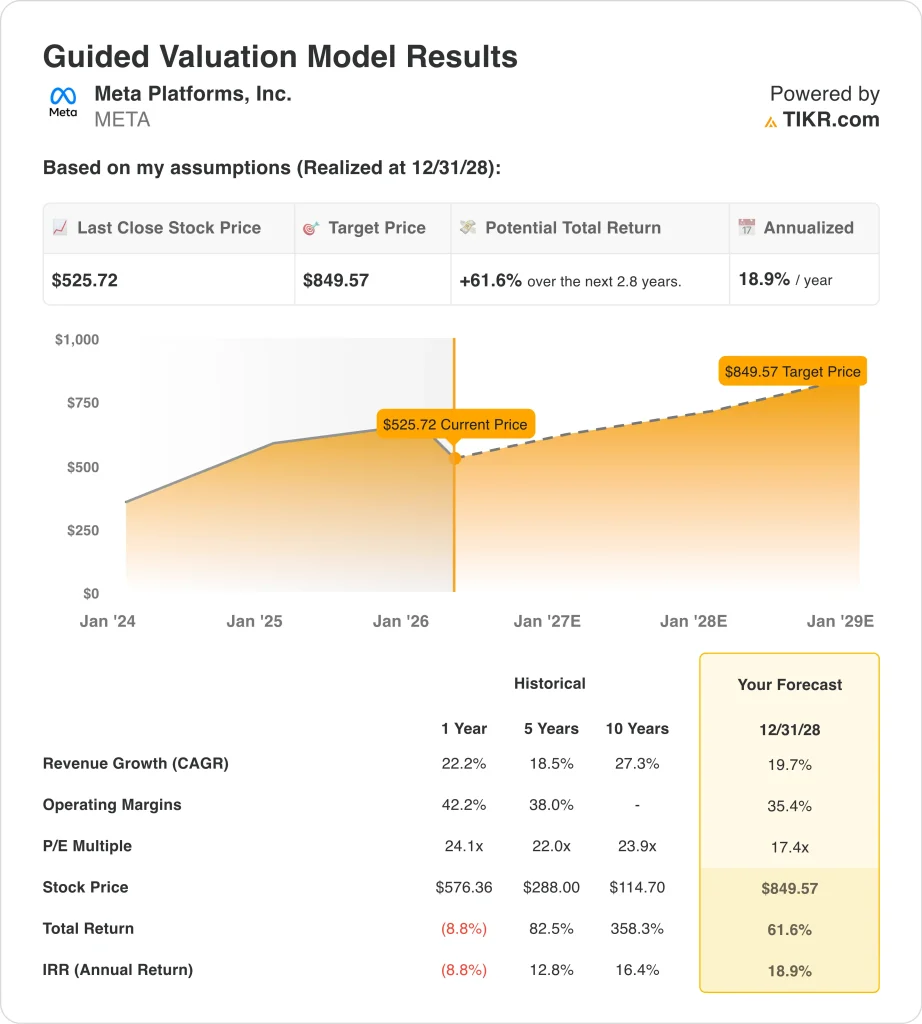

Key Stats for META Stock

- Past week’s performance: -13%

- 52-week range: $480 to $796

- Valuation model target price: $850

- Implied upside: 61.6% over 2.8 years

Value your favorite stocks like META with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Meta Platforms, Inc. (META) stock fell sharply this week as investors reacted to a more complicated story than just advertising growth. On March 27, Reuters reported that Meta was boosting its investment in an AI data center in West Texas to $10 billion from an initial $1.5 billion. That announcement reinforced how aggressively Meta is spending to build AI infrastructure, and it arrived as the broader market was already growing more cautious on megacap AI capex.

At the same time, legal risk moved closer to the center of the story. New Mexico court ordered Meta to pay $375 million in a lawsuit over child exploitation and user safety claims, and a separate Los Angeles jury found Meta and Google liable for contributing to a young woman’s mental health harms through addictive social media design. Those rulings matter because they raise the possibility of more litigation and more scrutiny around how Meta’s platforms are designed.

Meta also faced new operational and restructuring headlines. Reuters reported that the company was laying off hundreds of employees across teams as it tried to contain costs while still pouring money into AI, and it also reported that Meta had delayed the rollout of a new AI model after performance concerns.

There were still positive developments in the mix. Meta plans to debut two new Ray-Ban smart glasses models next week for prescription wearers, which shows the company is still pushing into AI hardware beyond its core apps business. But this week’s price action suggests investors focused more on legal overhangs and spending intensity than on near-term product momentum.

See analysts’ growth forecasts and price targets for META (It’s free) >>>

Is META Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 19.7%

- Operating Margins: 35.4%

- Exit P/E Multiple: 17.4x

Based on these inputs, the model estimates a target price of $849.57, implying 61.6% total upside from the current share price and a 18.9% annualized return over the next 2.8 years.

Meta does not look expensive relative to its own earnings power, even after years of strong performance. The stock trades at about 22.4x LTM earnings, while the valuation model assumes a 17.4x exit P/E, which suggests the model is not relying on a richer multiple to justify a higher value. That matters because Meta is already generating very large profits and cash flow at scale.

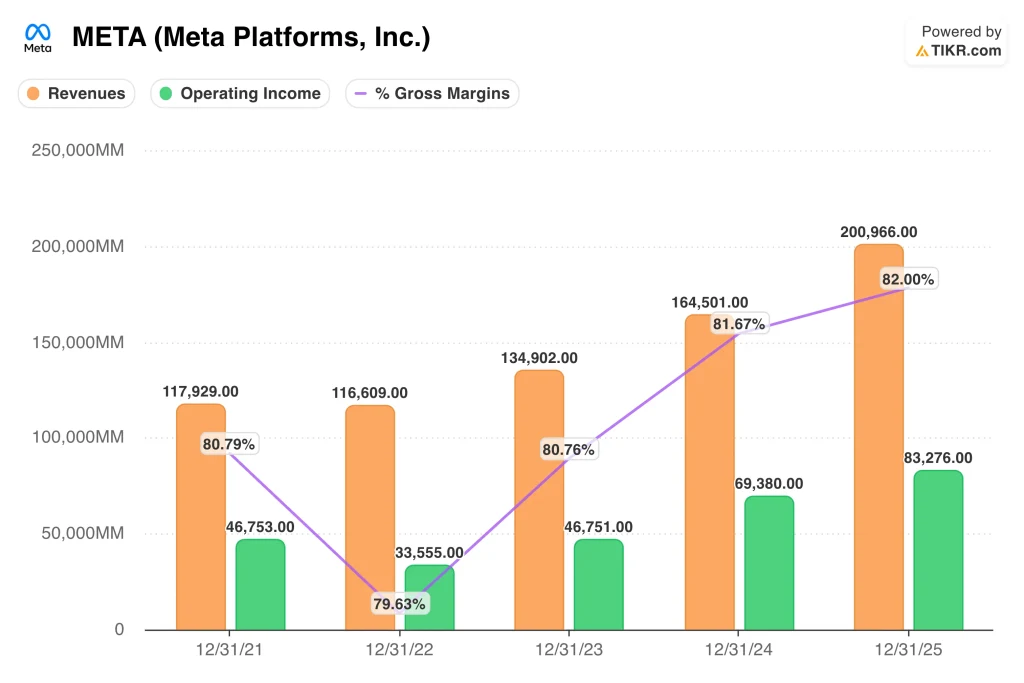

The business fundamentals remain strong. Revenue rose 22.2% to $201.0 billion in 2025, operating income reached $83.3 billion, and gross margin expanded to 82.0%. Those numbers show that Meta’s Family of Apps business is still monetizing engagement efficiently, even as the company keeps investing in AI, infrastructure, and Reality Labs.

Cash generation is also a major part of the valuation story. Meta produced $115.8 billion in operating cash flow and $46.1 billion in free cash flow in 2025, while still repurchasing $44.6 billion of stock and paying dividends. That financial strength gives Meta unusual flexibility to fund data centers, chips, acquisitions, and product launches without stressing the balance sheet.

The debate is less about whether Meta is profitable and more about how much spending is still ahead. Reuters reported that Meta’s 2026 expense outlook is $162 billion to $169 billion, largely because of AI infrastructure and compensation. So the stock’s valuation now depends on whether those higher costs keep translating into better ad performance, stronger AI products, and durable user engagement.

What’s Driving the META Stock Going Forward?

The next big catalyst is Meta’s Q1 2026 earnings report, expected on April 22. Investors will focus on whether ad revenue keeps compounding at a strong pace and whether management still sounds confident about monetizing AI across Facebook, Instagram, WhatsApp, and emerging devices. They will also want updates on expense discipline because capex and infrastructure spending are clearly rising faster than before.

AI remains the main growth driver and the main spending driver. In its January results, Meta guided for first-quarter 2026 revenue of $53.5 billion to $56.5 billion and said full-year 2026 expenses would rise because of cloud spend, depreciation, and infrastructure operating costs. That tells investors Meta is still betting that stronger recommendation systems, better ad tools, and new AI products will justify much heavier investment.

Finally, regulation and litigation could stay front and center. Reuters reported both the New Mexico judgment and the Los Angeles verdict, and it also noted that Indonesia is rolling out social media restrictions for users under 16. So even if Meta keeps growing revenue and cash flow, the stock may remain sensitive to legal headlines that challenge platform design, youth safety practices, and global access rules.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Meta Platforms, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up META, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track META alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Meta Platforms stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!