Key Stats

- 52-Week Range: $376 to $652

- Current Price: $502

- Street Mean Target: $538

- Street High Target: $650

- TIKR Model Target (Dec. 2030): $930

Synopsys Stock Jumps as Elliott Takes a Multibillion-Dollar Stake and the Ansys Integration Accelerates

Synopsys (SNPS) is the world’s leading provider of electronic design automation software, the mission-critical tools semiconductor companies use to design and verify chips before manufacturing, and following Q1 fiscal 2026 earnings and an activist entry by Elliott Investment Management, the stock is trading at a meaningful discount to where it stood just six months ago.

Elliott Investment Management disclosed a multibillion-dollar stake in Synopsys stock in March, telling the Wall Street Journal there is a “clear opportunity for Synopsys’ financial performance to more fully reflect the value it delivers.”

The activist entry arrived as Synopsys was already executing a significant strategic transformation: the $35 billion acquisition of Ansys, a leading simulation and analysis software provider, closed in mid-2025 and added an entirely new engineering software platform to the portfolio.

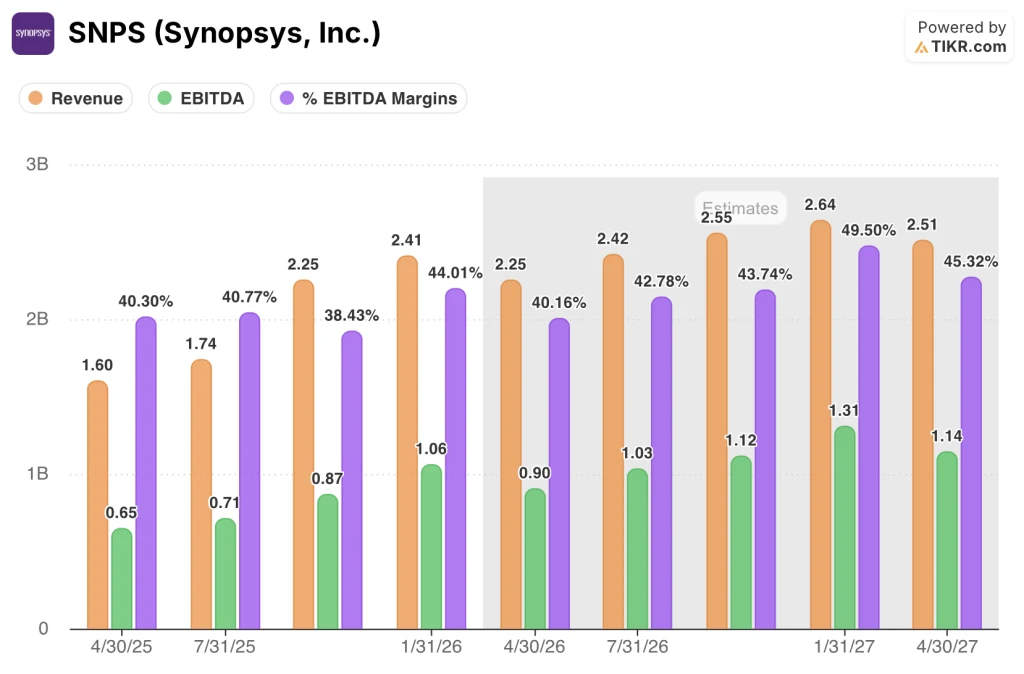

Q1 fiscal 2026 was the first quarter reflecting Ansys as a fully integrated business, and the company delivered revenue of $2.41 billion, at the high end of guidance, while non-GAAP EPS of $3.77 came in ahead of expectations.

Ansys alone contributed approximately $886 million of that Q1 revenue, reflecting seasonally strong year-end deal flow from the legacy Ansys business, and CFO Shelagh Glaser noted on the earnings call that the Ansys portfolio demonstrated “broad opportunity really across all those segments.”

CEO Sassine Ghazi summarized the quarter directly on the Q1 2026 earnings call: “We said what we’re going to do, and we did it.”

Synopsys also repaid the entirety of its $4.3 billion in term loans within six months of closing the Ansys deal, ahead of the original three-year paydown schedule, and followed that with a $250 million accelerated share repurchase agreement announced in March and a $2 billion stock repurchase authorization from the board.

The company reiterated its full-year revenue guidance of $9.56 billion to $9.66 billion while raising its full-year non-GAAP EPS guidance by $0.06 to a range of $14.38 to $14.46, citing better-than-expected net interest expense from the accelerated debt paydown.

Wall Street’s Take on SNPS Stock

The central question for investors in Synopsys stock right now is not whether the company is growing — it clearly is — but whether a transitional year in the IP business and the lingering discount to pre-Ansys price levels represent a structural problem or a setup.

Wall Street’s answer leans constructively bullish. Of the 26 analysts covering SNPS, 15 rate it a Buy, 2 rate it Outperform, 7 rate it Hold, and 1 rates it Underperform, with a mean price target of around $538, implying around 7% upside from the current price of $502.42.

The consensus growth thesis centers on revenue: analysts project Synopsys to generate around $2.25 billion in the April 2026 quarter, representing around 40% year-over-year growth, driven by the Ansys contribution, with full-year consensus revenue estimates pointing to a combined business approaching the high end of Synopsys’ guided $9.56 billion to $9.66 billion range.

EBITDA tells the margin expansion story. Consensus estimates project EBITDA of around $900 million for the April 2026 quarter, growing to around $1.03 billion in the July 2026 quarter, with EBITDA margins expanding from 40.2% to around 43% as the company accelerates its $400 million cost synergy target ahead of its original three-year schedule.

Elliott’s entry hardened the bull case. The firm’s public statement that Synopsys has room to “boost sales and improve margins” is essentially an endorsement of the thesis that the Ansys deal was underpriced by the market and that a focused push on monetization — particularly through the agentic AI engineering tools Ghazi outlined at the Morgan Stanley TMT Conference in March — could accelerate the growth trajectory meaningfully.

The bear case, and the reason 7 analysts remain on Hold, centers on the IP segment. Design IP revenue came in at $407 million in Q1, down approximately 6% year-over-year, and management explicitly characterized fiscal 2026 as a “transitional year” for the business, citing delayed title deliveries, the planned divestiture of the ARC processor business to GlobalFoundries, and headwinds from China, where cumulative technology export restrictions have compressed demand from domestic chip designers.

The China exposure is also real but bounded. Excluding Ansys, Synopsys’ China revenue declined slightly year-over-year in Q1, consistent with management’s guidance, and the company has explicitly derisked its China assumptions for the full year by modeling no new design starts with a major unnamed foundry customer.

The mean analyst price target of around $538 against a current price of $502 implies only modest near-term upside, but that gap understates the valuation case: the stock has fallen from a 52-week high of $652, meaning a reversion to prior Street consensus alone would represent a 30% move.

With backlog of $11.3 billion providing revenue visibility and management committing to accelerating both $400 million cost synergy and $400 million revenue synergy targets ahead of schedule, Synopsys stock appears undervalued relative to the scale of the combined business and the earnings power embedded in that backlog, with the IP segment’s recovery the key variable that determines the pace of re-rating.

What Does the Valuation Model Say?

TIKR’s base case values Synopsys at $930 per share, anchored to a mid-case revenue CAGR of around 11% from fiscal 2025 through 2035 and a normalized net income margin of 32.5%, assumptions grounded in the combined Synopsys plus Ansys platform’s demonstrated ability to compound revenue through multi-year customer agreements and a $11.3 billion backlog.

At $502 against a TIKR base case of $930 and a mid-case 10-year price forecast of around $1,063, Synopsys stock appears undervalued by a margin that the current analyst consensus mean of $538 significantly understates.

The single variable the entire argument hinges on is whether the IP segment’s transitional headwinds in fiscal 2026 prove temporary or structural: if Synopsys delivers on its road map of high-speed interface IP titles for HPC and hyperscaler customers in the second half of the year, the base case holds and the discount closes.

Bull Case

- TIKR’s high-case scenario projects revenue CAGR of around 12% through 2035, with a net income margin of 33.9%, yielding a stock price forecast of around $1,361 by fiscal 2035

- The $400 million cost synergy target is being accelerated into fiscal 2026 and 2027, ahead of the original three-year schedule, compressing the path to margin normalization

- EBITDA margins are already at 44% in Q1 fiscal 2026, expanding toward consensus estimates of around 50% by fiscal 2027, as Ansys deal costs amortize and cross-selling kicks in

- Backlog of $11.3 billion provides multi-year revenue visibility, reducing execution risk on the double-digit growth target for both EDA and simulation and analysis segments

- Elliott’s multibillion-dollar stake adds a direct activist catalyst for capital return acceleration and operating margin improvement beyond what management has already committed

Bear Case

- TIKR’s low-case scenario prices Synopsys at around $809 per share by fiscal 2035 on revenue CAGR of just under 10% and a net income margin of 30.7%, assuming IP headwinds persist longer than guided

- China design starts remain suppressed by export restrictions with no clear catalyst for reversal, and Synopsys’ outsized IP exposure in that market versus peers creates an asymmetric downside risk relative to Cadence Design Systems

- The ARC processor divestiture, still pending close with GlobalFoundries, introduces execution noise into an already transitional year for the IP segment

- EPS Normalized has declined year-over-year in recent quarters, with consensus projecting around (14%) year-over-year change for the April 2026 quarter before recovering, creating a near-term earnings optics headwind

- Integration risk on the $35 billion Ansys deal is real: revenue synergy monetization is not expected until fiscal 2027 at the earliest, leaving a multi-quarter window where the combined business must justify a premium valuation on cost synergies alone

Should You Invest in Synopsys, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Synopsys, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Synopsys, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SNPS stock on TIKR for Free →