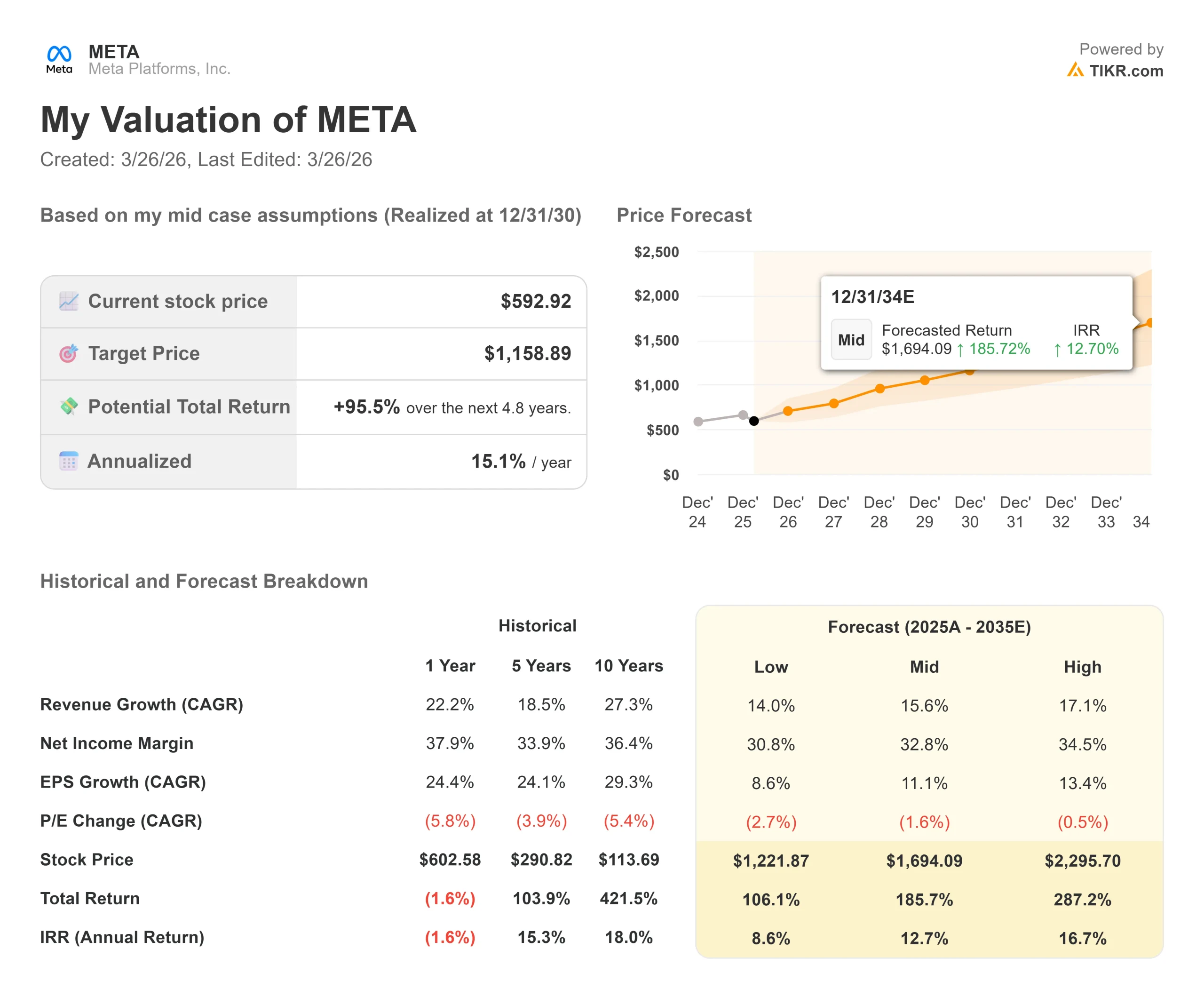

Key Stats for Meta Stock

- Current Price: $592.92

- Target Price (Mid): $1,158.89

- Street Target (Mean): $863.63

- Potential Total Return: +95.5%

- Annualized IRR: 15.10% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

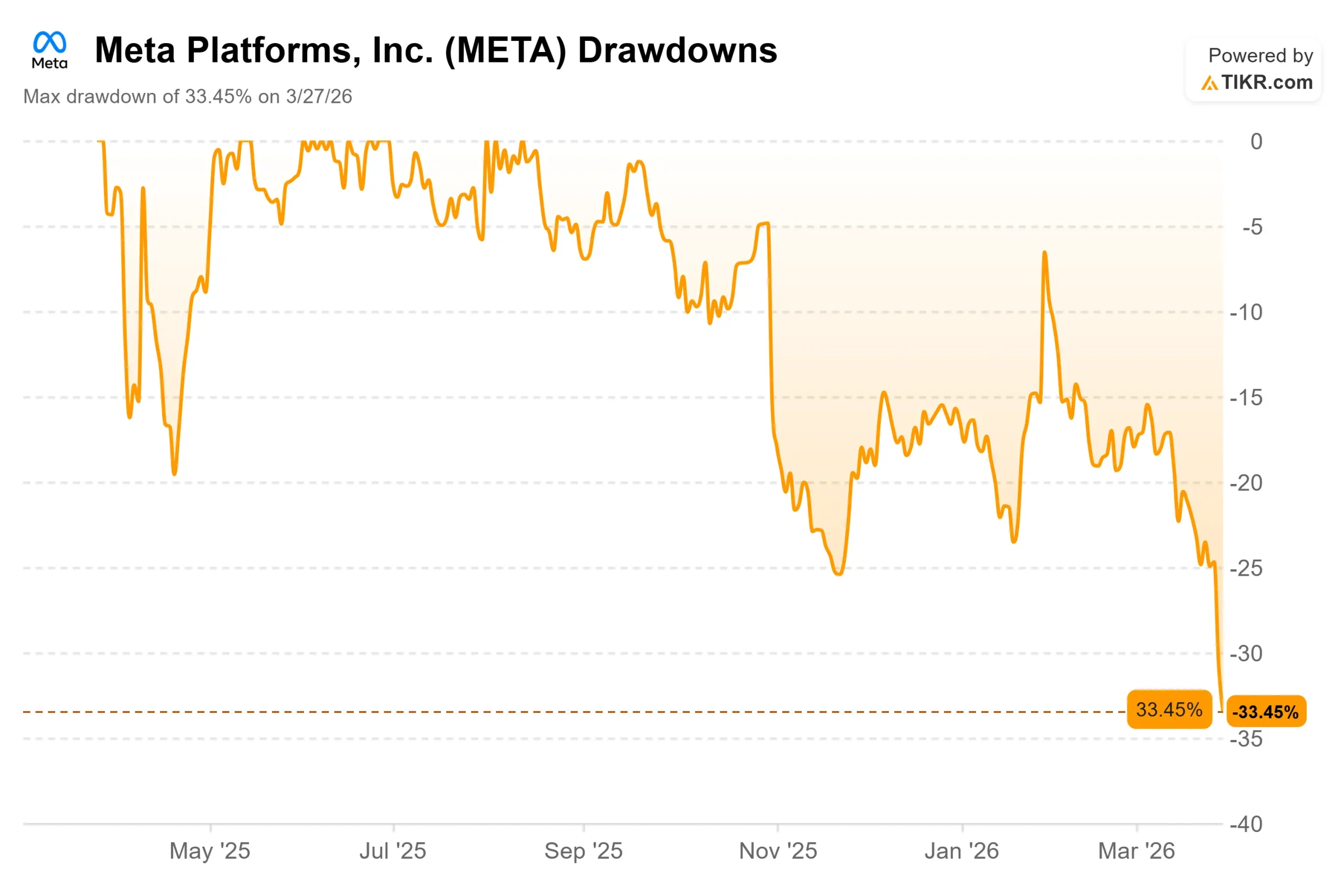

Meta Platforms (META) has fallen roughly 25% from its 52-week high of $796.25, with investors already uneasy about a $115–$135 billion capital expenditure commitment for 2026.

Then two jury verdicts arrived in four days and sent the stock down nearly 8% on March 26.

Bulls say the fines are rounding errors against a business generating more than $83 billion in annual operating income.

Bears say the verdicts open the door to a litigation pipeline that could eventually cost far more. That tension is the question every META investor is sitting with right now.

On March 24, a New Mexico jury ordered Meta to pay $375 million for violating state consumer protection law by enabling child sexual exploitation on its platforms, the first time any U.S. state prevailed at trial against Meta on child safety grounds.

The following day, a Los Angeles jury found Meta and YouTube liable in a social media addiction case.

The L.A. damages attributable to Meta were a few million dollars, but the legal theory mattered far more.

The case centered on platform design rather than specific content, which bypasses Section 230 (the federal law that has long shielded tech companies from liability for third-party content).

New Mexico attorney general Raúl Torrez told CNBC after the verdict that there is “a distinct possibility that these cases motivate Congress to re-examine Section 230.”

If that happens, the liability math changes fundamentally.

A Meta spokesperson said the company “respectfully disagrees with the verdict and will appeal.”

Meta’s CFO, Susan Li, had flagged this risk explicitly on the January 28 Q4 earnings call, noting that various U.S. trials scheduled for 2026 “may ultimately result in a material loss.”

Li also presented at the Morgan Stanley Technology, Media and Telecom Conference on March 4, where the dominant topic was return on invested capital (ROIC, the profit generated relative to capital deployed) from the AI buildout, not litigation.

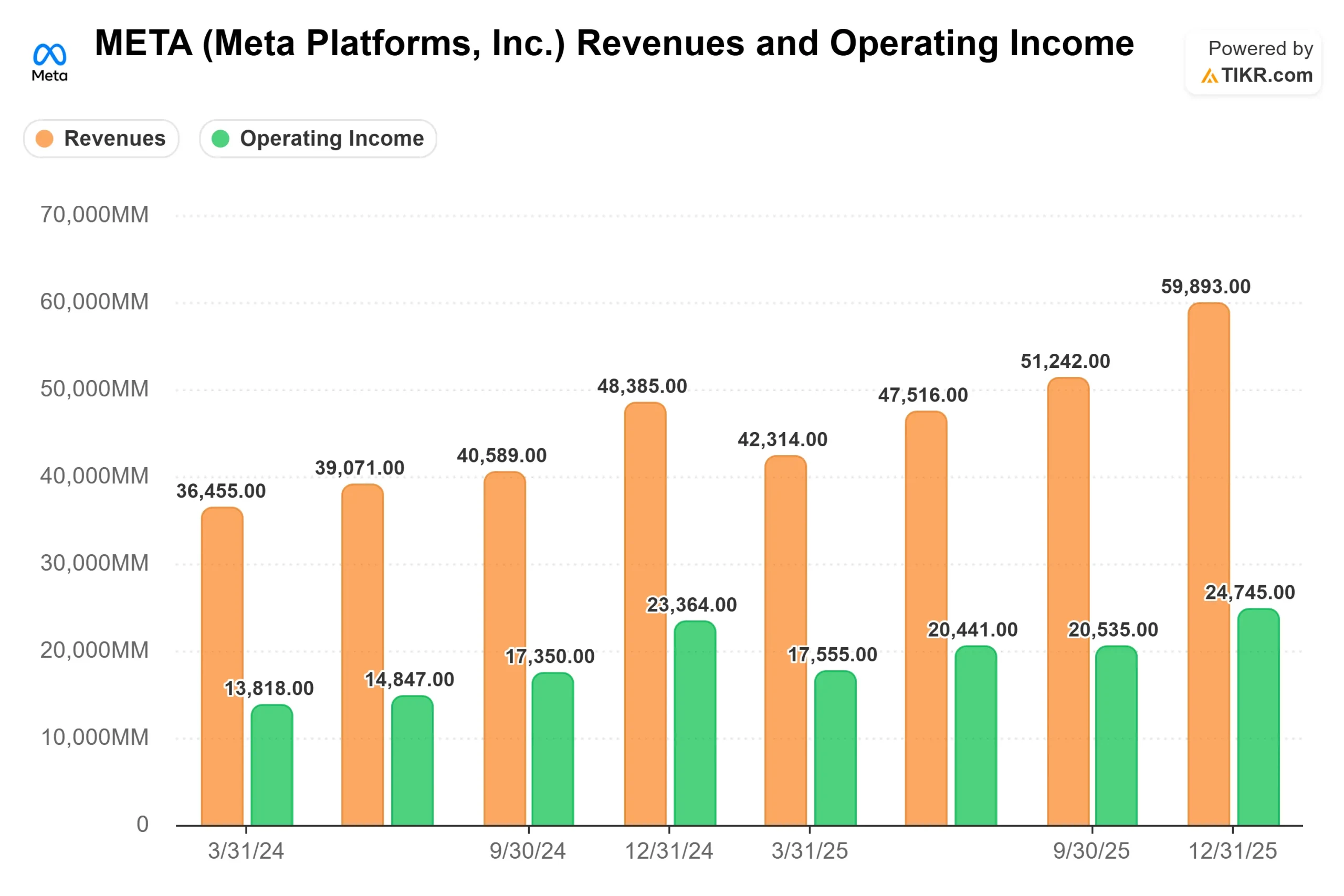

The underlying business is strong. Q4 2025 revenue came in at $59.9 billion, up 24% year over year, ahead of the $58.4 billion consensus.

Since that post-earnings high, the stock has given back most of those gains.

The company that looked like the clearest AI monetization story in Big Tech now trades near the low end of its one-year range, carrying two fresh jury verdicts and one of the largest capex budgets in corporate history.

See historical and forward estimates for Meta stock (It’s free!) >>>

Is Meta Undervalued Today?

The legal calendar is the first thing to understand.

The $375 million New Mexico penalty represents less than two days of Meta’s 2025 operating income.

The L.A. award is measured in millions. Both will be appealed.

The real risk is what comes next: more than 40 state attorneys general have sued Meta over child safety, a major multi-state school district lawsuit is set for trial this summer in Oakland, and another bellwether case involving a teenage boy is scheduled later this year.

The verdicts this week matter because they proved a plaintiff can win, which changes the negotiating dynamics for every case still in the pipeline.

The Street’s mean price target of $863.63, based on 60 price target submissions, implies 45.7% upside from current levels.

Evercore ISI reiterated a Buy rating on March 27, the day after the verdict-driven selloff.

The NTM EV/EBITDA multiple (enterprise value relative to a company’s cash earnings) sits at 10.60x.

For context, Alphabet trades at 15.82x on the same basis, despite facing similar legal exposure in the same California case.

Reddit, which generates a fraction of Meta’s profits, trades at 7.71x NTM revenues against Meta’s 5.99x.

The market is applying both a legal discount and a capex discount to Meta simultaneously, raising the question of whether those fears are being double-counted.

The capex story is the other weight on the multiple.

Meta guided to $115–$135 billion in 2026 capex, nearly double the $69.7 billion in capital expenditures on Meta’s 2025 cash flow statement (the company’s own guidance-basis figure of $72.2 billion includes finance lease payments).

Li made the mechanics of this explicit at the Morgan Stanley conference.

She described a flywheel where ad improvements lower costs for advertisers, which draws in more budget, which funds the next round of improvements.

A single product ranking change in Q4 2025 drove a 7% lift in organic content views on Facebook, which Li called the highest-revenue-impact product launch in the past two years.

A separate compute efficiency optimization drove a 3% conversion lift on Instagram ads.

These are measurable improvements on a platform where Q1 2026 consensus revenue is already sitting at $55.5 billion, up 31% from Q1 2025.

TIKR Advanced Model Analysis

See analysts’ growth forecasts and price targets for Meta stock (It’s free!) >>>

The TIKR mid-case uses a 15.6% revenue CAGR (compound annual growth rate) through December 31, 2030, with a net income margin of 32.8%, up from 30.1% in 2025. Two drivers underpin the revenue assumption. The first is advertising yield: the compounding flywheel Li described at the Morgan Stanley conference. The second is Meta AI’s distribution advantage. Li confirmed that Meta AI already has over 1 billion active users, running on a pre-frontier model. When a frontier model arrives, monetization spans WhatsApp, Instagram, Facebook, and Messenger simultaneously, reaching billions of users with no need to build a new distribution network.

The margin driver is operating leverage. SG&A expenses (selling, general, and administrative costs) fell from 20.2% of revenue in 2021 to 12.0% in 2025. Li noted at the Morgan Stanley conference that AI tools have boosted developer coding productivity by roughly 80% for the most effective users, which means Meta may scale output without proportionally scaling headcount.

The primary risk is capex payback timing. Suppose the $125 billion midpoint of 2026 spending does not show up in measurable engagement or monetization gains by late 2026, the multiple compresses further. Even the TIKR low-case target of $1,221.87 implies a 106.1% total return from today’s price, which shows how much earnings power is already embedded in the base business before any new AI product monetization is counted. The downside scenario carries an 8.6% annualized IRR, assuming the AI spending underdelivers, and legal costs are real but manageable. That is not catastrophic for a company that generated $115.8 billion in operating cash flow in 2025.

Conclusion: The metric to watch at the Q1 2026 earnings report, expected April 29, is average revenue per user in the U.S. and Canada. If that figure keeps rising alongside ad impression volume, the AI-driven ad engine is compounding through the legal and capex noise. A deceleration there, paired with any upward revision to legal reserve estimates, is where the bear case gets credible. At 19.61x NTM earnings, with the Street’s mean target 45.7% above the current price and zero Sell ratings among 69 covering analysts, the market has priced in real risk, but not collapse.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Meta?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Meta, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Meta alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!