Key Stats for CrowdStrike Stock

- Friday’s Performance: -6%

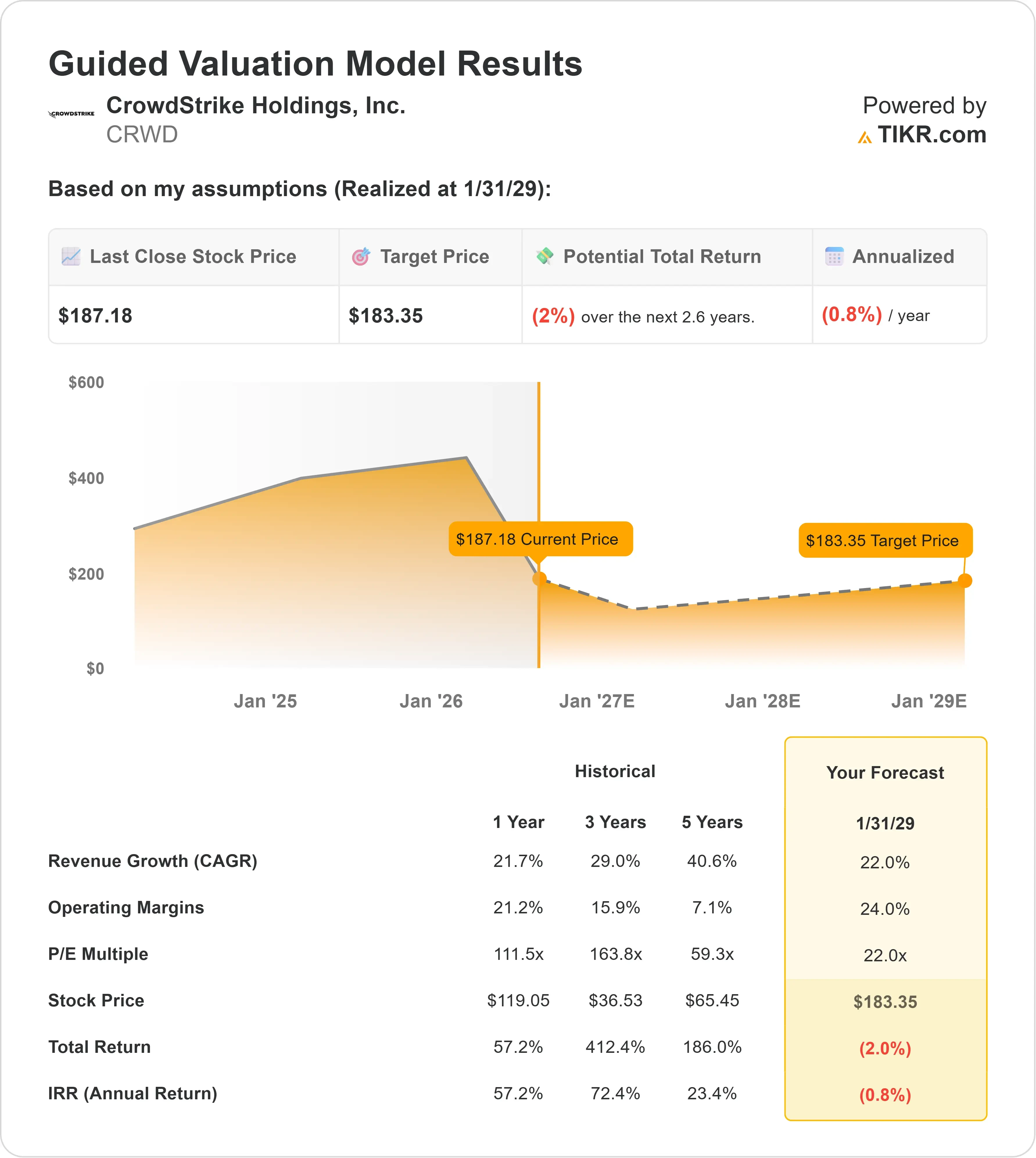

- 52-Week Range: $86 to $210

- Valuation Model Target Price: Around $183

- Implied Downside: About 2%

Analyze your favorite stocks like CrowdStrike with TIKR (It’s free) >>>

What Happened?

CrowdStrike has become one of Wall Street’s most prominent bets on the idea that rapid AI adoption will create an equally large need for cybersecurity. That enthusiasm helped lift CRWD to a split-adjusted 52-week high near $210 on July 6, but the stock fell nearly 6% Friday to around $187. The decline stood out as the Nasdaq gained about 0.3% and the S&P 500 rose about 0.4%, indicating that the selling was concentrated in CrowdStrike rather than driven by a broader market downturn.

The stock appears to have fallen mainly because investors locked in gains after its sharp rally and reconsidered how much future growth was already reflected in its premium valuation. CRWD had ended a two-day losing streak with a 4% rebound Thursday, but Friday’s decline more than erased that recovery and left the stock about 11% below its recent high. CrowdStrike’s 4-for-1 stock split began trading on a split-adjusted basis on July 2, reducing the quoted share price without changing the company’s market value, earnings power, or underlying valuation.

Recent analyst updates remained constructive but showed disagreement over how much upside remains. UBS maintained a Buy rating and raised its split-adjusted price target from $198 to $235, citing the potential for AI security demand to support another growth cycle. Morgan Stanley maintained an Overweight rating but trimmed its target from around $173 to $172, below Friday’s closing price, highlighting the divide between confidence in CrowdStrike’s business and concern that much of its expected growth may already be priced into the shares.

CrowdStrike’s latest results did not point to weakening demand. Fiscal first-quarter revenue rose 26% to $1.39 billion, annual recurring revenue, which measures the size of its subscription base, increased 24% to $5.51 billion, and net new ARR reached $255.8 million, up 32%. CEO George Kurtz said, “The more AI an organization adopts, the more cybersecurity it requires,” as customers expanded spending across endpoint protection, cloud security, identity tools, and next-generation SIEM, which gathers security data across an organization.

CrowdStrike’s 26% revenue growth also exceeded SentinelOne’s 21% growth in the comparable quarter, while ARR increased 24% at CrowdStrike and 23% at SentinelOne, showing that CrowdStrike continues to grow slightly faster than one of its closest endpoint-security competitors.

Value CrowdStrike instantly (Free with TIKR) >>>

Is CrowdStrike Slightly Overvalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 22%

- Operating Margins: 24%

- Exit P/E Multiple: 22x

CrowdStrike’s 22% revenue-growth assumption depends on selling existing Falcon customers more cloud security, identity protection, next-generation SIEM, and AI detection and response products rather than relying only on new endpoint-security customers.

Falcon Flex, which allows customers to commit spending upfront and add products as their needs change, represented more than $1.9 billion in ending ARR, while customers expanding through re-Flex increased their commitments by an average of 26%, showing how platform consolidation can raise contract values without relying entirely on new customer wins.

See analysts’ growth forecasts and price targets for CrowdStrike (It’s free) >>>

Cash generation provides important support for the valuation, with CrowdStrike producing $468.5 million in first-quarter free cash flow, equal to 34% of revenue, while management expects a free cash flow margin of at least 30% for fiscal 2027.

The 24% operating-margin assumption reflects the potential for recurring revenue to grow faster than operating expenses, while the 22x exit P/E assumes significant valuation compression as CrowdStrike matures and earnings catch up with its premium share price.

Based on these inputs, TIKR’s model estimates a target price of around $183, implying about 2% downside over roughly 2.6 years and suggesting that CrowdStrike is fairly valued to slightly overvalued near $187, with stronger returns requiring sustained AI-security demand, larger Falcon Flex commitments, and profit growth above the model’s assumptions.

How Much Upside Does CrowdStrike Stock Have From Here?

Investors can estimate CrowdStrike’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value CrowdStrike in under 60 seconds with TIKR (It’s free) >>>