Key Stats for LULU Stock

- Past-Week Performance: -10%

- 52-Week Range: $144 to $340

- Valuation Model Target Price: $176

- Implied Upside: 20.8%

Analyze your favorite stocks like American Electric Power with TIKR (It’s free) >>>

What Happened?

Lululemon stock is down about 10% this week, trading near $146 per share as investors question whether the company can sustain premium pricing and high margins while North America remains under pressure.

The broader market narrative has shifted from Lululemon’s long track record of premium growth toward a tougher debate around slower U.S. demand, markdown risk, and margin pressure.

The stock is down this week primarily because the company’s 2026 outlook pointed to weaker profitability and soft near-term growth, while analysts also cut price targets.

Barclays reduced its target to $161 from $203 and rated the stock equal weight, UBS lowered its target to $176 from $189 and maintained a neutral rating, Robert W. Baird cut its target to $190 from $210 while keeping a neutral stance, and BTIG trimmed its target to $225 from $250 despite maintaining a buy rating. Those revisions reinforced concerns that Wall Street is resetting expectations lower as growth and margins normalize.

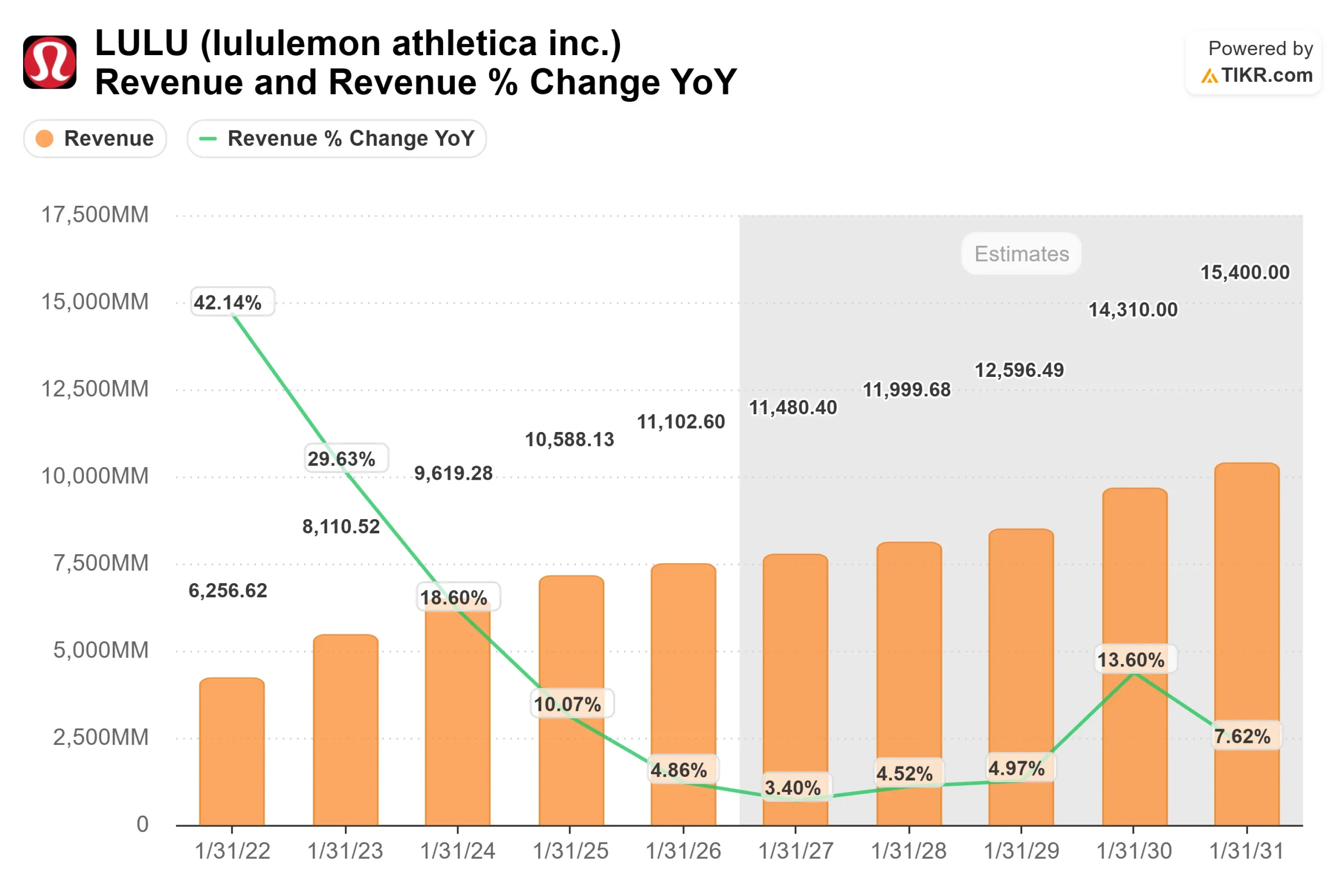

Lululemon reported fourth quarter revenue of $3.6 billion, with comparable sales up 2%, but gross margin fell 550 basis points to 54.9% as tariffs and higher markdowns weighed on results.

Management guided for 2026 revenue of $11.35 billion to $11.5 billion, or 2% to 4% growth, while diluted EPS is expected to fall to $12.10 to $12.30 from $13.26 in 2025.

North America is expected to decline 1% to 3%, though the company said it is already seeing better full-price selling in Q1, and Meghan Frank noted the business is focused on “restoring the full-price health of our brand.”

Competition has also become a bigger part of the story, with direct peers like Nike and Adidas putting more pressure on the category through promotions and stronger product cycles.

That matters because Lululemon’s historical outperformance has been driven by full-price selling and premium margins, so any shift toward heavier discounting could weigh on profitability.

Institutional activity reflected mixed conviction, with AllianceBernstein cutting its stake by 62.4% to about 1,367,638 shares worth $243.3 million, while Assenagon Asset Management increased its position by 255.6% to 438,461 shares worth about $91.1 million.

Insider activity added some support, with Director Charles Bergh purchasing 6,090 shares at an average price of $164 for about $1.0 million.

Value lululemon athletica instantly (Free with TIKR) >>>

Is LULU Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 4.3%

- Operating Margins: 17.4%

- Exit P/E Multiple: 11.8x

Revenue growth has slowed from earlier 20%+ expansion into a more mature mid-single-digit range, reflecting a shift from rapid store expansion toward more normalized demand trends.

See analysts’ growth forecasts and price targets for lululemon athletica (It’s free) >>>

Future growth is increasingly tied to international markets, particularly China, where revenue rose 28% in the fourth quarter and the store runway remains much longer than in North America.

Growth also depends on newer categories like men’s apparel and footwear, which are still smaller than the core women’s business but can expand Lululemon’s addressable market over time.

Margin performance remains the key swing factor, as the company is trying to reduce markdowns, improve inventory discipline, and return North America to healthier full-price selling.

That matters more now because 2026 will still absorb tariff pressure, fixed-cost deleverage, and brand investment even as management tries to course-correct the U.S. business.

Execution across product newness, inventory management, and international expansion will drive results over the next year.

Management is increasing new style penetration to about 35% in North America, rolling out updated store presentations, and trying to shorten product timelines to better react to demand.

At current levels, Lululemon appears modestly undervalued, with future performance driven by improving full-price sell-through, stronger product cycles, and continued international growth rather than a return to its earlier hyper-growth phase.

How Much Upside Does LULU Stock Have From Here?

Investors can estimate lululemon athletica’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value lululemon athletica in under 60 seconds with TIKR (It’s free) >>>