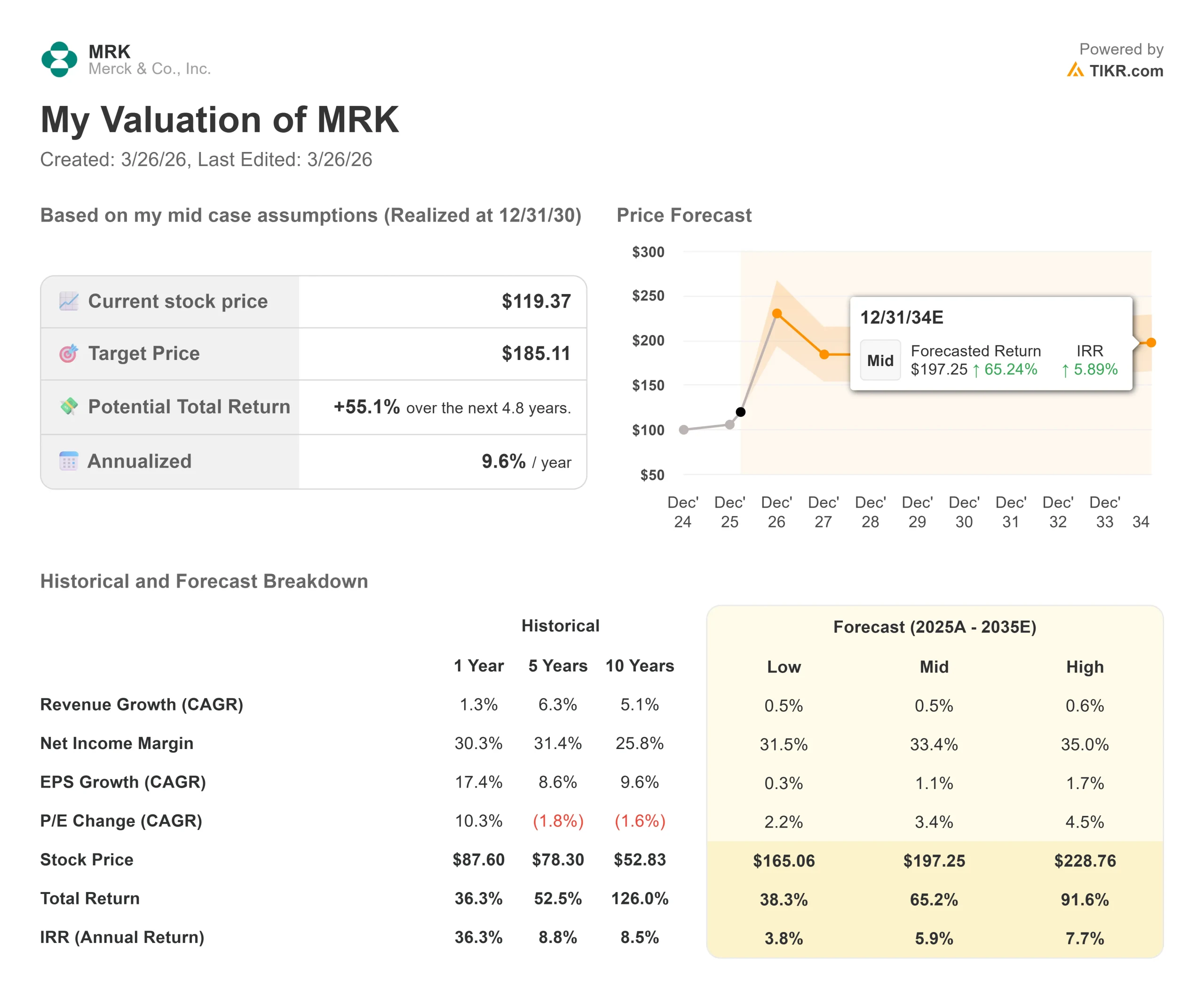

Key Stats for Merck Stock

- Current Price: $119.37

- Target Price (Mid): $185.11

- Street Target (Mean): $128.04

- Potential Total Return: +55.1%

- Annualized IRR: 9.60% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Merck (MRK) stock has spent two years under one shadow: the looming expiration of Keytruda’s U.S. patent in December 2028.

Bulls say the pipeline is deep enough to bridge the gap. Bears say nothing in pharma replaces a blockbuster cleanly. This week, Merck made its most pointed response to that debate.

On March 25, 2026, Merck announced it would acquire Terns Pharmaceuticals for $53 per share in cash, an equity value of approximately $6.7 billion, or roughly $5.7 billion net of acquired cash.

MRK shares rose $3.00, or 2.58%, to close at $119.37 on announcement day. The reaction was measured, not euphoric.

The asset at the center of the deal is TERN-701, an investigational oral allosteric BCR::ABL tyrosine kinase inhibitor (a targeted drug that blocks the protein driving CML cancer cell growth) being studied in patients with chronic myeloid leukemia, or CML, a slow-growing blood cancer arising from bone marrow.

CML affects an estimated 18,000 newly diagnosed patients each year across the U.S., key European markets, and Japan.

CEO Robert Davis was direct on the acquisition call: “We believe TERN-701 has the potential to be a best-in-class therapy, driven by high selectivity and an improved therapeutic index that could lead to efficacy advantages versus currently approved TKI agents.

“This is Merck’s third multibillion-dollar acquisition in roughly twelve months.

The prior $10 billion purchase of Verona Pharma and the $9.2 billion deal for Cidara Therapeutics bring the total to approximately $25.9 billion in committed capital across three deals, all aimed at building pipeline depth before Keytruda revenues fall.

See historical and forward estimates for Merck stock (It’s free!) >>>

Is Merck Undervalued Today?

MRK trades at 23.28x NTM P/E and 15.50x NTM EV/EBITDA as of March 25, 2026.

The premium over distressed peers is straightforward to explain.

Pfizer trades at 9.21x NTM P/E and Bristol-Myers Squibb at 9.40x, both facing steep patent cliffs with fewer credible replacement assets in late-stage development. Novartis trades at 16.76x and AstraZeneca at 18.20x, richer multiples backed by pipeline momentum.

Merck’s 23.28x assumes its own transition plays out. That assumption rests largely on what Terns brings.

According to BioPharma Dive, data presented at the American Society of Hematology meeting in December 2025 suggested TERN-701 could challenge Novartis’ Scemblix, a drug with peak annual sales potential exceeding $4 billion.

William Blair analyst Andy Hsieh called TERN-701’s clinical profile “unprecedented” in CML. Leerink Partners’ Andrew Berens wrote that Merck’s offer “vastly underestimates” TERN-701’s potential, with his model projecting approximately $6.2 billion in peak-year revenue.

What makes TERN-701 different is its mechanism.

Unlike traditional TKIs that compete for the active site of the BCR::ABL cancer-driving protein, TERN-701 targets a distinct allosteric pocket, meaning it binds to a separate region designed to overcome the resistance mutations that cause patients to fail existing therapies over time.

As Dr. Dean Li, President of Merck Research Laboratories, stated on the call, early data suggest TERN-701 may achieve approximately double the major molecular response rate and two to three times the deep molecular response rate of approved TKIs, including Scemblix.

The bears have a real counterargument. TERN-701 is still in Phase 1/2 clinical testing.

The 6% premium paid over Terns’ last closing price was among the lowest for a publicly traded drugmaker in years, prompting William Blair to suggest a competing bid could still emerge.

CFO Caroline Litchfield confirmed the deal will trigger an R&D charge of approximately $5.8 billion, or roughly $2.35 per share, in 2026, on top of charges already embedded from Cidara.

The IRA pressure compounds the near-term noise. Januvia’s 79% Medicare price cut takes effect in 2026, and the Janumet franchise faces negotiated pricing in 2027.

See Merck’s full FCF history and forward model on TIKR >>>

TIKR Advanced Model Analysis

Key Stats:

- Current Price: $119.37

- Target Price (Mid): $185.11

- Potential Total Return: +55.1%

- Annualized IRR: 9.60% / year

See analysts’ growth forecasts and price targets for Merck stock (It’s free!) >>>

The mid-case uses a 0.5% revenue CAGR through 12/31/30, reflecting near-term biosimilar pressure on Keytruda offset by two drivers: the commercial ramp of Winrevair in pulmonary arterial hypertension (high blood pressure in the lung arteries), and the building contribution from nemtabrutinib and zilovertamab vedotin across hematology. A 33.4% net income margin in the mid-case reflects operating leverage from the $3 billion cost reduction program. The primary risk is a sharper-than-expected Keytruda revenue decline beginning late 2028, compounded by slower adoption of the subcutaneous Keytruda formulation (a rapid-injection version designed to retain patients ahead of biosimilar entry).

The high case reaches $228.76 if TERN-701 earns approval and captures meaningful CML share while Winrevair and hematology push margins toward 35%. The low case at $165.06 reflects near-zero revenue growth and multiple compression if the transition disappoints. At $119.37, the mid-case delivers a 9.60% annualized return through year-end 2030. For a company paying a 2.8% dividend yield with $14.57 billion in cash, that is not a heroic assumption.

Conclusion: Watch Q1 2026 revenue when Merck reports, expected in late April. Management guided $65.5 to $67.0 billion for the full year in February. A reaffirmation signals that the acquisition charges are noise. A cut validates the bears’ concern that the dealmaking pace is outrunning near-term delivery.

Merck’s thesis is straightforward: spend aggressively today so there is no revenue cliff to explain in 2029. The Terns deal adds the most scientifically credible hematology asset the company has acquired. If TERN-701 delivers in Phase 3 what it has shown in Phase 1/2, the $5.7 billion net price may one day look like a bargain. What has to go right is the data. What could go wrong is that it doesn’t.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Merck?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Merck, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Merck alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!