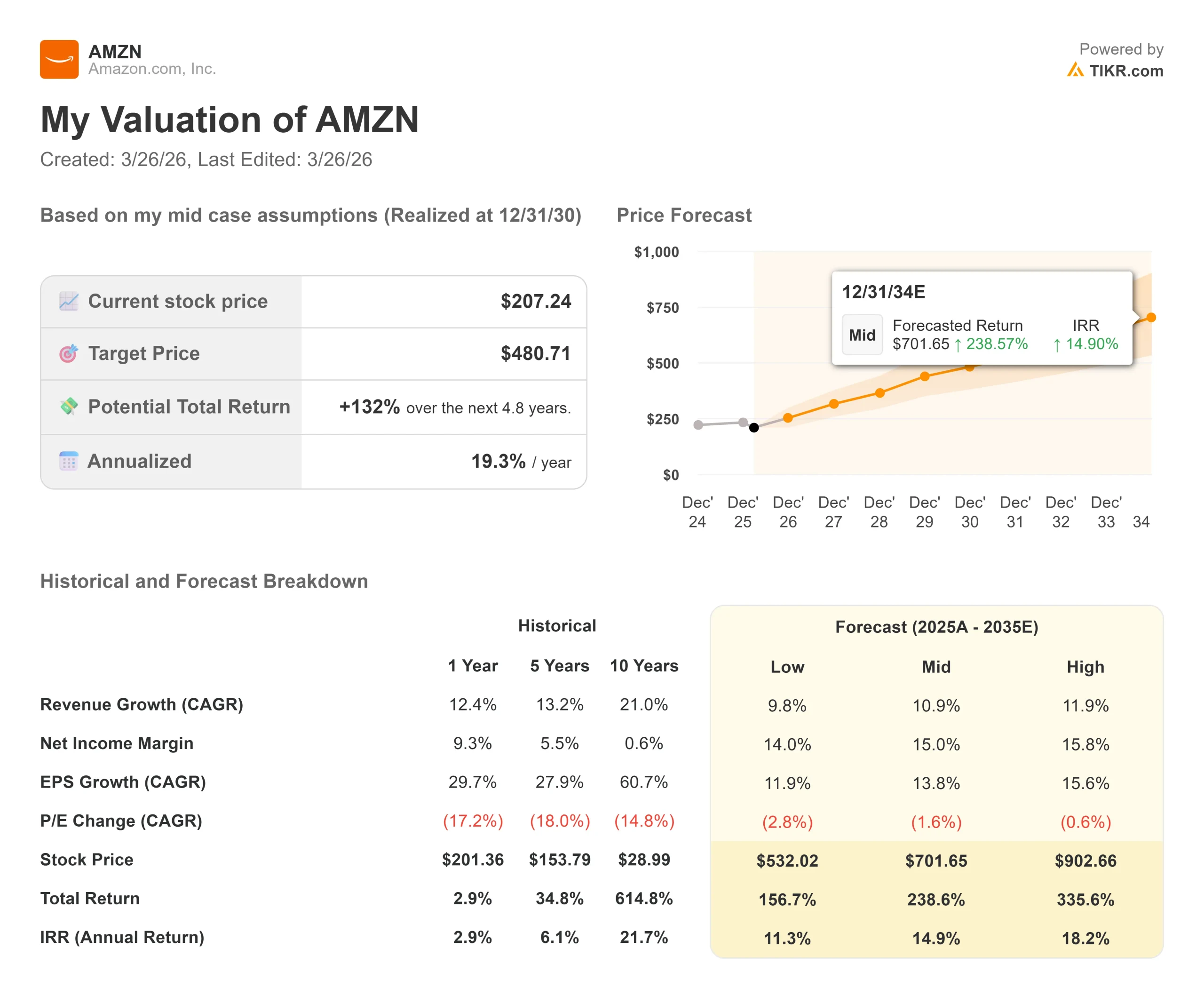

Key Stats for Amazon Stock

- Current Price: $207.24

- Target Price (Mid): $480.71

- Street Target: $280.47

- Potential Total Return: +132% over the next 4.8 years

- Annualized IRR: 19.30% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Amazon (AMZN) stock has rarely divided investors this sharply.

Bulls see a structurally advantaged business trading near its cheapest forward multiple in years. Bears see a company pouring cash into data centers while free cash flow collapses.

The unresolved question: will Amazon’s $200 billion AI infrastructure commitment in 2026 generate the returns CEO Andy Jassy is promising, or is the market right to demand proof first?

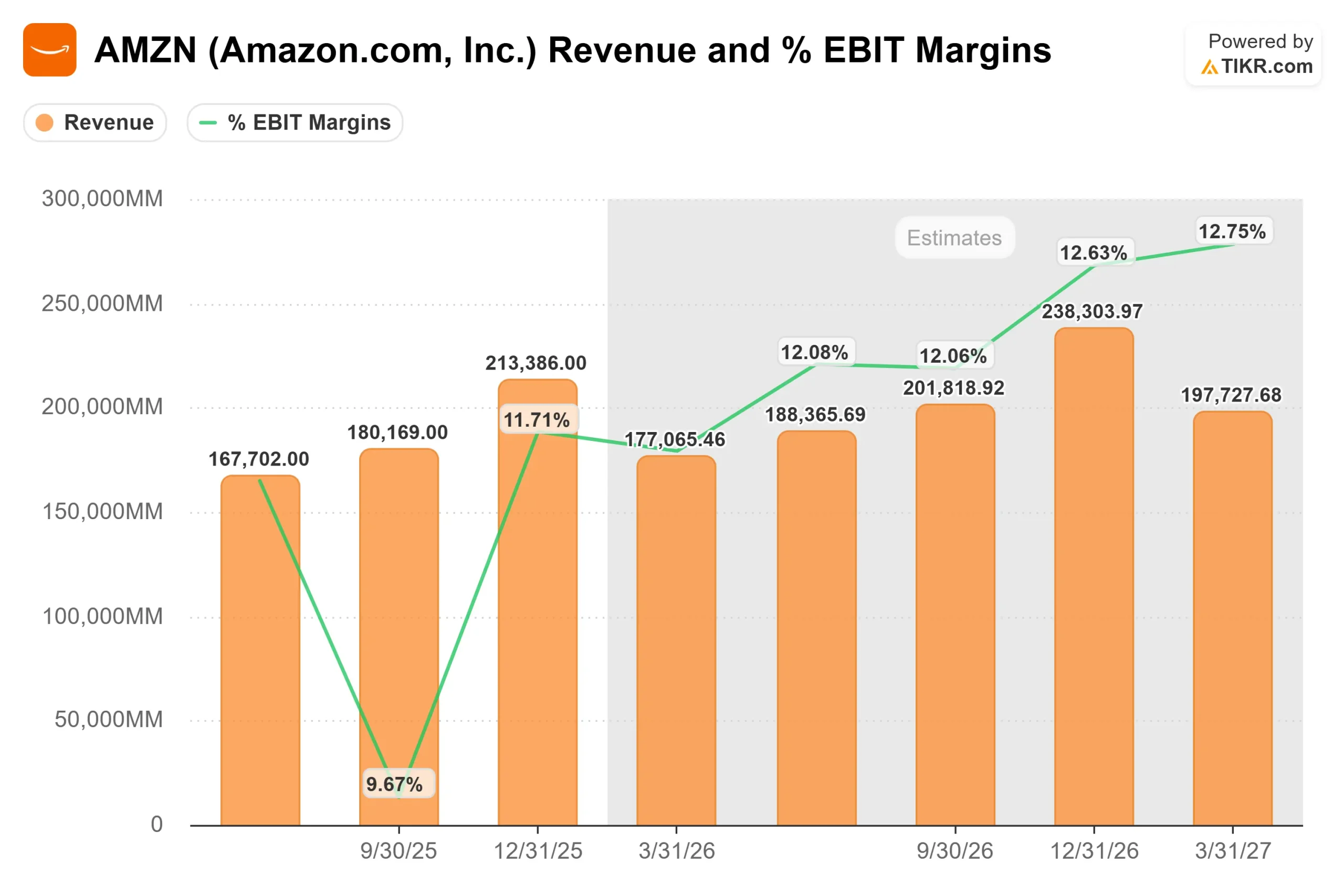

The selloff began with the Q4 2025 earnings report on February 5, 2026.

Amazon beat revenue expectations, posting $213.4 billion for the quarter, and delivered adjusted EPS of $1.95. But management guided for approximately $200 billion in 2026 capital expenditures (spending on data centers, chips, and AI infrastructure), far exceeding Wall Street’s prior estimates.

The stock fell 5.55% on the day and hit a max drawdown of 21.74% by February 13, 2026. It has not fully recovered since, closing near $199 on March 27 as macro pressure and renewed capex skepticism weighed on shares.

Jassy addressed the return-on-capital question directly on the call. “We have very high demand, customers really want AWS for core and AI workloads, and we’re monetizing capacity as fast as we can install it,” he said.

“We have deep experience understanding demand signals in the AWS business, and then turning that capacity into strong return on invested capital. We’re confident this will be the case here as well.” CFO Brian Olsavsky added that AWS operating margins reached 35% in Q4, up 40 basis points year over year, even as AI depreciation created a visible headwind.

The underlying results were strong. AWS growth re-accelerated to 24% year over year in Q4, its fastest pace in 13 quarters, on an annualized revenue run rate of $142 billion.

North America’s operating margin expanded to 9% from 8% a year earlier.

Advertising revenue grew 22% to $21.3 billion. Full-year operating cash flow rose 20% to $139.5 billion. The market’s issue is not the business. It is the timing of returns on a $200 billion bet.

See historical and forward estimates for Amazon stock (It’s free!) >>>

Is Amazon Undervalued Today?

At $207.24, Amazon trades at 26.84x forward earnings and 10.83x NTM EV/EBITDA (next twelve months enterprise value divided by earnings before interest, taxes, depreciation, and amortization).

The pressure point is free cash flow.

Amazon’s LTM (last twelve months) free cash flow fell to $7.70 billion in 2025, down 76.6% year over year, as capital expenditure surged to $131.8 billion. With 2026 CapEx guided at approximately $200 billion, free cash flow will likely turn negative before recovering as installed capacity generates revenue.

According to Evercore ISI, Amazon is among several large-cap technology companies expected to see year-over-year free cash flow declines in 2026 as AI infrastructure spending accelerates across the sector. That near-term cash drag is real.

What may be underappreciated is the revenue already scaling against that capacity.

The AWS revenue backlog stood at $244 billion as of Q4, up 40% year over year. Jassy described a “barbelled” AI demand landscape, with AI labs consuming massive compute on one end, enterprises running productivity workloads on the other, and the largest long-term opportunity in the middle as enterprise production workloads migrate to AI-native architectures.

That migration is still early, which is why the buildout is happening now.

Amazon’s custom silicon business adds durability to the thesis.

The Trainium and Graviton chip programs (Amazon’s in-house AI and CPU chips) combined now exceed $10 billion in annualized revenue, growing at triple-digit rates year over year.

Trainium2 underpins the majority of Amazon’s Bedrock platform (the service that lets companies access and run AI models at scale), giving Amazon better unit economics than rivals relying solely on third-party GPUs.

Jassy confirmed that nearly all Trainium3 supply is expected to be committed by mid-2026, a supply constraint that reflects demand strength, not weakness.

The retail and advertising businesses are performing better than the stock price implies.

Everyday essentials grew nearly twice as fast as all other categories in the U.S. in 2025, representing one in three units sold.

Advertising grew 22% in Q4, adding more than $12 billion of incremental revenue across all of 2025.

Prime Video’s ad-supported audience reached 315 million viewers globally, up from 200 million in early 2024. Bernstein analyst Nikhil Devnani reiterated an Outperform rating with a $300 price target in January 2026, calling the current setup one of the strongest bull cases since the pandemic, with AWS revenue growth and retail margins both appearing to accelerate.

TIKR Advanced Model Analysis

Key Stats

- Current Price: $207.24

- Target Price (Mid): $480.71

- Potential Total Return: +132%

- Annualized IRR: 19.30% / year

See analysts’ growth forecasts and price targets for Amazon stock (It’s free!) >>>

The TIKR mid-case model targets $480.71 by December 31, 2030, a 132% total return at a 19.30% annualized IRR from $207.24. The two revenue drivers are AWS re-acceleration as AI enterprise workloads scale into production and continued retail monetization through advertising and everyday essentials. The margin driver is net income margin expansion to 15.0% by 2030, up from 10.8% today, as the capex cycle matures and high-margin AWS and advertising revenue grow as a share of the mix. The primary risk is that AI monetization takes longer than expected, extending free cash flow suppression and pressuring the multiple further.

The low case targets $532.02 at 12/31/30, assuming 9.8% revenue CAGR and 14.0% net income margins, representing 156.7% total return at an 11.3% IRR. The high case reaches $902.66, assuming 11.9% revenue CAGR and 15.8% margins. The mid-case reflects the most balanced view of execution risk, and at 19.30% annualized it represents a compelling long-term risk-reward.

Conclusion: Watch AWS revenue growth at the Q1 2026 earnings report, expected in late April. If AWS holds at or above 24% and management signals a free cash flow trough in 2026 ahead of recovery in 2027, the stock has a credible path toward the Street consensus. If growth slips below 20% or CapEx guidance moves higher without corresponding backlog clarity, the pressure will extend.

Amazon’s $200 billion bet is either the right investment at the right time, or the most expensive way to find out it wasn’t. The late April earnings call is where the evidence starts to accumulate.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Amazon?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Amazon, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amazon alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!