Key Takeaways:

- Capgemini SE is a global leader in consulting, technology, and engineering services that helps enterprises modernize IT, accelerate digital transformation, and deploy AI and cloud at scale while serving clients across Europe, North America, and fast‑growing Asia‑Pacific markets.

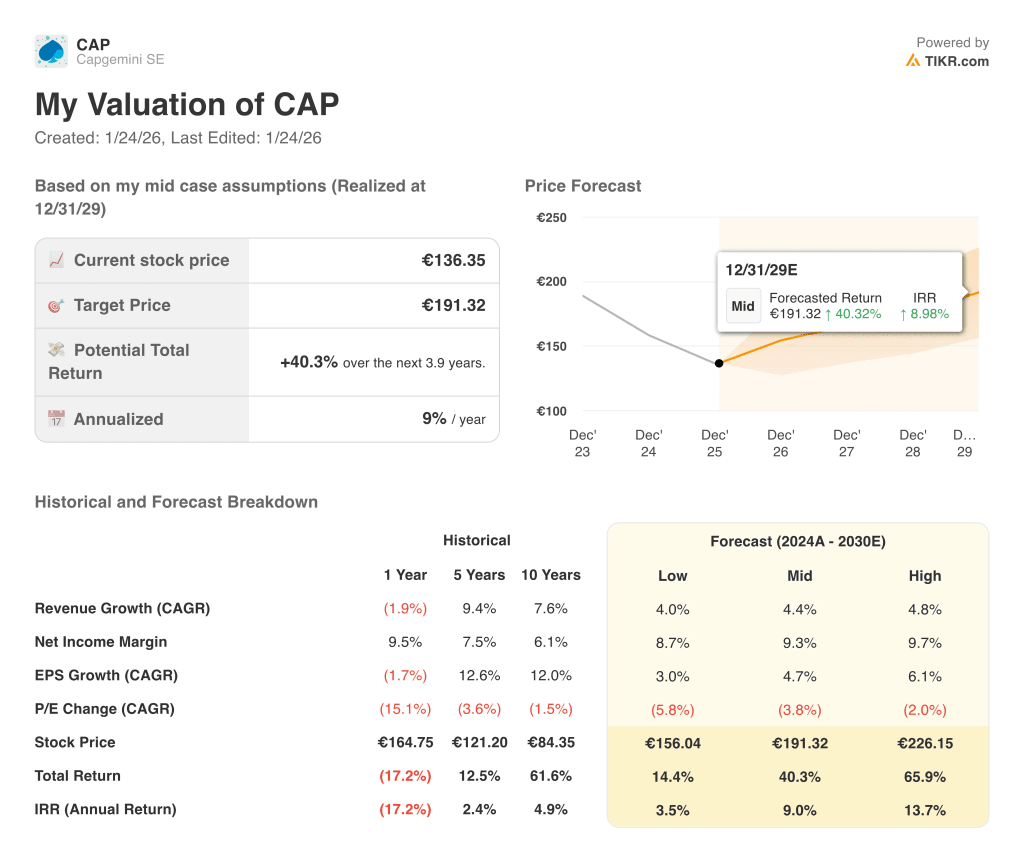

- CAP stock could reasonably reach €191 per share by December 2029, based on our valuation assumptions.

- This implies a total return of 40.3% from today’s price of €136, with an annualized return of 9.0% over the next 3.9 years.

Capgemini SE (CAP) is deepening its role as a strategic digital transformation partner by combining consulting, cloud, and engineering capabilities to support large enterprises as they modernize legacy systems and deploy data‑driven solutions across their operations.

The company leverages its global delivery network and domain expertise to design, build, and manage complex IT and business process platforms, so clients can scale AI, analytics, and automation more efficiently while improving resilience and customer experience.

Capgemini’s diversified industry footprint across financial services, public sector, manufacturing, consumer, and telecom clients helps smooth cyclical swings, and its long‑term contracts and managed services provide recurring revenue and visibility into future demand.

Management continues to focus on high‑value segments like cloud, data, and AI, and it is aligning its portfolio toward higher‑margin, innovation‑led work while maintaining cost discipline across its global delivery model.

Here’s why Capgemini stock could provide solid returns through 2029 as it executes on digital and cloud transformation demand while using disciplined capital allocation and maintaining attractive profitability.

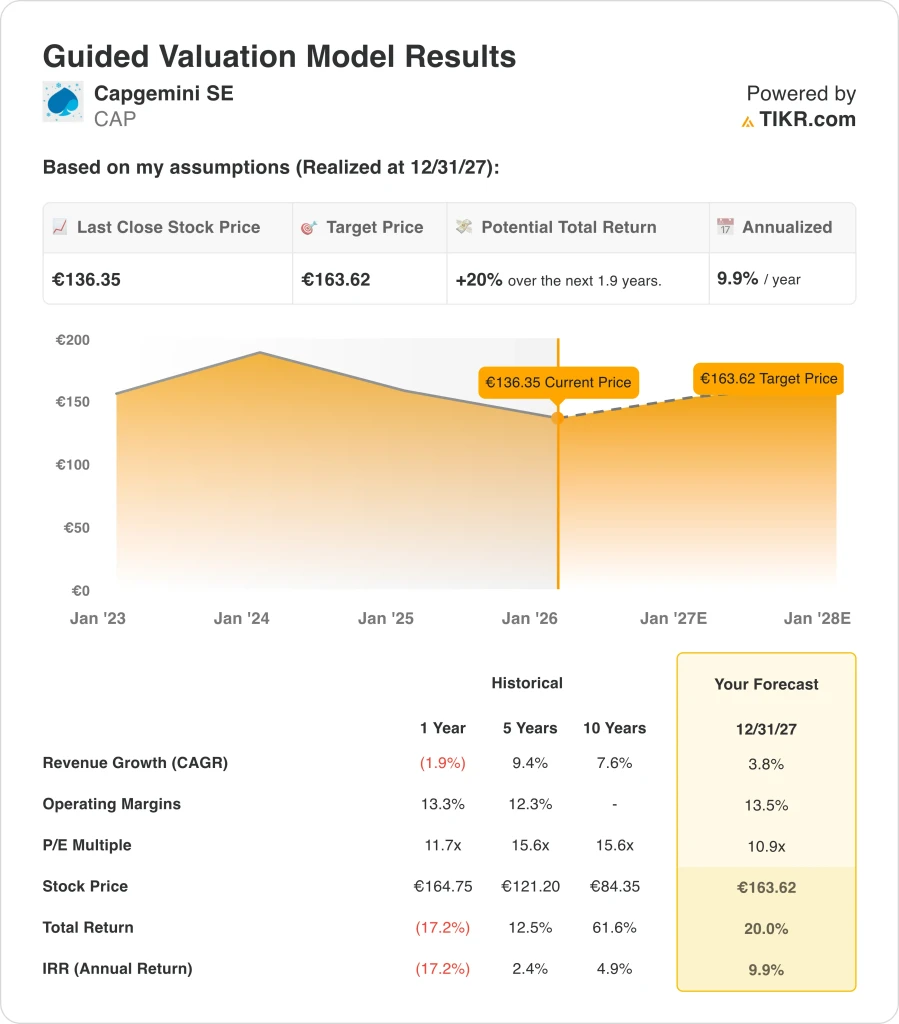

What the Model Says for Capgemini Stock

We analyzed the upside potential for Capgemini stock using valuation assumptions that reflect its balanced growth profile, margin resilience, and a reasonable valuation multiple for a mature but still growing IT services leader.

Based on estimates of 3.8% annual revenue growth, 13.5% net income margins, and a normalized exit P/E multiple of 10.9x, the model projects Capgemini stock could rise from €136 to €164 per share in the next 2 years.

That would be a 20% total return, or a 9.9% annualized return over the next 2 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Capgemini stock:

1. Revenue Growth: 3.8%

Capgemini has delivered mid‑single‑digit revenue growth over the last decade, supported by steady demand for application services, infrastructure modernization, and consulting projects across its global client base.

In recent years, growth has been tempered by macro uncertainty and slower discretionary IT spending, but structural drivers like cloud migration, data modernization, and AI adoption remain intact and should support a gradual reacceleration as conditions normalize.

Based on these factors and analysts’ consensus estimates, a 3.8% annual revenue growth assumption seems reasonable for a mature IT services leader that still has room to expand in data, cloud, and AI‑driven solutions.

2. Operating Margins: 13.5%

Capgemini has historically delivered double‑digit operating margins, reflecting its ability to manage utilization, pricing, and delivery efficiency across its global workforce.

The company continues to optimize its cost base through industrialization of delivery, selective offshoring, and a disciplined mix shift toward higher‑value offerings such as consulting, cloud, and data services, which generally carry better profitability.

At the same time, Capgemini must keep investing in talent, innovation, and capabilities around AI, cybersecurity, and industry‑specific solutions, so margin expansion is likely to be gradual rather than dramatic.

Based on analysts’ consensus estimates, we use a 13.5% operating margin assumption, which aligns with the company’s recent performance and reflects a balance between efficiency gains and ongoing investment in growth initiatives.

3. Exit P/E Multiple: 10.9x

Capgemini currently trades at a P/E multiple in the low double‑digits, which is below some faster‑growing software and cloud peers but broadly consistent with other large, diversified IT services providers.

The multiple reflects the company’s solid competitive position and recurring revenue base, but it also incorporates investor caution around macro‑sensitive enterprise IT spending and the cyclicality of project‑based work.

Based on analysts’ consensus estimates, we maintain a 10.9x exit P/E multiple in our model, which is consistent with a steady, high‑quality IT services business that offers reasonable growth and cash generation without assuming an aggressive revaluation.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for CAP stock through 2030 show varied outcomes based on how growth, margins, and valuation evolve over time (these are estimates, not guaranteed returns):

- Low Case: CAP’s revenue growth and margins stay pressured as IT budgets remain tight → 6.2% annual returns

- Mid Case: Digital and cloud transformation projects stabilize and then recover → 11.9% annual returns

- High Case: Demand for large‑scale data, AI, and cloud programs accelerates → 16.9% annual returns

In the conservative scenario, the stock still offers modest positive returns supported by its diversified customer base, resilient services mix, and strong free cash flow, but the upside is limited if growth stays subdued for longer.

For both potential buyers and existing shareholders, the valuation model helps frame expectations around what different growth and margin paths could mean, rather than implying that any particular upside is guaranteed.

See what analysts think about CAP stock right now (Free with TIKR) >>>

How Much Upside Does Capgemini Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!