Key Stats for Enphase Stock

- Past-Week Performance: %

- 52-Week Range: $25.8 to $63.7

- Current Price: $37.8

What Happened?

Enphase Energy (ENPH), a maker of microinverters that convert rooftop solar power into usable electricity, delivered a Q4 non-GAAP EPS of $0.71 against an IBES estimate of $0.58, yet shares trade at $37.84, nearly 41% below their 52-week high of $63.70, as investors weigh a structurally challenged 2026 demand environment against a product cycle that is only now beginning to reload.

On February 3, CEO Badri Kothandaraman reported Q4 revenue of $343.3 million alongside Q1 2026 guidance of $270 million to $300 million, a range management explicitly identified as the demand trough, while simultaneously disclosing a 6% workforce reduction of 160 jobs tied directly to the expiration of the Section 25D residential solar tax credit, the 30% federal incentive for homeowners that expired at end of 2025 under Trump’s tax overhaul.

The sharpest operational proof point sits in the Q4 sell-through figure: U.S. product sell-through surged 21% quarter over quarter to its highest level in more than two years, with battery sell-through specifically up 27%, suggesting genuine end-market demand recovery even as channel inventory normalized following the $70.9 million in safe harbor shipments that had artificially inflated Q3 revenue.

Kothandaraman stated on the Q4 2025 earnings call that “the strong demand trends that we saw at the beginning of Q4 continued till the end of the year, driven by increased solar and battery installations ahead of the expiring Section 25D tax credit,” directly corroborating the channel clean-out and setting the stage for a leaner, more sustainable demand baseline entering 2026.

Enphase’s competitive repositioning across five concurrent product initiatives, including the IQ9 GaN-based commercial microinverter addressing a new $400 million addressable market, a fifth-generation battery targeting 40% lower cost and 50% higher energy density with pilots in Q3 2026, and a $2 billion battery retrofit opportunity across 475,000 installed systems in the Netherlands, gives the company multiple independent revenue levers to drive recovery well beyond its current $37.84 price.

Wall Street’s Take on ENPH Stock

The Q4 demand trough confirmation, paired with a 6% workforce reduction that drops quarterly non-GAAP operating expenses to $70 million to $75 million from Q3 2026 onward, directly improves the earnings recovery trajectory the market has been discounting since October 2025.

Enphase posted FY 2025 normalized EPS of $2.96, and as TIKR estimates, that figure compresses further to $2.19 in 2026 before rebounding to $2.69 in 2027 and $3.13 in 2028, a trajectory grounded in the Q4 sell-through surge of 21% quarter over quarter and the OpEx reset now locked into guidance.

Wall Street’s current stance reflects a market in transition: 9 buys, 3 outperforms, 17 holds, and 1 sell across 29 analysts, with a mean price target of $46.13 implying 21.9% upside from $37.84, a consensus that has compressed alongside the stock but still leans constructive on the product cycle reset.

The spread between the analyst low target of $27.00 and the high of $85.00 reflects exactly the binary embedded in this story: the low anchors to prolonged 25D demand destruction and tariff margin pressure, while the high prices in full execution on the fifth-generation battery cost reset and IQ9 commercial ramp.

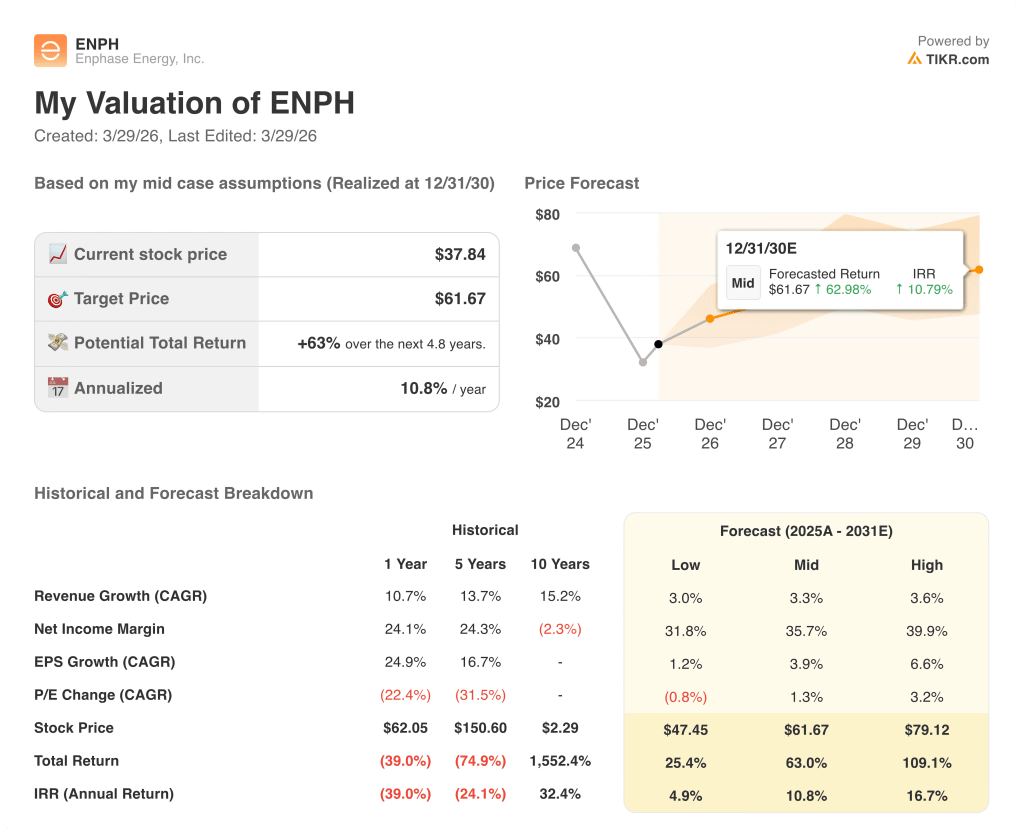

What Does the Valuation Model Say?

The TIKR mid-case model targets $61.67 by December 2030, implying a 63% total return at a 10.8% IRR, driven by a net income margin expansion from 24.3% historically to 35.7% in the mid case, a trajectory the fifth-generation battery’s 40% cost reduction and the $70 million to $75 million quarterly OpEx floor directly support.

The market is pricing ENPH as a structurally impaired solar play, yet FY 2025 FCF of $0.10 billion is set to recover to $0.39 billion in 2026, as TIKR estimates, a 311% surge the current $37.84 price does not reflect.

That FCF recovery is not a model assumption; it is an operational consequence of a lean channel, confirmed Q4 sell-through of 21% quarter over quarter, and a cost structure already reduced by the February headcount cut.

CEO Kothandaraman’s acquisition of common shares in February, disclosed via SEC EDGAR, signals that management views the current price as disconnected from the underlying earnings recovery already visible in Q4 operating metrics.

Sustained reciprocal tariff pressure at 5% of gross margin, combined with a slower-than-expected prepaid lease pilot rollout, would directly erode the margin expansion assumption underpinning the TIKR $61.67 mid-case target.

The Q2 2026 earnings report is the first confirmation point: a sequential revenue increase above the $285 million Q1 midpoint, alongside non-GAAP gross margin expansion toward the 42% to 45% guided range, would validate that the demand recovery Kothandaraman explicitly called is tracking on schedule.

Should You Invest in Enphase Energy, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ENPH stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Enphase Energy, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ENPH stock on TIKR for Free →