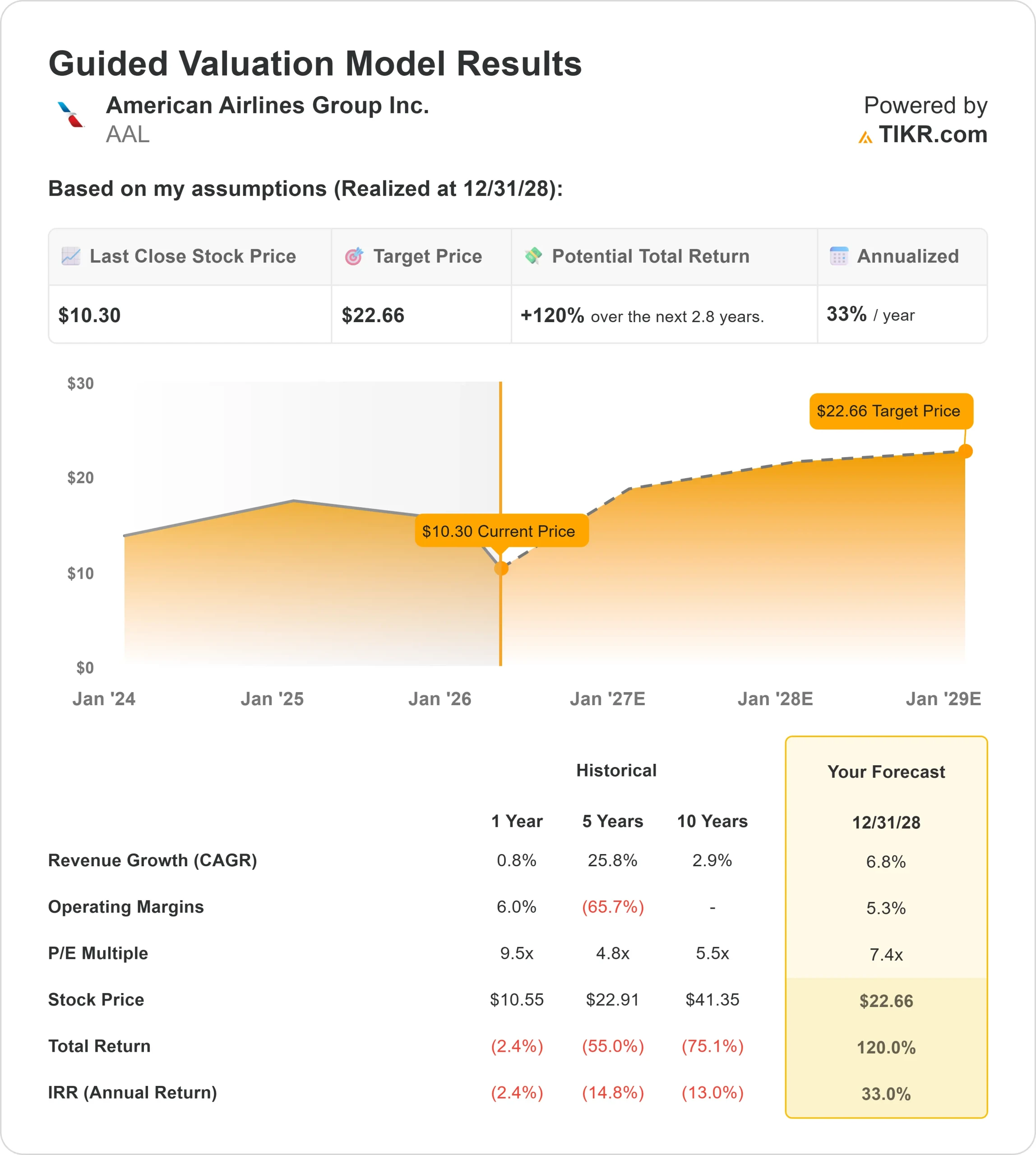

Key Stats for AAL Stock

- Past-30-Day Performance: -21%

- 52-Week Range: $9 to $17

- Valuation Model Target Price: $23

- Implied Upside: 120%

Analyze your favorite stocks like American Airlines Group with TIKR (It’s free) >>>

What Happened?

American Airlines Group Inc. stock has come under pressure recently as investors shift focus from strong travel demand toward whether that demand can translate into consistent profitability, with the company underperforming peers like Delta Air Lines and United Airlines, which have generally maintained higher margins through stronger premium pricing and better earnings execution.

American Airlines Group Inc. stock fell about 21% over the past 30 days, finishing near $10 per share, primarily because rising fuel costs and analyst price target cuts have increased concerns that near-term earnings will come under pressure despite strong demand.

Management indicated fuel has increased expenses by about $400 million in the first quarter alone, while UBS cut its price target from $21 to $15 and Wells Fargo lowered its target from $17 to $12, signaling reduced confidence in margin recovery.

Compared to Delta and United, which generate stronger profitability from premium cabins and loyalty programs, American remains more exposed to cost volatility because its margins are thinner, which has weighed on sentiment.

This month, at the JPMorgan Industrials Conference, American Airlines raised its first quarter revenue outlook to more than 10% growth, which CEO Robert Isom said would represent a company record year over year and roughly $1.3 billion of additional revenue, as strong premium and main cabin demand drove March unit revenue above 10% with strength expected to continue into April and May.

Isom said 8 of American’s top 10 booking days and 8 of its top 10 revenue weeks occurred this quarter, while rapidly rising fuel costs added about $400 million in expenses, noting, “Demand for our product is strong,” as the company still expects to finish within its prior guide.

Recent filings show mixed institutional positioning. Aquatic Capital Management increased its stake by 22.9% to about 969,899 shares worth roughly $10.9 million, while Entropy Technologies boosted its position by 874.7% to 669,600 shares valued at about $7.53 million.

At the same time, Brevan Howard Capital Management reduced its stake by 71%, and Quantbot Technologies trimmed its position by 60.7%, even as overall institutional ownership remains around 52%.

This divergence suggests that while some investors are positioning for a recovery, others remain cautious given ongoing uncertainty around margins and the company’s still-elevated debt load.

Value American Airlines Group instantly (Free with TIKR) >>>

Is AAL Undervalued?

Under valuation assumptions, the stock is modeled using:

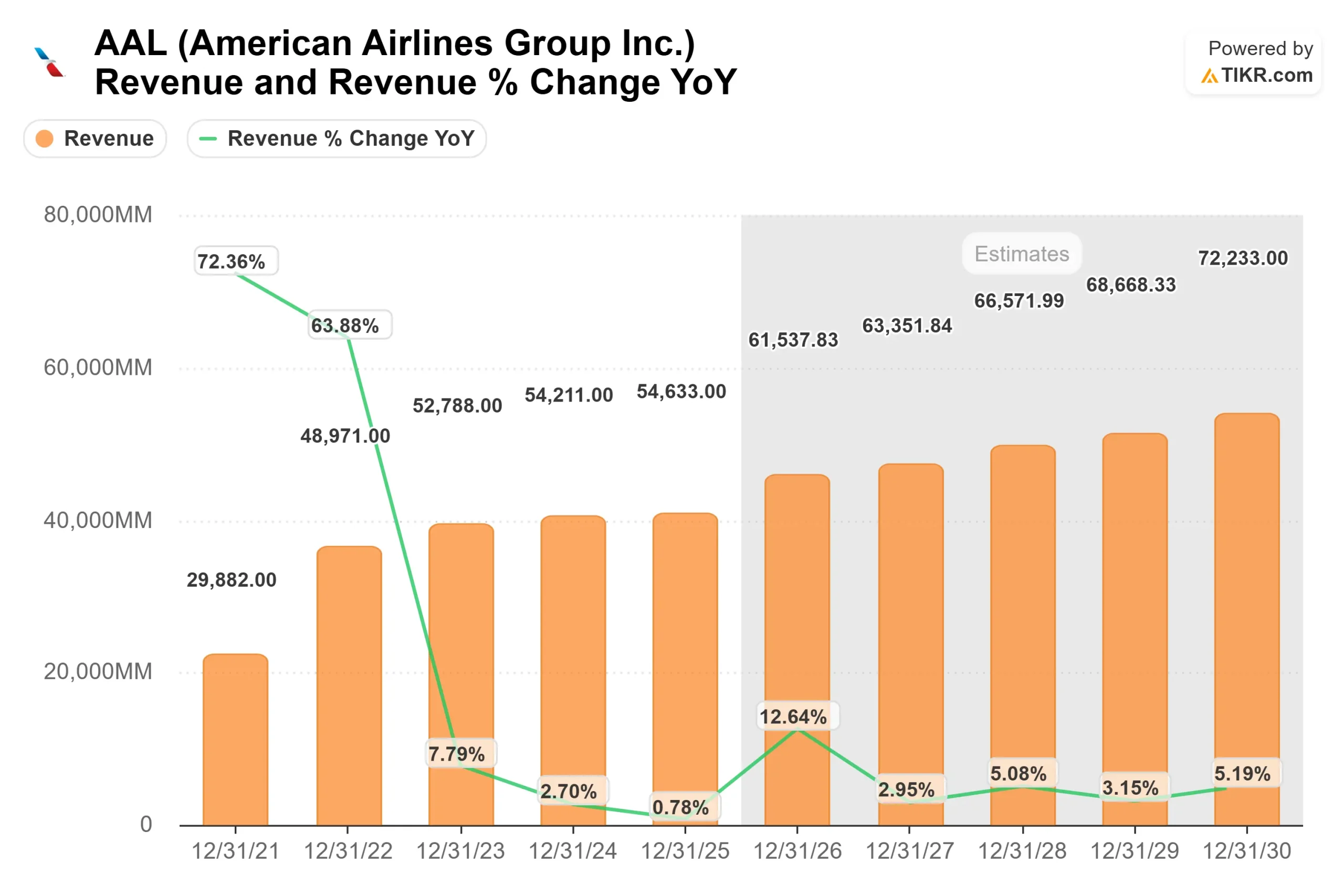

- Revenue Growth (CAGR): 6.8%

- Operating Margins: 5.3%

- Exit P/E Multiple: 7.4x

Growth is expected to remain steady, supported by resilient travel demand and continued strength across both premium and main cabin segments.

The more important driver is margin expansion, where improved pricing in premium cabins, higher ancillary revenue from seat upgrades and baggage, and continued growth in the AAdvantage loyalty program can lift profitability without requiring significant increases in passenger volume.

See analysts’ growth forecasts and price targets for American Airlines Group (It’s free) >>>

American’s loyalty program is particularly important because it generates high-margin, recurring revenue through credit card partnerships, providing a more stable earnings base compared to ticket sales.

This dynamic matters because the company currently operates with lower margins than peers, meaning even modest improvements in pricing, cost efficiency, or revenue mix can have an outsized impact on earnings.

Balance sheet improvement also remains a key lever, as reducing the company’s still-elevated debt load can lower interest expense and support equity value as free cash flow improves.

Based on these inputs, the model estimates a target price of about $23, implying roughly 120% total upside over the next 2.8 years, suggesting the stock appears undervalued, with future performance driven by margin recovery, loyalty revenue growth, and balance sheet improvement.

How Much Upside Does AAL Stock Have From Here?

Investors can estimate American Airlines Group’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value American Airlines Group in under 60 seconds with TIKR (It’s free) >>>