Key Takeaways:

- AbbVie (ABBV) beat Q1 2026 estimates with adjusted EPS of $2.65 versus the $2.59 consensus estimate. Revenue rose 12.4% year-over-year to $15 billion on strong Skyrizi and Rinvoq demand.

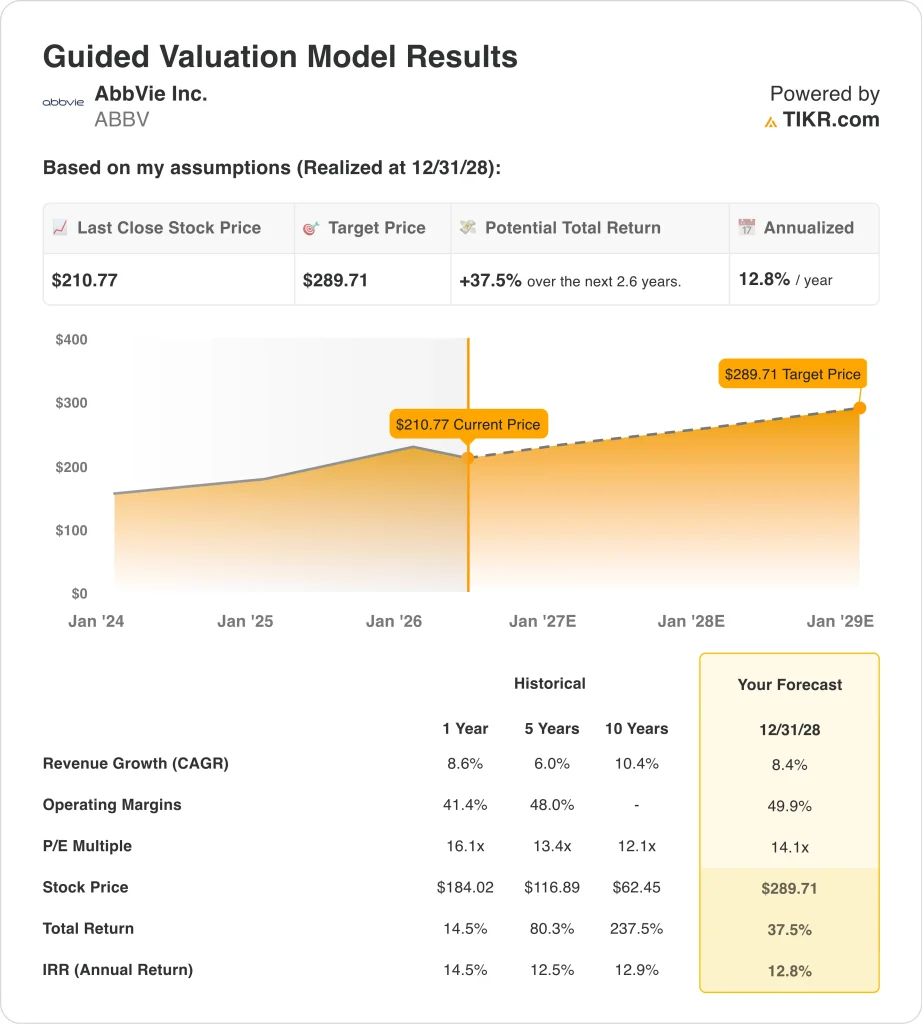

- ABBV stock trades at around $211, up about 22% over the past year. Analysts maintain a consensus target price of around $253.

- ABBV stock could rise from $211 to around $290 per share by December 2028. That implies a total return of around 38% and an annualized return of around 13%.

What Happened?

AbbVie Inc. (ABBV) delivered a solid Q1 2026 earnings beat on April 29, 2026. Adjusted EPS came in at $2.65, ahead of the $2.59 analyst estimate. Revenue grew 12.4% year-over-year to $15 billion. And management raised its full-year adjusted profit outlook on continued demand strength.

The growth story at AbbVie centers on two key newer drugs. Skyrizi is an immunology drug approved for plaque psoriasis and Crohn’s disease. And Rinvoq treats rheumatoid arthritis and other inflammatory conditions.

Together, they are more than offsetting the ongoing revenue decline of Humira, AbbVie’s former flagship drug that is now facing biosimilar competition from lower-cost generic versions.

Rinvoq recently demonstrated superiority over Humira for the primary endpoint in a rheumatoid arthritis clinical study. And AbbVie submitted an FDA application for Rinvoq in severe alopecia areata, which is an immune-related hair loss condition, in April 2026.

But the FDA declined to approve a separate AbbVie wrinkle treatment due to manufacturing concerns. So the pipeline has both positive momentum and some setbacks to navigate.

AbbVie also pays a quarterly dividend of $1.73 per share, which translates to a dividend yield of about 3.3%. So income-focused investors benefit from a meaningful payout alongside any capital appreciation. Analyst consensus still points to fair value above current prices.

Here’s why AbbVie stock could continue delivering attractive returns through 2028 as its newer immunology drugs drive durable revenue and earnings growth.

What the Model Says for ABBV Stock

We analyzed the upside potential for AbbVie stock based on its growing immunology franchise, expanding Skyrizi and Rinvoq indications across new disease areas, and resilient cash flow generation supporting dividends and reinvestment.

Based on estimates of around 8% annual revenue growth, around 50% operating margins, and a normalized P/E multiple of around 14x, the model projects AbbVie stock could rise from $211 to around $290 per share.

That would be a total return of around 38%, or around 13% annualized over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ABBV stock:

1. Revenue Growth: 8.4%

AbbVie delivered Q1 2026 revenue of $15 billion, up 12.4% year-over-year. Growth was driven by strong Skyrizi and Rinvoq demand across existing and new indications. And both drugs continue winning approvals in additional disease areas, expanding their total addressable patient populations.

Based on analysts’ consensus estimates, we used around 8% annual revenue growth. This reflects AbbVie’s diversified drug portfolio and ongoing Skyrizi and Rinvoq expansion, balanced against continued Humira biosimilar erosion. And the company’s forward two-year revenue CAGR of around 9% aligns closely with this estimate.

So 8% represents a realistic growth trajectory. AbbVie’s active pipeline also includes new FDA submissions for upadacitinib in alopecia areata and Skyrizi in Crohn’s disease. And these additional approvals, if granted, could provide incremental revenue streams beyond the current portfolio.

2. Operating Margins: 49.9%

AbbVie’s last-twelve-months gross margin is around 72%, and its LTM EBIT margin is around 35%. The company has room to expand operating margins as newer high-margin drugs scale. Reduced spending on mature products like Humira should improve overall margin efficiency over time.

Based on analysts’ consensus estimates, we used around 50% operating margins. This reflects the inherently high profitability of pharmaceutical companies at scale. And it accounts for AbbVie’s continued R&D investments in pipeline drugs and new indications for Rinvoq and Skyrizi.

AbbVie’s forward two-year EBITDA CAGR is around 23%, suggesting significant earnings power improvement ahead. So the 50% operating margin target reflects achievable improvement from current levels. And the company’s strong cash generation supports both dividends and ongoing reinvestment in the pipeline.

3. Exit P/E Multiple: 14.1x

AbbVie currently trades at a next-twelve-months P/E of around 14x. This is a modest multiple for a large-cap pharmaceutical company with a strong branded drug portfolio. It reflects lingering investor concern about the Humira transition but does not fully credit the growth potential of Skyrizi and Rinvoq.

Based on analysts’ consensus estimates, we maintained a normalized P/E multiple of around 14x. This reflects the pharmaceutical sector’s typical valuation range and AbbVie’s stable earnings profile. And it incorporates some uncertainty around the pace of the Humira transition and pipeline execution risk.

The 3.3% dividend yield adds meaningful total return support beyond stock price appreciation. So even without multiple expansion, AbbVie offers income alongside earnings growth. And if Rinvoq and Skyrizi scale faster than expected, multiple expansion becomes a meaningful additional catalyst.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for ABBV stock through 2034 show varied outcomes based on Skyrizi and Rinvoq growth, pipeline execution, and the pace of Humira erosion (these are estimates, not guaranteed returns):

- Low Case: Humira decline accelerates faster than expected, and pipeline approvals disappoint → around 5% annual returns

- Mid Case: Skyrizi and Rinvoq sustain growth momentum, and new indications expand the pipeline’s revenue contribution → around 7% annual returns

- High Case: Multiple pipeline approvals and new drug launches drive accelerating revenue and earnings growth → around 10% annual returns

Going forward, AbbVie’s longer-term performance depends heavily on how successfully its newer immunology drugs replace the lost Humira revenue. The mid-case scenario implies around 7% annual returns through 2034, which falls below the 10% threshold many equity investors target.

But the shorter-term model through 2028 shows a more attractive around 13% annualized return, and near-term pipeline catalysts like the Rinvoq superiority data and new FDA submissions could provide meaningful additional upside.

See what analysts think about ABBV stock right now (Free with TIKR) >>>

Should You Invest in AbbVie?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ABBV, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ABBV alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!