Key Stats for GTX Stock

- Past-Week Performance: 7%

- 52-Week Range: $10 to $32

- Valuation Model Target Price: $37

- Implied Upside: 20%

Analyze your favorite stocks like Garrett Motion with TIKR (It’s free) >>>

What Happened?

Garrett Motion Inc. stock rose about 7% this week, finishing near $31 per share as investors reacted to stronger Q1 results, raised 2026 guidance, analyst target increases, and newly released institutional positioning data.

The stock moved higher because Garrett’s Q1 results showed the company is gaining share in gasoline turbo and recovering in commercial, off-highway, and industrial markets, even while light vehicle production remains weak. Stronger margins and a higher 2026 outlook made the rally look tied to real earnings improvement, not just a short-term trading move.

This week’s earnings call showed Q1 net sales of $985 million, up 12% year over year on a reported basis and 6% at constant currency, with adjusted EBIT of $151 million, a 15.3% adjusted EBIT margin, and $49 million of adjusted free cash flow.

CEO Olivier Rabiller said the quarter was driven by “share of demand gains in gasoline turbo” and growth in commercial vehicle, off-highway, and industrial markets, while Garrett also repurchased $87 million of common stock, paid $16 million in dividends, and raised its 2026 outlook to midpoint targets of $3.75 billion in net sales, $560 million of adjusted EBIT, and $415 million of adjusted free cash flow.

Analyst updates helped support the move. BWS Financial raised its Garrett Motion price target to $32 from $22, Deutsche Bank lifted its target to $24 from $19, JPMorgan raised its target to $33 from $30, and Stifel set one of the higher targets at $36, while Fintel data showed Garrett’s average one-year price target increased 27% to about $29.

Recent filings showed a mixed institutional picture, with Mitsubishi UFJ Trust & Banking cutting its stake by 41.2%, Seizert Capital Partners reducing its position by 27.8%, and Comerica Bank increasing its stake by 22%.

Value Garrett Motion instantly (Free with TIKR) >>>

Is GTX Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth: 5%

- Operating Margins: 15%

- Exit P/E Multiple: 13x

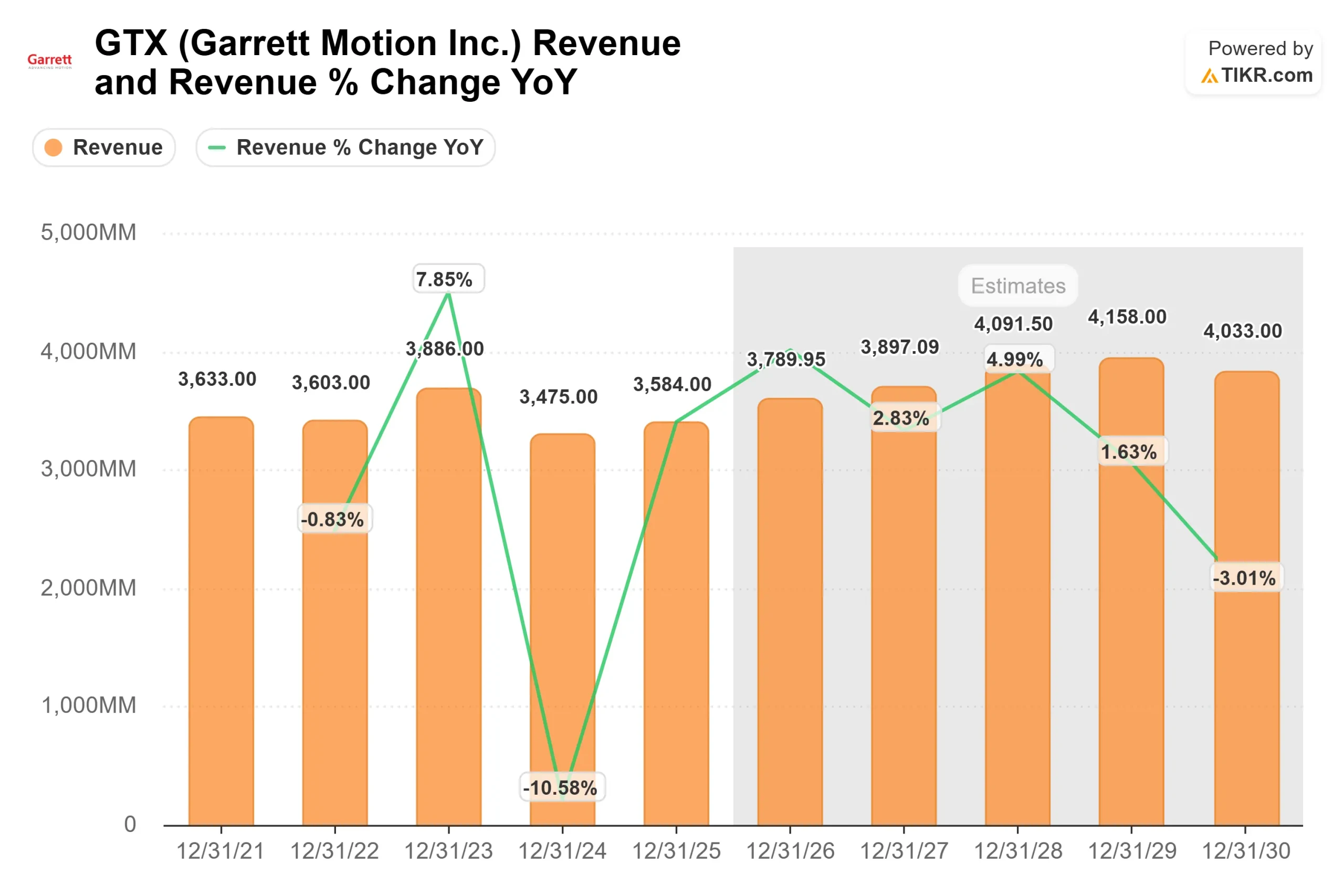

Garrett’s setup is not built on explosive revenue growth. The model assumes revenue rises from about $3.6 billion in 2025 to about $4.1 billion by 2028, which points to steady expansion rather than a high-growth story.

That makes margin execution and cash flow more important than fast top-line growth. Garrett’s latest quarter showed the company can grow through share gains and stronger commercial, off-highway, and industrial demand while still converting earnings into cash.

The company’s business drivers are more specific than just auto production. Garrett sells turbocharging and motion-control technologies that help automakers improve efficiency, and demand from gasoline, hybrid, commercial vehicle, off-highway, and industrial applications gives the business more than one path to growth.

See analysts’ growth forecasts and price targets for Garrett Motion (It’s free) >>>

Hybrid demand is especially important because automakers still need more efficient combustion systems even as the industry shifts toward electrification. That could give Garrett a longer runway than a supplier tied only to traditional internal combustion vehicle volumes.

Based on these inputs, the model estimates a target price of $37, implying about 20% total upside over roughly 2.6 years, which suggests Garrett Motion appears modestly undervalued at current prices.

The next 12 months will likely depend on whether Garrett can turn its raised outlook into consistent cash flow. Strong adjusted free cash flow gives the company more room to support dividends, reduce debt, repurchase shares, and invest in newer growth areas without leaning heavily on outside capital.

Margin durability is another key factor. The model assumes operating margins of about 15%, so Garrett’s pricing, product mix, and productivity efforts need to stay strong enough to offset normal cost pressure across the auto supplier industry.

Commercial vehicle, off-highway, and industrial demand could also help results if those markets continue improving. These areas matter because they can add growth outside passenger vehicles and make Garrett’s revenue base less dependent on one part of the auto cycle.

At current levels, Garrett Motion appears modestly undervalued, with future performance driven by margin execution, cash flow, hybrid-related demand, and continued strength in commercial and industrial end markets rather than aggressive revenue acceleration.

How Much Upside Does GTX Stock Have From Here?

Investors can estimate Garrett Motion’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Garrett Motion in under 60 seconds with TIKR (It’s free) >>>