Key Takeaways:

- Electrophysiology Leadership: EP sales surged 63% in Q3 with FARAPULSE treating over 500,000 patients and capturing share in the overall EP market.

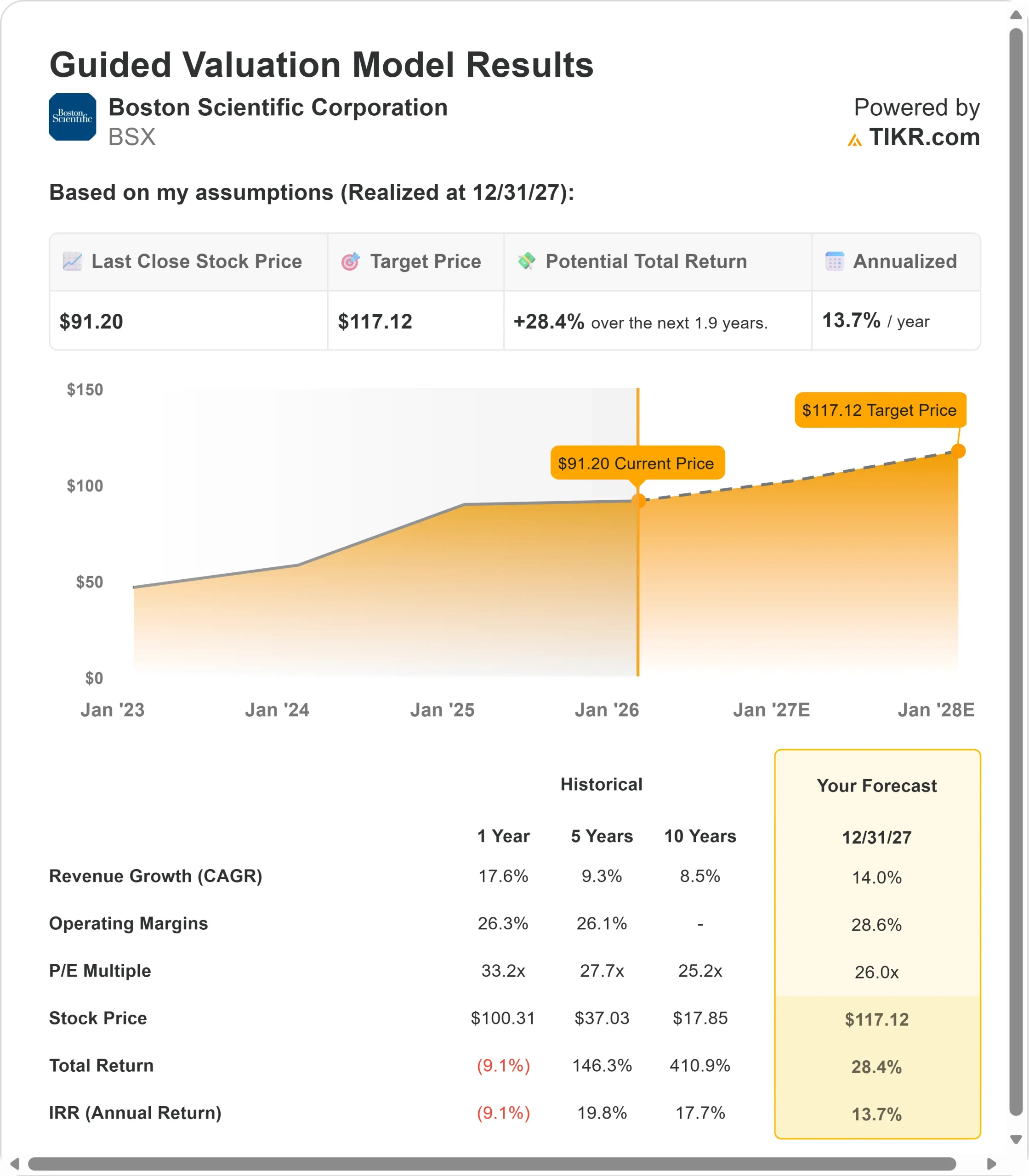

- Price Projection: Based on current momentum, the stock could reach $117 by December 2027.

- Potential Gains: This target implies a total return of 28% from the current price of $91.

- Annual Return: Investors could see roughly 14% growth per year over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Boston Scientific (BSX) just delivered another quarter that exceeded expectations across the board. Q3 organic sales grew 15%, crushing the high end of guidance at 12%-14%. Adjusted EPS of $0.75 grew 19%, also beating expectations. But the real story lies in two businesses redefining their markets: Electrophysiology and WATCHMAN.

- EP sales exploded by 63% as FARAPULSE continues its dominant run, with over 500,000 patients treated and 1 in 3 accounts now using the integrated OPAL mapping system.

- WATCHMAN grew an outstanding 35%, surpassing 600,000 patients treated with approximately 25% of U.S. procedures now done concomitantly with ablation—and that figure could double by 2028.

- The company raised full-year organic growth guidance to 15.5% and adjusted EPS guidance to $3.02-$3.04, representing 20%-21% growth.

Despite this momentum with operating margins expanding 80 basis points to 28% and $3.5 billion in expected free cash flow, BSX stock trades at $91, offering upside for investors who grasp the company’s category-creating innovation.

See analysts’ full growth forecasts and estimates for BSX stock (It’s free) >>>

What the Model Says for Boston Scientific Stock

We analyzed Boston Scientific through the lens of CEO Mike Mahoney’s vision to be “the market share leader, not just in PFA but the overall EP market over time” while simultaneously driving WATCHMAN’s 20% market CAGR for years to come.

The company is executing a differentiated growth strategy.

- FARAPULSE is simplifying AF ablation workflows with consistently reproducible results demonstrated in the FARADISE trial.

- WATCHMAN is penetrating the 5 million indicated patients through concomitant procedures, upcoming CHAMPION trial data in H1 2026, and next-generation WATCHMAN Elite expected in late 2027.

- Meanwhile, businesses like Interventional Cardiology with AGENT DCB, Peripheral Interventions, and Neuromodulation with the pending Nalu acquisition provide diversified growth.

Using a forecast of 14% annual revenue growth and 28.6% operating margins, our model projects the stock will rise to $117 within 1.9 years. This assumes a 26x Price-to-Earnings multiple.

That represents compression from Boston Scientific’s current P/E of 27.5x. As the company invests heavily in EP infrastructure, completes the Nalu Medical acquisition, and absorbs approximately $100 million in annual tariff headwinds, some multiple compression is reasonable.

The real value comes from sustained above-market growth across the portfolio and continued margin expansion.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for BSX stock:

1. Revenue Growth: 14%

Boston Scientific’s growth engine fires across multiple categories with differentiated innovation.

Electrophysiology Dominance: EP grew 63% with FARAPULSE leading as the #1 PFA technology. Global PFA penetration is expected to exit 2025 at 50% and reach 80% by 2028.

The company is launching FARAPOINT for complex patients by year-end and enrolled the OPTIMIZE trial studying Cortex AI for persistent AF.

With one-third of accounts now using integrated OPAL mapping, the ecosystem is strengthening.

WATCHMAN Market Creation: Growing 35% with 600,000 patients treated, WATCHMAN is still vastly underpenetrating the 5 million indicated patients.

Concomitant procedures with FARAPULSE are accelerating adoption faster than expected. The CHAMPION trial data in H1 2026 should expand indications, while the WATCHMAN Elite launch in late 2027 provides another catalyst.

Management is comfortable with 20% market CAGR for the years ahead.

Interventional Cardiology Transformation: The segment grew 23% driven by AGENT Drug-Coated Balloon in the U.S., which now benefits from New Technology Add-on Payment starting October 1st.

The STANCE trial studying AGENT in de novo lesions could double the indicated population. SEISMIQ IVL for coronary is expected to launch early 2027, following the FRACTURE trial completion in Q1 2026.

Diversified Portfolio Strength: China grew in the mid-teens despite substantial VBP headwinds in Peripheral, demonstrating the team’s ability to offset pricing pressures with innovation.

Recent NMPA approval for WATCHMAN FLX Pro and expanding EP presence drive confidence in sustained mid-teens growth in China. Endoscopy grew 9%, Neuromodulation 9%, and Peripheral Interventions 16% operationally.

2. Operating margins: 28.6%

Boston Scientific operates with industry-leading margin expansion while reinvesting for growth.

Current Performance: Q3 operating margin expanded 80 basis points to 28%, driven by strong drop-through from revenue outperformance and favorable product mix. Full-year margin expansion is now expected at 100 basis points despite $100 million in tariff headwinds.

Gross Margin Tailwinds: Adjusted gross margin reached 71%, up 60 basis points year-over-year. The improvement came from a favorable mix with high-growth, high-margin businesses like EP and WATCHMAN offsetting tariff impacts. Management expects gross margin to slightly improve for the full year.

Strategic Reinvestment: The company targets approximately 50 basis points of annual operating margin expansion through 2028. R&D spending at 9%-10% represents high-end peer investment supporting the innovation pipeline. The company is deliberately moderating the margin expansion pace to fund growth initiatives.

3. Exit P/E Multiple: 26x

The market currently values Boston Scientific at 27.5x earnings. We chose 26x for our exit multiple to stay conservative.

Slight Compression From Current: Boston Scientific’s P/E has averaged 33.2x over the past year and 27.7x over 5 years. The current multiple reflects strong execution and differentiated growth, but some compression is reasonable as the business scales and high-growth categories like EP face tougher comparisons.

Quality Premium Warranted: Boston Scientific deserves a premium to medtech averages due to its 15.5% organic growth (well above 9% market growth), 28% operating margins with 100 basis point annual expansion, clear leadership in EP and WATCHMAN with widening competitive moats, and disciplined capital allocation generating $3.5 billion in free cash flow with 70%-80% conversion.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

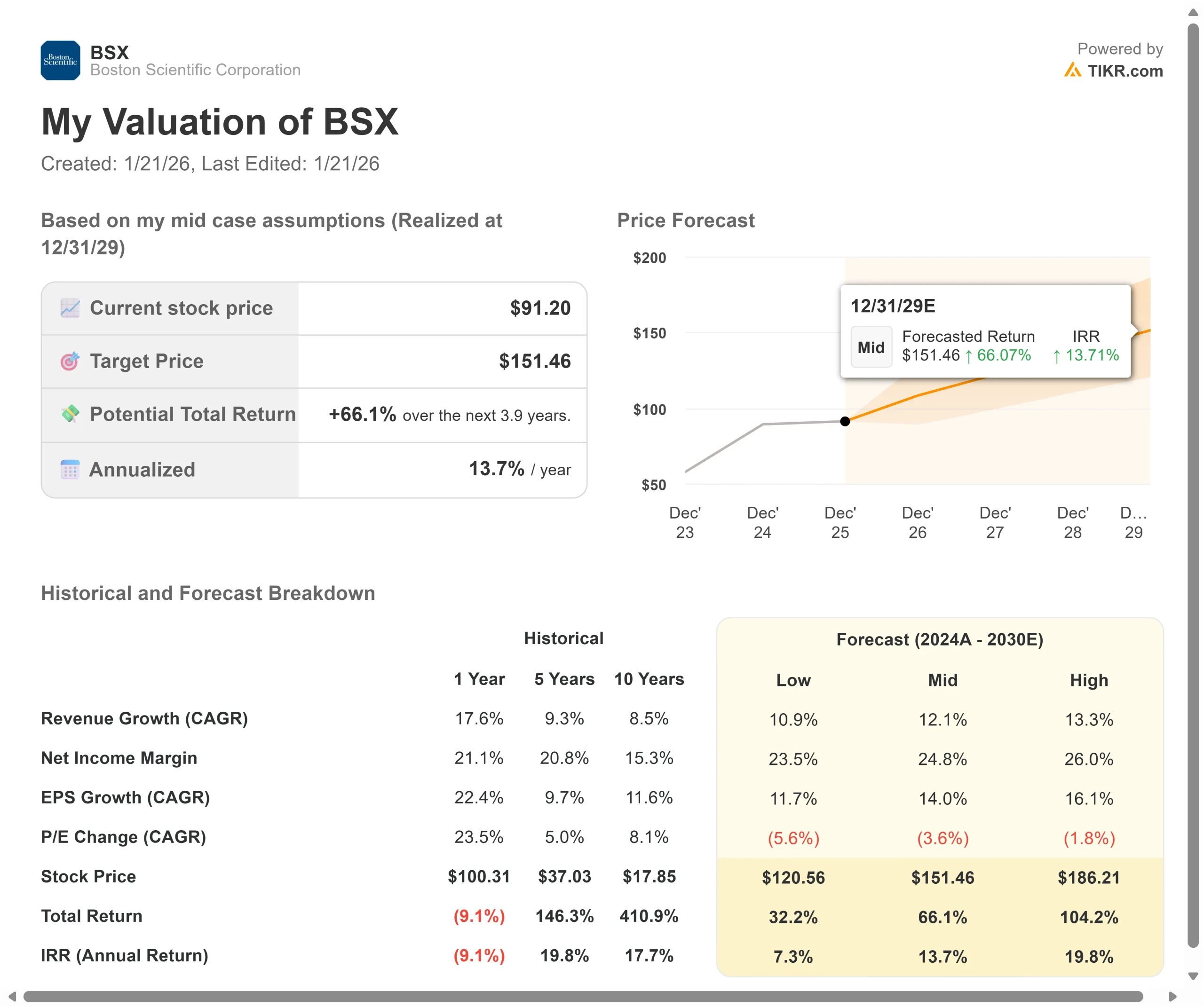

Medical device markets face competitive and regulatory risk. Here’s how Boston Scientific stock might perform under different scenarios through December 2027:

- Low Case: If revenue growth slows to 10.9% and margins compress to around 24%, the stock still offers a 7.3% annual return.

- Mid Case: With 12.1% growth and 25% margins (our base assumptions converted to net income margins), we expect an annual return of 13.7%.

- High Case: If CHAMPION data drives faster WATCHMAN adoption and Boston Scientific maintains 26% margins while growing at 13.3%, returns could hit 19.8% annually.

See what analysts think about BSX stock right now (Free with TIKR) >>>

The range reflects different outcomes for the CHAMPION trial, EP competitive dynamics as others launch PFA technologies, and execution on the DENALI CRM platform refresh launching through 2026-2028.

In the low case, competition gains share in EP, or CHAMPION fails to meaningfully expand WATCHMAN indications.

In the high case, concomitant adoption accelerates further, AGENT captures a significant coronary DCB share before competition arrives, and the Nalu acquisition opens substantial peripheral nerve stimulation growth.

How Much Upside Does Boston Scientific Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!