Key Stats for Sysco Stock

- 52-Week Range: $64 to $85

- Current Price: $73.05

- Street Mean Target: ~$83

- TIKR Target Price (Mid): ~$107

- TIKR Annualized IRR (Mid): ~10% per year

- FY2025 Revenue: $81.4B

- FY2026 Full-Year Adjusted EPS Guidance: $4.50 to $4.60

- US Local Case Volume Growth (Q3 FY2026): 3.3% YoY

- Dividend Yield: ~3%

Value your favorite stocks like SYY with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

How Sysco Makes Money and Why Scale Is the Entire Story

Sysco (SYY) is the largest foodservice distributor in the United States, delivering food, kitchen supplies, and related products to roughly 700,000 customer locations: restaurants, hotels, hospitals, schools, and caterers. The company operates more than 340 distribution facilities and runs one of the largest private trucking fleets in the country.

The business model is simple in concept and hard to replicate in practice. Sysco buys in bulk from producers, warehouses it, and delivers it on tight schedules. The margin on any individual delivery is thin. The competitive advantage is pure scale: the more volume Sysco moves, the lower the per-unit cost, the better the supplier terms, and the harder it becomes for smaller competitors to match on price or service reliability.

That scale took decades to build. US Foods is the main domestic competitor at roughly half Sysco’s size. Performance Food Group is a distant third. No one is leapfrogging Sysco in US foodservice distribution.

See historical and forward estimates for Sysco stock (It’s free!) >>>

What Four Years of Margin Expansion Actually Look Like

Sysco’s operating margin was 2.86% in fiscal 2021, as it continued to recover from the pandemic. The company then began a deliberate push to improve profitability: better route density, pricing discipline, investment in logistics technology, and a mix shift toward higher-margin specialty products.

The results have been consistent. Margins expanded to 3.45% in fiscal 2022, 3.91% in fiscal 2023, and peaked at 4.35% in fiscal 2024. Revenue grew alongside it, from $51.3 billion to $78.8 billion over the same period. Fiscal 2025 revenue reached $81.4 billion, though the operating margin pulled back slightly from the prior-year peak as cost pressures and acquisition-related expenses weighed on near-term results.

The margin story matters because of the math at this scale. Moving from 2.86% to 4.35% on $78 billion in revenue is roughly $1.2 billion in incremental annual operating income. The long-term ambition is to keep pushing that line higher, and the Restaurant Depot combination is central to that plan. Management has outlined a pro forma EBITDA margin of around 6.7% for the combined business, roughly 150 basis points above Sysco’s current margin.

See what analysts think about SYY stock right now (Free with TIKR) >>>

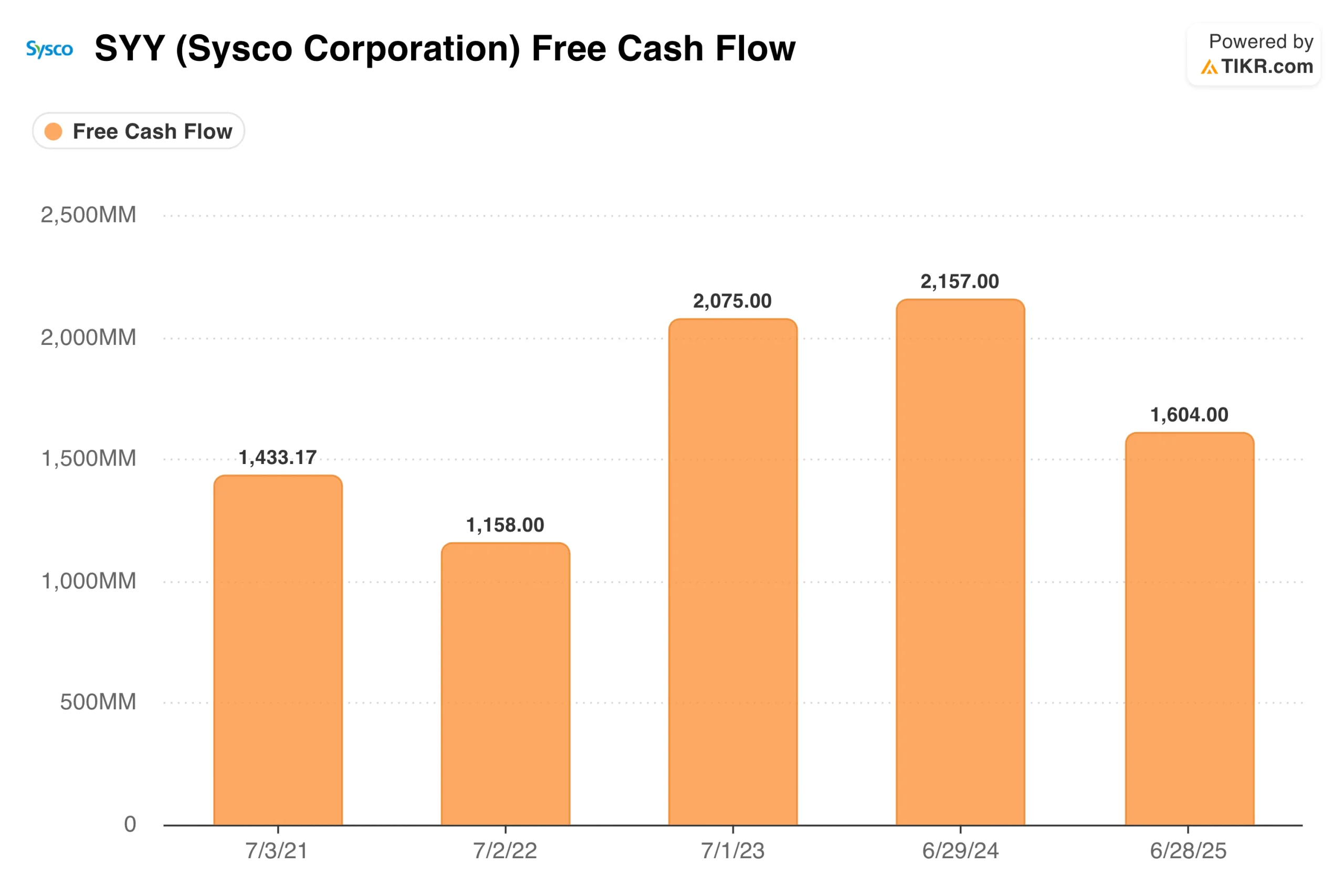

Why the Free Cash Flow Picture Needs Context

Free cash flow grew from $1.4 billion in fiscal 2021 to $2.1 billion in fiscal 2023 and $2.2 billion in fiscal 2024, a strong trajectory for a low-margin distribution business. Fiscal 2025 FCF fell to $1.6 billion, which at first glance appears to be a deterioration.

It is not. The decline reflects elevated transaction costs, integration planning expenses, and incremental capital expenditures tied to the Restaurant Depot acquisition, which was announced in March 2026 and is expected to close by Sysco’s third quarter of fiscal 2027. The underlying business did not change.

Management has stated that the combined entity is expected to increase free cash flow by roughly 55% on a pro forma basis once the deal closes, driven by Restaurant Depot’s minimal capex requirements and strong cash conversion characteristics. A business that generated $16 billion in revenue with only $136 million in annual capex is a meaningful addition to Sysco’s cash flow profile.

What the TIKR Model Implies at $73

The TIKR model targets around $107 per share in the mid case, implying a total return of roughly 47% over about 4.1 years, or about 10% annually. The model uses revenue growth of around 3% per year, a net income margin of around 3%, and EPS growth of around 5% per year.

These assumptions do not require Restaurant Depot synergies to materialize early or margins to expand dramatically above current levels. They reflect a business continuing to do roughly the same as it has been doing. The low case targets around $112 at roughly 5% per year. The high case reaches around $159 at roughly 10% annually. At 10% annualized plus a 3% dividend, the total return profile is competitive for a business with this level of earnings stability.

The Case for SYY: Defensive Revenue, Margin Leverage, and a Transformative Acquisition

Sysco’s revenue base is among the most recession-resistant in the market. Restaurants, hospitals, schools, and hotels do not stop buying food when the economy slows. Volume may soften, but the customer base is structurally sticky and geographically diversified.

The margin expansion thesis has additional runway. Moving from current levels toward the 6.7% pro forma EBITDA target represents hundreds of millions in incremental earnings without requiring revenue acceleration. US local case volume growth accelerated to 3.3% in Q3 fiscal 2026, the strongest quarterly growth rate in over three years, which gives management confidence in reiterating full-year adjusted EPS guidance of $4.50 to $4.60.

The dividend, growing for over 50 consecutive years, provides a 3% yield in addition to the capital appreciation the model identifies.

The Risks: Thin Margins, Acquisition Complexity, and Slow Growth

A net income margin of around 3% means cost increases hit earnings hard. Food inflation, diesel prices, and labor rates all directly affect Sysco’s cost structure, and the thin margin amplifies every move against the company.

The Restaurant Depot acquisition is subject to regulatory approval and is not expected to close until fiscal 2027. Integration of a business serving over 725,000 independent restaurants through 167 warehouse stores is operationally complex, and the $250 million synergy target is a goal, not a guarantee.

Revenue growth of around 3% annually is steady but modest. The investment case here is about margin improvement and EPS compounding, not a revenue inflection.

Is SYY Worth Buying at $73?

Sysco moves food from warehouses to kitchens, earns a thin margin on every delivery, and compounds quietly over time. It does not generate headlines. What it does generate is consistent cash flow, a growing dividend, and a margin structure that has meaningfully improved over four years.

At $73, the stock trades at a roughly 30% discount to the TIKR mid-case target. The 10% annualized return in the mid case, combined with the 3% dividend, is a total return profile that is difficult to find at this level of earnings predictability. The Restaurant Depot deal adds near-term complexity and medium-term upside. The base business keeps executing.

For investors seeking a steady compounder with defensive characteristics and a clear catalyst in the pipeline, the current price appears to be a reasonable entry point.

See analysts’ growth forecasts and price targets for SYY stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!