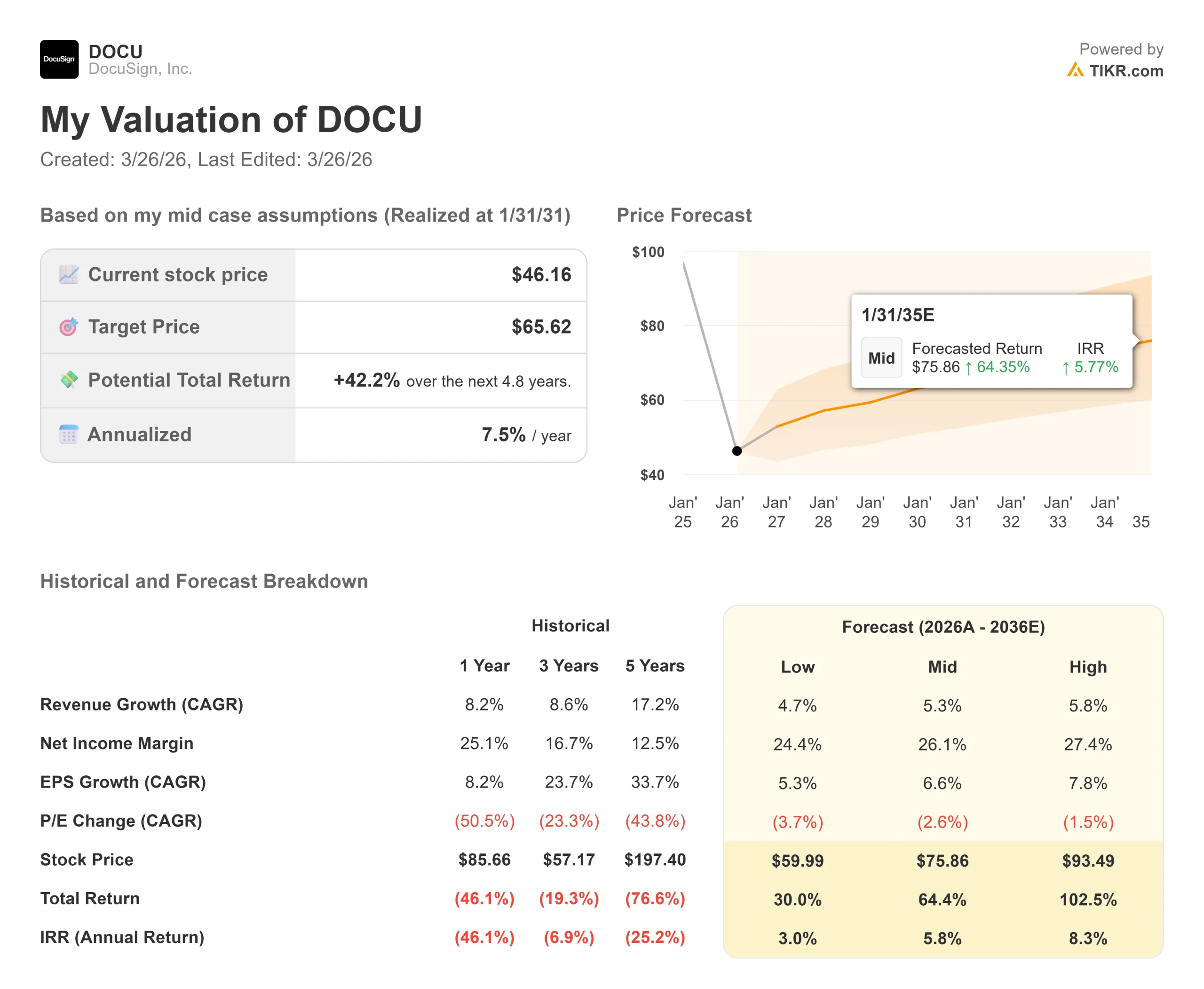

Key Stats for DocuSign Stock

- Current Price: $46.16

- Target Price (Mid): $65.62

- Street Target (Mean): $64.55

- Potential Total Return: +42.2%

- Annualized IRR: 7.50% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Few software stocks carry as much emotional baggage as DocuSign (DOCU).

It soared tenfold during the pandemic, then collapsed as remote-work tailwinds faded, and it has spent three years trying to convince a skeptical market that its best days are not behind it.

The stock now sits at $46.16, down 55.51% from its 52-week high of $94.67, near levels that predate its $3 billion revenue milestone, $1 billion in free cash flow, and 30% operating margins.

Bulls say the selloff has overshot reality. Bears say a company growing at 8% annually deserves a compressed multiple, and they are not convinced the growth rate is going anywhere fast.

The most recent catalyst is the Q4 fiscal 2026 earnings report, released March 17, 2026.

DocuSign beat on revenue ($836.9 million versus the $828.2 million consensus) and on non-GAAP EPS ($1.01 versus $0.95 expected).

What drew as much attention as the results was the simultaneous announcement of a $2 billion increase to DocuSign’s share repurchase authorization, bringing total remaining capacity to $2.6 billion.

CFO Blake Grayson noted on the call that DocuSign established a 10b5-1 program allowing buybacks before the post-earnings open trading window, and had already repurchased $158 million in Q1 fiscal 2027 at the time of the call.

For a sub-$9 billion market cap company, that is a meaningful commitment.

CEO Allan Thygesen framed the moment directly. “In fiscal 2026, DocuSign’s AI-native IAM platform established clear market leadership as the agreement system of action for companies of all sizes,” he said.

“We are positioned to begin accelerating the business.”

The word “accelerating” is doing significant work in that sentence. The market wants to see what it means in ARR dollars over the coming quarters.

See historical and forward estimates for DocuSign stock (It’s free!) >>>

Is DocuSign Undervalued Today?

At $46.16, DOCU trades at 2.38x NTM (next twelve months) EV/Revenue and 8.02x NTM market cap to free cash flow.

For context, those same multiples sat at 6.05x and 20.72x just twelve months ago.

The compression reflects the growth uncertainty, not a deterioration in the underlying business model.

The mean price target is $64.55, representing 39.8% upside from the current price.

Post-earnings, the analyst community responded with broad target cuts rather than upgrades:UBS lowered its target to $54 from $75 (Neutral).

The pattern is not abandonment. It is a wait-and-see posture on growth reacceleration.

The growth story depends on IAM (Intelligent Agreement Management, DocuSign’s AI-native platform for automating agreement workflows end-to-end).

After 18 months on the market, IAM has reached $350 million in ARR, or 10.8% of DocuSign’s total base, up from 2.3% a year earlier.

Management has guided IAM to reach approximately 18% of total ARR by fiscal year-end 2027, meaning IAM ARR would exceed $600 million.

Early IAM renewal cohorts are performing better than the company average on gross and dollar net retention, though the sample size remains limited.

The competitive picture is relevant here.

Atlassian, a workflow software company with comparable enterprise ambitions and a similar revenue scale, trades at 2.49x NTM EV/Revenue. Adobe, whose Acrobat Sign competes directly in eSignature, trades at 3.63x NTM EV/Revenue.

On a free cash flow basis, DocuSign at 8.02x NTM MC/FCF sits below the peer group median of 8.88x. The discount reflects growth uncertainty, not a structural flaw.

The risk the bears are holding is legitimate.

DocuSign’s fiscal 2027 revenue guidance of $3.484 to $3.496 billion implies 8% growth at the midpoint.

The company’s aspiration for double-digit top-line growth carries no firm timeline.

When pressed directly on the earnings call, Grayson said only: “The when on that is not as important to me at the moment.”

That answer is the clearest explanation for why analyst targets moved down, not up, after a quarter where the company beat EPS estimates by 6.4%.

The counterargument is the capital return math.

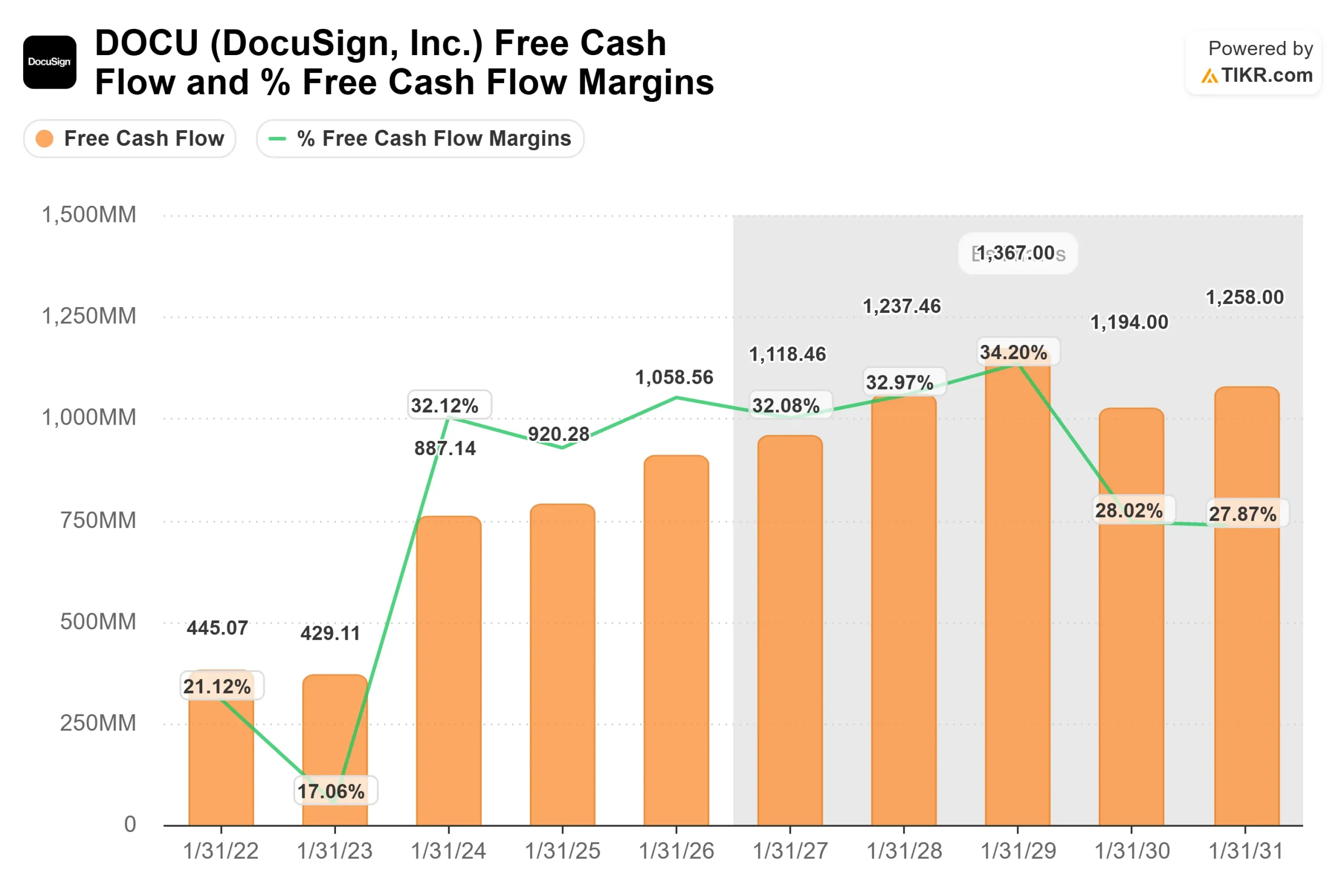

DocuSign repurchased $869 million in stock in fiscal 2026, equal to 82% of its annual free cash flow.

See how DocuSign performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $46.16

- Target Price (Mid): $65.62

- Potential Total Return: +42.2%

- Annualized IRR: 7.50% / year

See analysts’ growth forecasts and price targets for DocuSign stock (It’s free!) >>>

The TIKR mid-case uses a 5.3% revenue CAGR (compound annual growth rate) through the forecast period, supported by two drivers: IAM platform expansion into enterprise accounts, and gross retention improvement in the core eSignature base. The margin driver is continued operating leverage, with a 26.1% net income margin at mid-case. The primary risk is the cloud infrastructure migration, which has already created 50 to 80 basis points of gross margin headwind this year and is not yet complete.

The upside case reaches $93.49 at a 5.8% revenue CAGR and 27.4% net income margin, implying a 102.5% total return. That requires IAM to hit enterprise scale faster than the current consensus. The downside case still reaches $59.99 at a 4.7% CAGR, a positive return from today’s price, because the buyback program provides a meaningful floor under the valuation. The forecast period ends 12/31/30.

Conclusion: Watch IAM as a percentage of total ARR at the Q1 fiscal 2027 earnings report on June 4, 2026. Management has guided approximately 18% by the fiscal year-end. If Q1 shows meaningful sequential progress toward that figure, the double-digit growth timeline becomes something investors can model with conviction. If IAM stalls, the “accelerating business” language starts to look premature.

DocuSign is a high-margin, cash-generating business trading near multi-year valuation lows with an aggressive buyback program and an AI platform showing early retention advantages. The unresolved question is whether 8% revenue growth is the ceiling or the floor.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in DocuSign?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DocuSign, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DocuSign alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze DocuSign on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!