to build from. So as high-margin cloud software becomes a larger percentage of revenue, operating margin improvement should materialize. An AI tool launched in 2026 could accelerate this shift earlier than the market expects.

3. Exit P/E Multiple: 46.5x

Axon currently trades at a next-twelve-months P/E of around 46x. This reflects investor expectations of high revenue growth and long-term margin expansion. High-growth public safety technology companies with recurring software revenue typically command premium multiples. Axon’s dominance in law enforcement hardware and software supports this premium.

Based on analysts’ consensus estimates, we maintained a normalized P/E multiple of around 47x. This reflects Axon’s unique competitive positioning and the high barriers to entry in its core market. Law enforcement agencies rarely switch technology providers after full deployment, and so this creates strong revenue durability.

The multiple does incorporate some compression over time as growth rates moderate. But Axon’s expanding AI suite and growing enterprise segment provide continued support for a premium valuation. And ongoing contract wins demonstrate the long-term durability of its revenue base.

Build your own Valuation Model to value any stock (It’s free!) >>>

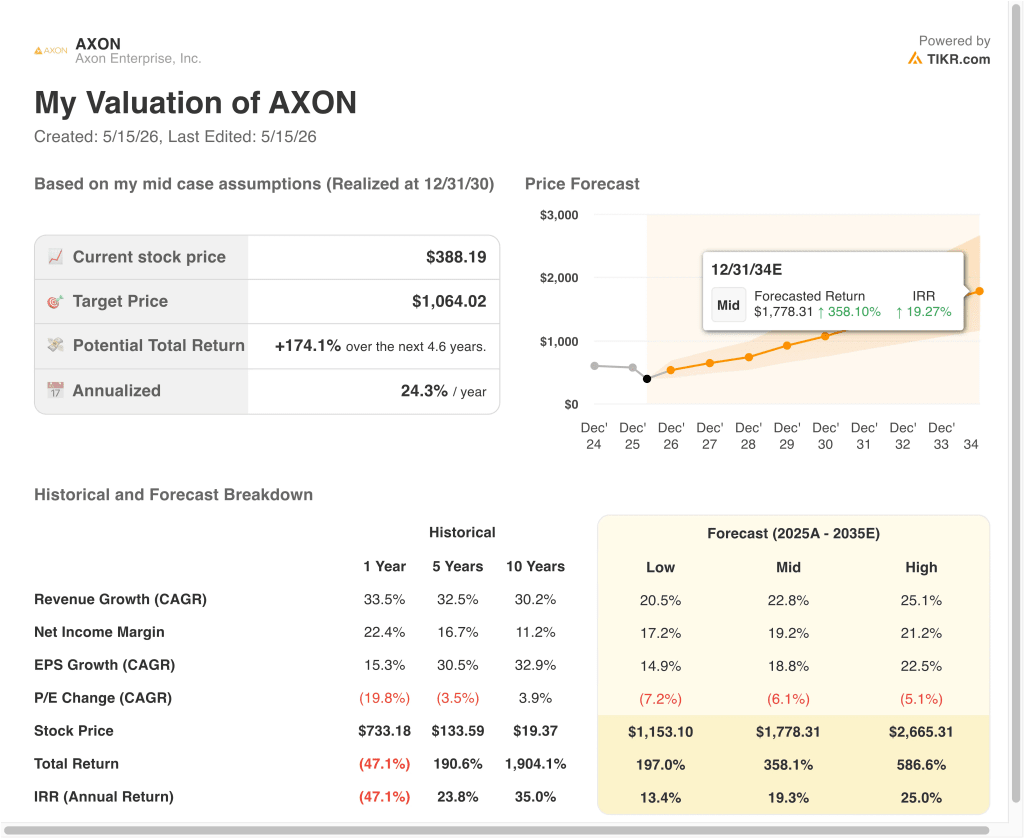

What Happens If Things Go Better or Worse?

Different scenarios for AXON stock through 2034 show varied outcomes based on software monetization, AI adoption rates, and margin expansion (these are estimates, not guaranteed returns):

- Low Case: Software growth underperforms and margin expansion stalls, with slower AI and enterprise adoption → around 13% annual returns

- Mid Case: AI tools drive sustained strong revenue growth and consistent margin improvement across the platform → around 19% annual returns

- High Case: Rapid AI monetization, accelerating enterprise contract wins, and international expansion deliver stronger-than-expected results → around 25% annual returns

Going forward, Axon’s stock path depends on executing its AI and software strategy while delivering consistent margin progress alongside revenue growth. The Q1 2026 earnings beat and raised guidance confirm real operational momentum.

But investors will need to see sustained margin improvement alongside high revenue growth for AXON shares to recover and justify a premium multiple on a long-term basis.

See what analysts think about AXON stock right now (Free with TIKR) >>>

Should You Invest in Axon?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AXON, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AXON alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!