Key Stats for BBAI Stock

- 52-Week Range: ~$2.41 to ~$5.50

- Current Price: $4.38

- Street Mean Target: ~$6

- TIKR Target Price (Mid): ~$8

- TIKR Annualized IRR (Mid): ~14% per year

- Q1 2026 Revenue: $34.4M (essentially flat YoY)

- Q1 2026 Gross Margin: 34.0% (up from 21.3% a year ago)

- FY2026 Revenue Guidance: $135M to $165M

- Cash and Investments: $431.5M

- Backlog: $281.9M

Value your favorite stocks like BBAI with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What BigBear.ai Actually Does and Why the Defense AI Theme Matters

BigBear.ai (BBAI) provides AI-powered decision intelligence to national security agencies, defense contractors, and government customers in the travel and trade sectors. In practical terms, that means building and deploying AI systems that help intelligence agencies process large volumes of sensor data, help customs authorities identify cargo risk, and help military commanders synthesize information for faster decisions.

The theme is genuinely compelling, as the US Department of Defense has been explicit about accelerating AI adoption across its operations, and allied governments are following. The challenge for BigBear.ai specifically is not whether the market exists. It is whether this particular company can execute consistently enough to capture a meaningful share of it.

That distinction matters because the financials over the last several years have been uneven.

See historical and forward estimates for BBAI stock (It’s free!) >>>

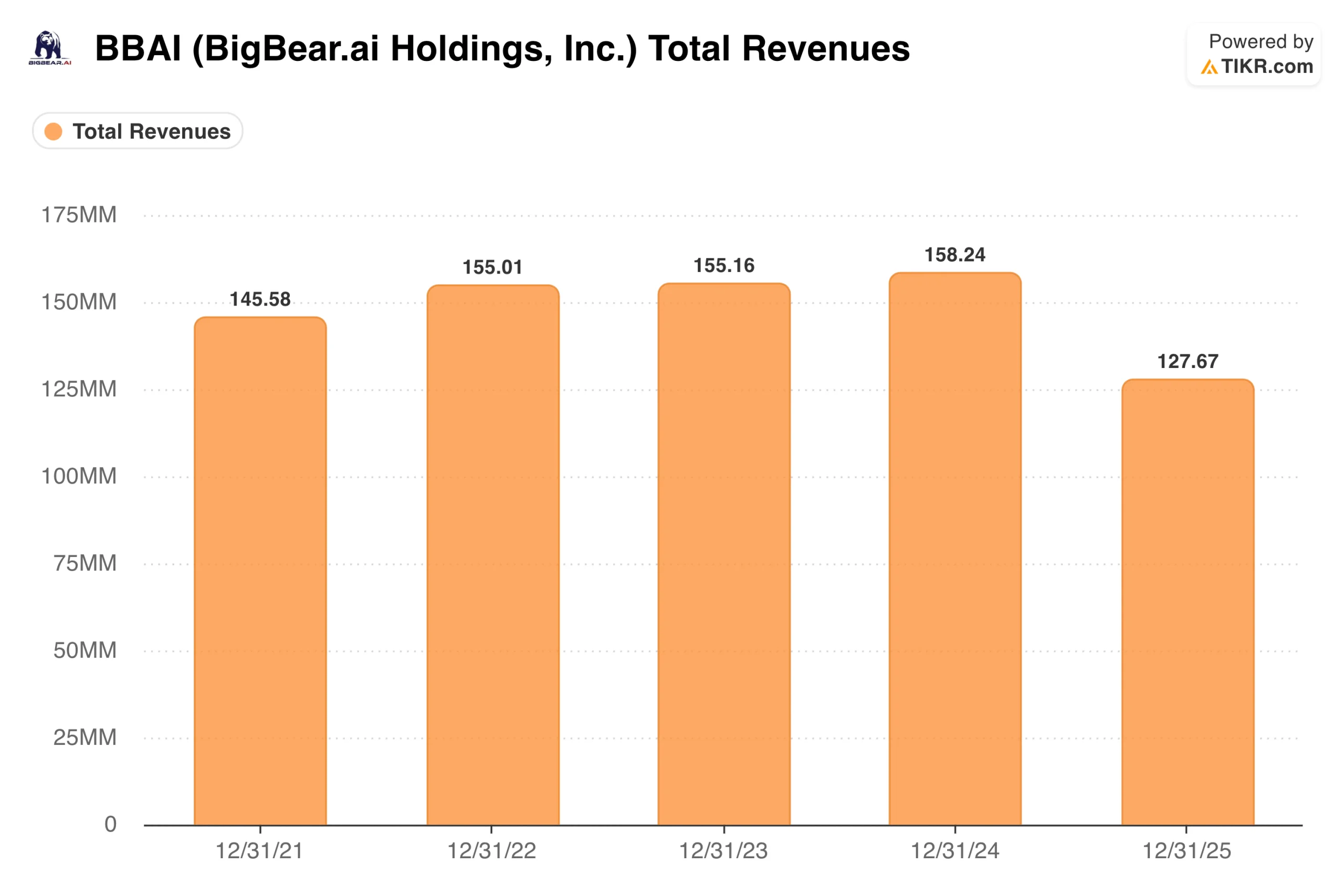

What the Revenue Decline Actually Tells Us

Revenue was essentially flat from 2021 through 2024, moving in a narrow band between $145M and $158M. Then in 2025, it dropped to $127.67M, a 19% decline. That number looks alarming in isolation, and it was the primary reason the stock has been under pressure.

The context is important. Revenue decreased 38% in Q4 2025 compared to Q4 2024, primarily due to lower volume on Army programs. That is a contract timing issue, not a structural loss of competitive position. The Army programs that drove 2024 revenue were completed and were not immediately replaced. Government contracts are inherently lumpy, which is one of the core risks of owning a company this concentrated in federal work.

Management affirmed full-year 2026 revenue guidance of $135M to $165M, which, at the midpoint, implies roughly 17% growth over the 2025 base. Q1 2026 came in at $34.4M, meaning the company needs meaningful acceleration in the back half to hit that range. The backlog grew 14% in Q1 to $281.9M, including a sole-source classified award of $53M, which provides some visibility on where that revenue could come from.

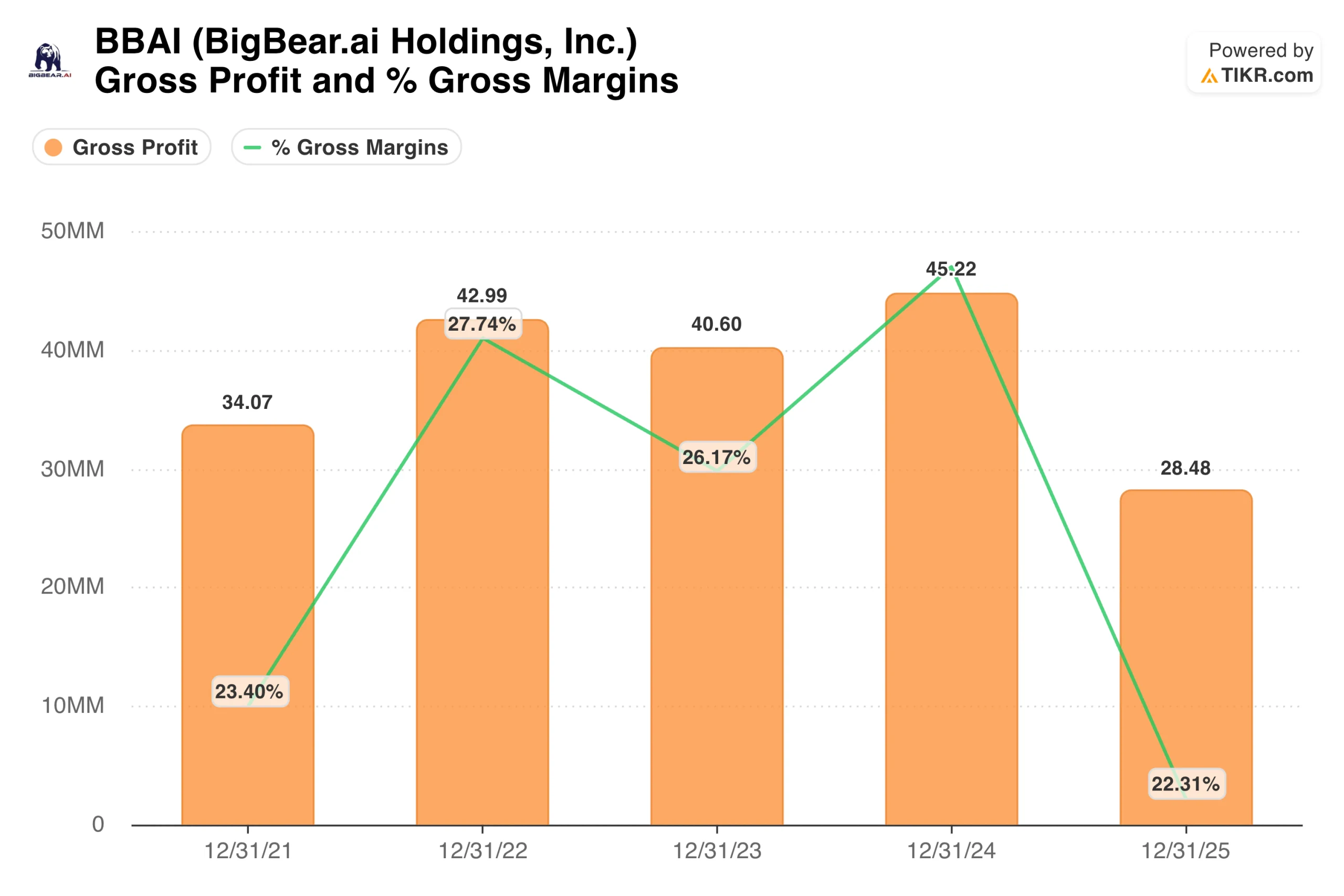

Why the Gross Margin Chart Is the Most Important Visual Here

The gross margin chart shows a business with inconsistent unit economics. Margins expanded from 23% in 2021 to nearly 28% in 2022, dipped back to 26% in 2023, reached roughly 29% in 2024, then fell sharply to 22% in 2025 as lower-margin Army program work dominated the mix.

What the chart cannot show yet is what happened in Q1 2026. Gross margin was 34.0% in Q1 2026, up from 21.3% in Q1 2025, driven by increased volume from Ask Sage’s higher-margin GenAI platforms and products. That is a 1,278-basis-point improvement in one quarter.

This is the signal that matters most for the investment thesis. Ask Sage, acquired in December 2025, is a generative AI platform designed specifically for government and national security use cases. Its software economics are meaningfully better than the services-heavy Army program work that defined 2025.

If BBAI can continue growing the Ask Sage revenue base while stabilizing its core business, the gross margin trajectory should continue to improve. A business that sustains 30% or better gross margins on $150M in revenue is a fundamentally different proposition than the one the 2025 annual numbers suggest.

See what analysts think about BBAI stock right now (Free with TIKR) >>>

What the TIKR Model Implies at the Current Price

The TIKR model targets around $8 per share in the mid case, implying a total return of roughly 84% over about 5.6 years, or about 14% annually. The model uses revenue growth of around 2% per year, which is actually more conservative than management’s own 2026 guidance implies. Net income margins remain deeply negative throughout the forecast period, meaning the return is driven almost entirely by multiple expansion as the market eventually reprices the revenue base.

The low case targets around $6, with roughly 4% annual growth. The high case reaches around $10 at roughly 10% per year. The wide range reflects genuine uncertainty about whether contract wins convert to stable, recurring revenue and whether the margin improvement story holds.

One important number not in the model: BigBear.ai ended 2025 with $462 million in cash and investments and reduced its debt by more than 90%. For a company generating $128M in annual revenue, that cash position is substantial. It eliminates near-term dilution and funding risk, and it gives management the flexibility to invest in the Ask Sage and CargoSeer platforms without financial distress becoming the story.

The Case for BBAI: Defense AI Tailwinds, Balance Sheet Reset, and a Margin Inflection

The balance sheet transformation is real. A year ago, BBAI carried significant convertible debt, creating an overhang on the equity. That debt has been converted or settled. The company now has over $400M in cash against a relatively small debt load, which materially changes the risk profile.

The gross margin expansion to 34% in Q1 2026 is the early evidence that the Ask Sage acquisition is doing what management said it would: shifting the revenue mix toward higher-margin software. If that mix shift continues, the path to breakeven becomes a legitimate scenario rather than a distant hope. CEO Kevin McAleenan noted that Q1 contract wins of roughly $75M demonstrate “our thesis that national security, trade, and travel are two markets we are right to stay laser-focused on serving.”

And the secular backdrop remains favorable. Government AI spending is growing, BBAI has an existing relationship base with hard-to-access agencies, and the Ask Sage platform was specifically designed for the classified and sensitive environments where commercial AI tools cannot operate.

The Risks: Concentration, Ongoing Losses, and a Lot That Has to Go Right

Revenue concentration is the dominant risk. A handful of large government contracts drove both the 2024 peak and the 2025 trough. If the Army programs that wind down are not replaced with comparable work, the 2026 guidance range becomes difficult to achieve, and the thesis stalls.

The losses are significant and not going away soon. A net loss of $56.8M on $34.4M in quarterly revenue means the company is burning cash at a rate that eventually matters, even with $431M in reserves. The path to profitability requires both revenue growth and sustained margin improvement, and both must occur in a business where contract timing is inherently unpredictable.

And the 2026 revenue guidance, while encouraging, requires strong back-half execution. Q1 at $34.4M means the remaining three quarters need to average around $34M each just to reach the low end of guidance. Management’s backlog growth and contract wins suggest that is achievable, but it has not happened yet.

Is BBAI Worth Buying at $4.38?

BigBear.ai is not a stock for every investor. It is pre-profitable, revenue-concentrated, and operating in a government contracting environment where timing disruptions can look like structural deterioration even when they are not.

What the data shows is a company that spent 2025 resetting its financial foundation: cleaning up its balance sheet, acquiring higher-margin software capabilities, and absorbing a painful but contract-specific revenue decline. The Q1 2026 gross margin jump to 34% is the clearest early evidence that the reset is working.

The TIKR mid-case of around $8 at roughly 14% annually is a compelling return if the thesis plays out. The wide range of outcomes in the model reflects the genuine uncertainty of the situation honestly.

For investors who understand the risks, have a multi-year time horizon, and believe the defense AI spending cycle is real, the current price offers exposure to a legitimate theme at a point where the business model may be quietly improving. For investors who need earnings visibility and steady cash flow, BBAI is not the right stock.

See analysts’ growth forecasts and price targets for BBAI stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!