BigBear.ai Holdings (BBAI) sits at the crossroads of artificial intelligence, defense analytics, and national security technology. The Maryland-based firm develops AI-driven “decision intelligence” platforms for U.S. defense and intelligence agencies, as well as clients in logistics, healthcare, and manufacturing. Its products analyze real-time data streams, helping customers anticipate threats, allocate resources, and optimize mission outcomes.

The 2024 acquisition of Pangiam, a leader in computer vision and biometric screening, expanded BigBear’s footprint into transportation and border security, marking a strategic step toward becoming a full-spectrum defense-tech integrator.

This combination of data analytics and visual-recognition AI enables BigBear to compete for larger contracts that integrate operational intelligence with physical security solutions. As governments worldwide modernize defense infrastructure with AI, BigBear’s offerings could find a firmer footing than its volatile small-cap status suggests.

Financial Story: A Reset year, Not a Lost One

Fiscal 2024 was a year of transition and turbulence. Revenue grew modestly by about 2% to $158.2 million, but a non-cash accounting impact tied to convertible-note adjustments caused a steep $296 million pre-tax loss versus $71 million the prior year. Management emphasized that these changes didn’t affect underlying operations; revenue, gross margin, and operating cash flow remained intact. However, the perception of instability rattled investors and weighed on valuation.

| Metric | Period | Value | YoY / Status | Commentary |

|---|---|---|---|---|

| Revenue | FY 2024 | $158.2M | +2.06% vs. 2023 | Modest growth year over year. |

| Pre-tax loss | FY 2024 | $(257.1)M | worse vs. $(71.3)M in 2023 | Driven partly by accounting effects tied to convertible notes. |

| Revenue | Q2 2025 | $32.5M | below Street; miss | Sparked a sharp sell-off post-print. |

| FY 2025 revenue guidance | Updated Aug 2025 | $125–$140M | cut from $160–$180M | Reflects contract timing & program delays; profitability guidance withdrawn. |

| Accounting restatement | Mar 2025 | Convertible-debt presentation | no change to revenue/GM/OCF | But it added uncertainty and contributed to volatility. |

| Strategic scope | 2024–2025 | Defense + Pangiam CV/biometrics | integrating | Expands use cases in secure screening & threat detection. |

Then came Q2 2025, which delivered another surprise: $32.5 million in revenue, missing expectations, and a guidance cut to $125–$140 million, down from the previously expected range of $160–$180 million. The company also pulled its profitability outlook for the year. While painful, management framed the move as a recalibration due to delayed government contract timing, rather than a cancellation of the business. BigBear’s contract model often produces uneven quarters, and until awards flow more predictably, volatility will remain part of the narrative.

Despite the turmoil, the company’s fundamentals haven’t collapsed, only the confidence around timing and visibility. With steady defense demand and new product synergies from Pangiam, BigBear could still reaccelerate into 2026 if its contract cadence normalizes.

1. The Guidance Reset: Reading Between the Lines

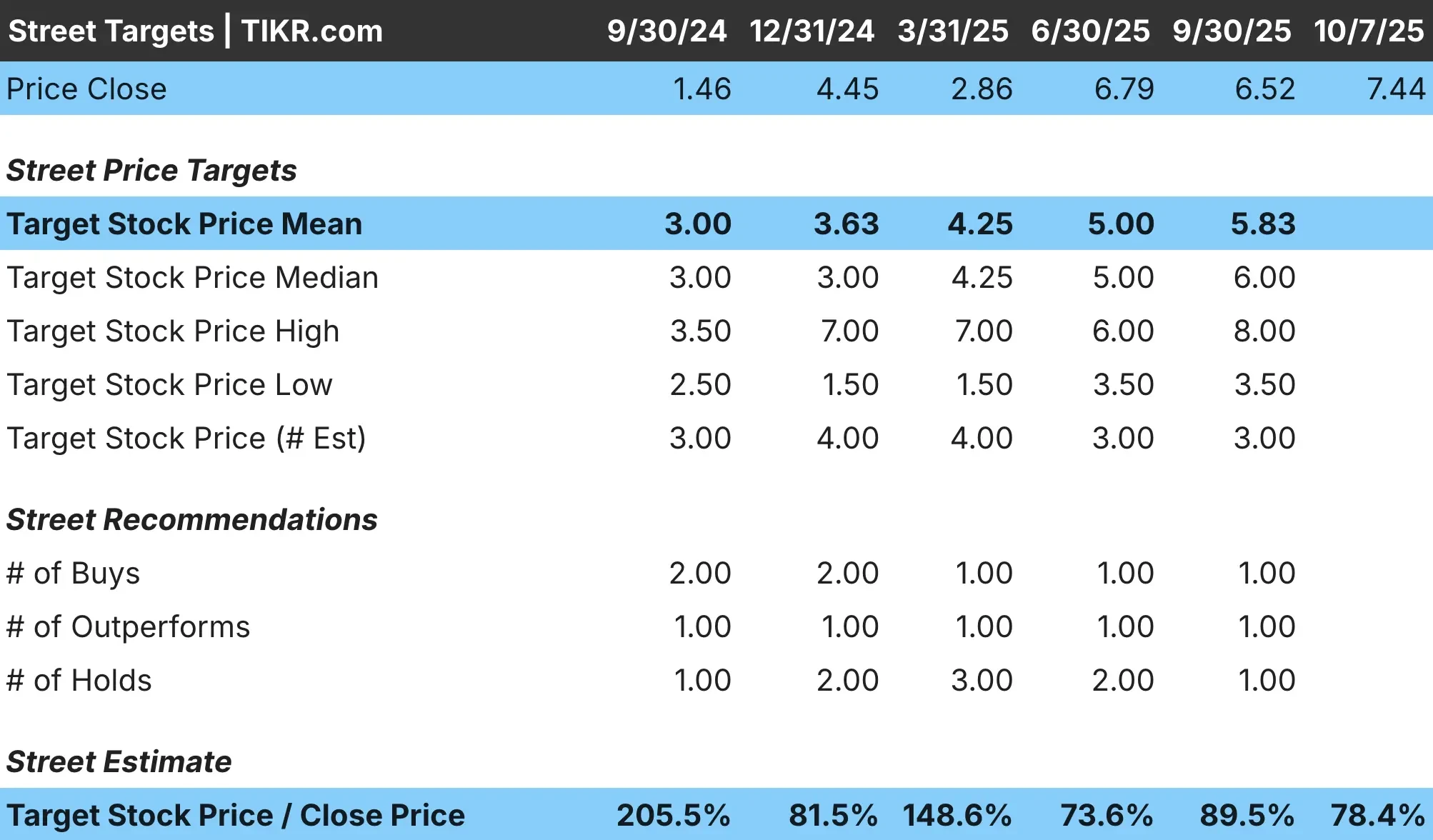

When BigBear cut its 2025 forecast, it framed the move as a matter of contract timing, not lost customers. That distinction matters: in defense technology, contracts often shift quarters due to funding approvals or bureaucratic delays, meaning lost revenue in one period can reappear in another. Investors punished the stock anyway, sending shares down sharply after the announcement.

Yet, there’s a subtler story underneath. Defense AI remains a budget-protected sector within U.S. and NATO modernization efforts, and BigBear’s analytics suite supports exactly the kind of operational intelligence those governments are prioritizing. If management executes even modestly on its backlog, the revenue decline may prove temporary. Investors will be watching closely for signs of rebound in late 2025 contract conversions, especially within the Air Force and Army logistics pipelines.

2. Profit Path: Prove It Before You Price It

The company’s March 2025 accounting restatement, which clarified convertible debt reporting but left core results unchanged, reinforced investor skepticism about its internal processes. Combined with a nearly $257 million loss in 2024, this underscored how far BigBear must go before achieving credible profitability. Restatements can erode trust, even when non-cash, and the company must now rebuild that confidence incrementally.

To its credit, BigBear has begun implementing stronger cost controls and realigning its go-to-market model around higher-margin defense and infrastructure projects. These contracts tend to have multi-year lifecycles and steadier margins, which could stabilize free cash flow as the company scales.

Still, Wall Street will likely wait for proof: analysts want to see two consecutive profitable quarters before re-rating the stock. The roadmap exists; it’s execution that remains the hurdle.

Value stocks in less than 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

3. Strategic Optionality: From Defense AI to Biometric Security

The Pangiam acquisition may ultimately prove the most transformative piece of BigBear’s strategy. Pangiam’s biometric and computer-vision platforms power security screening at airports, ports, and border checkpoints, markets that continue to see substantial public-sector investment. Integrating those capabilities with BigBear’s predictive analytics could give the combined company a differentiated edge: software that not only sees and identifies threats but also anticipates and models them.

If BigBear can integrate these systems into a single, modular platform, it could open new recurring-revenue streams tied to infrastructure modernization and critical asset protection. Such projects tend to attract steady funding, insulating results from the commercial-AI hype cycle. While integration risk remains, the strategic logic is sound, positioning BigBear less as a speculative AI play and more as a future-ready defense infrastructure company.

The TIKR Takeaway

BigBear.ai remains a high-volatility, “show-me” turnaround story, but one with undeniable potential if its defense contracts and Pangiam integration align. The 2025 reset cleared inflated expectations, allowing fundamentals to catch up to narrative. The company is no longer being priced like a moonshot; it’s being valued like a rebuilding mid-cap with optionality in defense, homeland security, and applied AI.

If management can demonstrate revenue consistency and progress toward achieving a positive cash flow, BigBear could transition from a speculative to a strategic holding in 2026. For now, investors are paying primarily for future execution, not current results, and that makes patience the core investment requirement.

Should You Buy, Sell, or Hold BigBear.AI?

- Consider if: You believe in the long-term defense-AI trend and are comfortable with small-cap volatility tied to government-contract timing. The story appeals to investors who view national-security AI as a secular theme rather than a short-term trade.

- Watch for: Large contract awards, integration milestones from Pangiam, and any signal of operating leverage through gross-margin stability or improved free cash flow. Those will be the earliest signs of a fundamental turnaround.

- Risks: Persistent losses, financing needs if cash flow lags, and exposure to sentiment shifts in the broader AI market. Short-term pullbacks could be sharp if award timing disappoints again.

BigBear.ai has stumbled, but it hasn’t fallen out of the race. With credible execution and a defense-focused identity, 2026 could mark the beginning of a quieter, steadier climb for this once-hyped AI contender.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie in the AI application layer, where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!