Key Takeaways:

- AI-Driven Growth: The data center segment hit a $1 billion run rate, growing 50% in fiscal 2025, while the ATE business surged 40%.

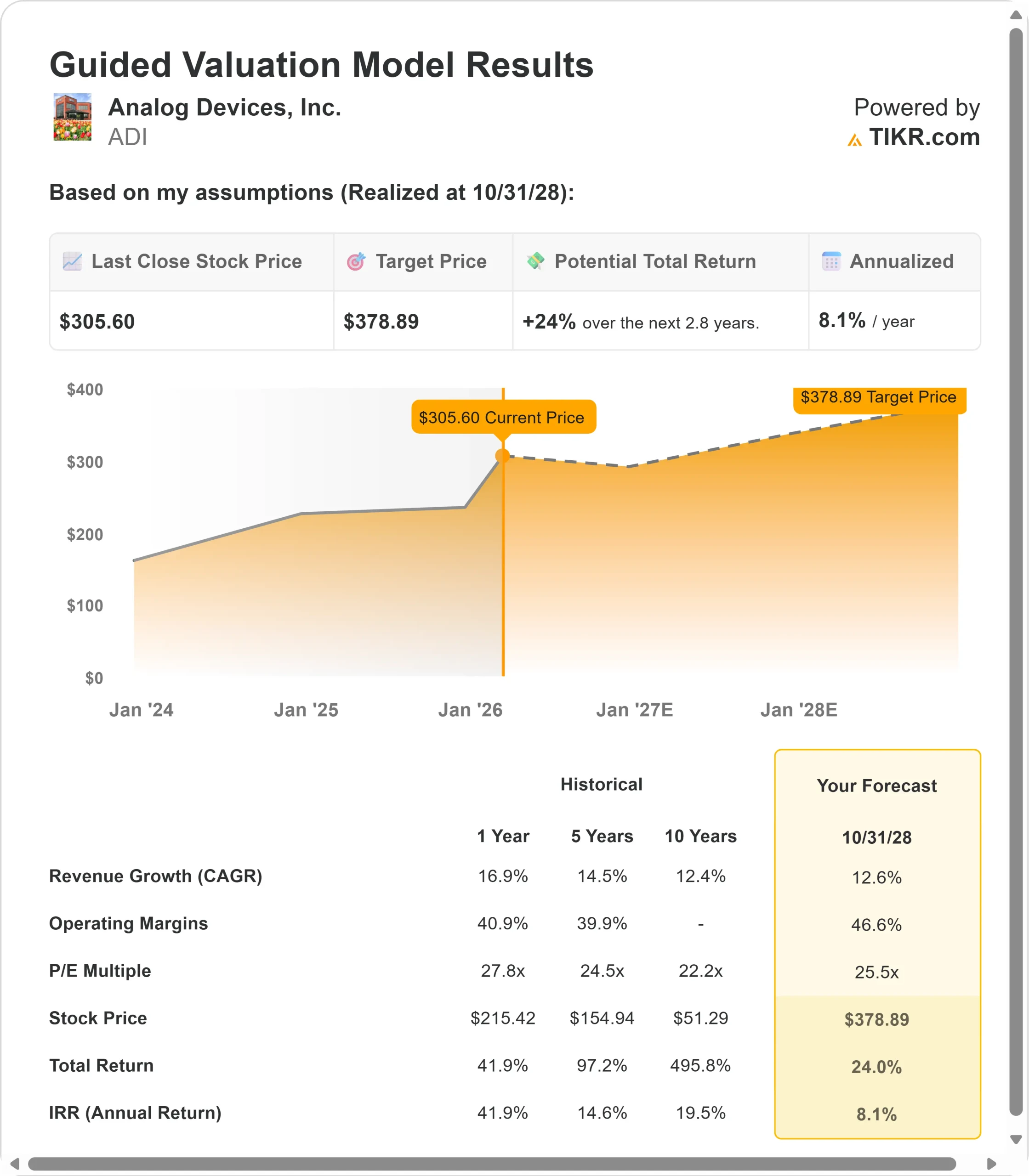

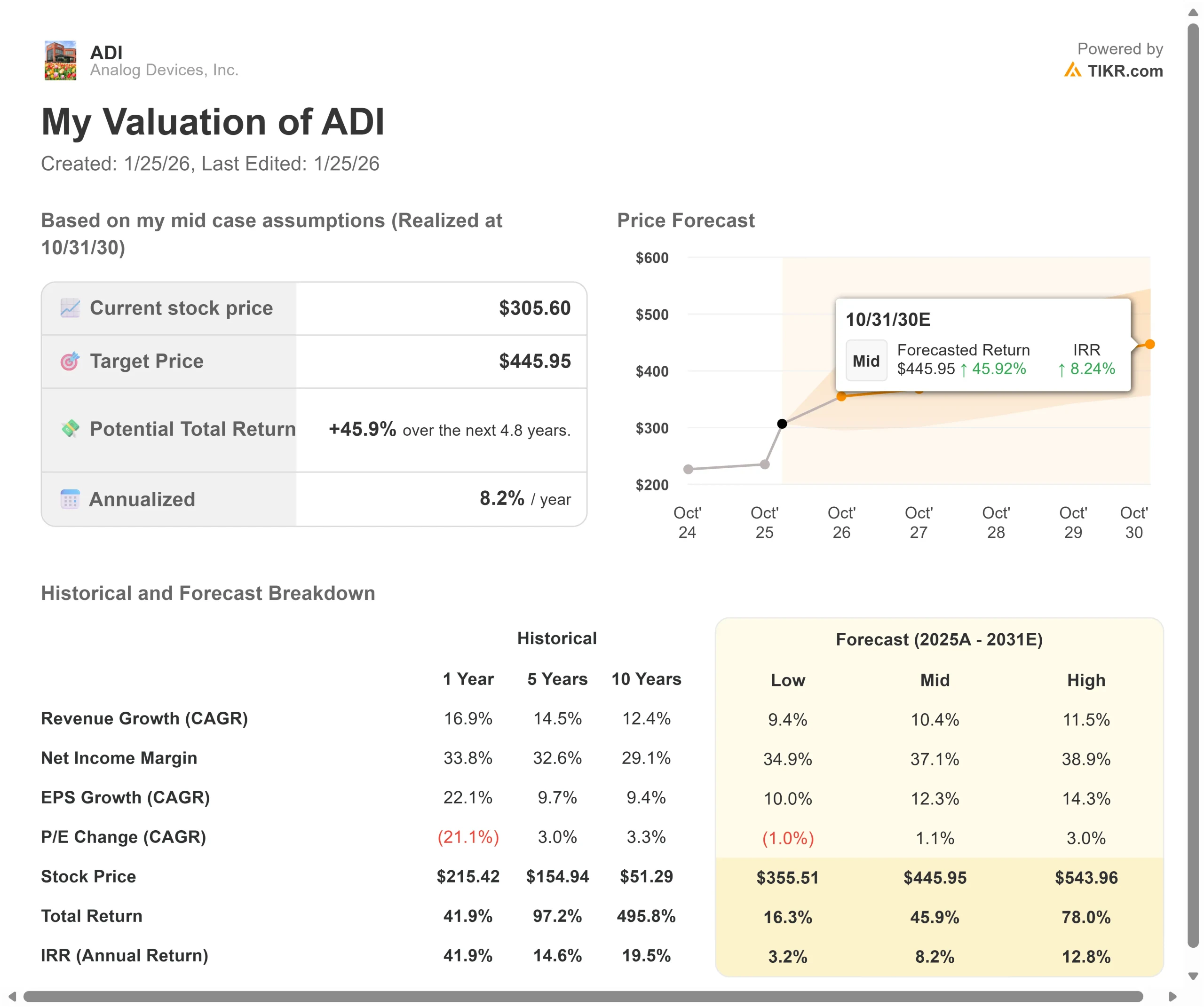

- Price Projection: Based on current momentum, the stock could reach $446 by October 2030.

- Potential Gains: This target implies a total return of 46% from the current price of $306.

- Annual Return: Investors could see roughly 8% annual growth over the next 4.8 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Analog Devices (ADI) delivered a strong year, posting 17% revenue growth in fiscal 2025. But the headline numbers barely capture what CEO Vincent Roche calls the company’s position “at the intelligent edge as it becomes a center of gravity for secular growth markets.”

- Revenue hit $11 billion, with double-digit growth across all end markets.

- The industrial segment posted record results in aerospace and defense, while the automatic test equipment business boomed on AI chip demand.

- Operating margins expanded to 41.9% as the company generated a record $4.3 billion in free cash flow.

With AI infrastructure spending accelerating and the Maxim acquisition delivering hundreds of millions in revenue synergies ahead of schedule, ADI is executing on multiple growth engines simultaneously. The company’s design pipeline grew by more than 20% in fiscal 2025, with particular strength in data centers, robotics, and energy management.

Despite strong performance and a fortress balance sheet with net leverage of just 0.9x, ADI stock trades at $306. This offers upside for investors who understand the company’s transformation from an analog chip supplier into an AI-enabled solutions provider.

See analysts’ full growth forecasts and estimates for ADI stock (It’s free) >>>

What the Model Says for Analog Devices Stock

We analyzed ADI through the lens of its evolution from a traditional analog semiconductor company into a comprehensive intelligent edge solutions provider.

The company’s technology breadth spans signal processing, power management, and increasingly sophisticated digital and AI capabilities.

With the Maxim acquisition now fully integrated, ADI combines industry-leading analog expertise with expanded power management and connectivity portfolios that are essential for AI infrastructure, automotive ADAS, and industrial automation.

The data center opportunity alone is massive.

- As hyperscalers deploy more AI accelerators requiring sophisticated power delivery and electro-optical connectivity, ADI’s content per server is expanding rapidly.

- The shift to 800-gigabit and 1.6-terabit optical modules demands the precision analog technology that ADI dominates.

Using a forecast of 10.4% annual revenue growth and 37.1% net income margins, our model projects the stock will rise to $446 within 4.8 years. This assumes a 29.5x price-to-earnings multiple.

That represents modest expansion from ADI’s current P/E of 27.8x. As the company demonstrates sustained double-digit growth in AI-related segments while maintaining industry-leading profitability, the market should reward this with a higher valuation.

The real value lies in ADI’s expanding content across secular growth markets and the Maxim synergies that are exceeding expectations.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ADI stock:

1. Revenue Growth: 10.4%

Analog Devices’ growth engine operates through multiple powerful channels.

AI Infrastructure Dominance: The data center segment reached a $1 billion run rate in Q4, growing 50% for three consecutive quarters. Management sees continued double-digit growth driven by 800G and 1.6T optical connectivity, power delivery solutions, and vertical power technology adoption. Hyperscalers continue increasing CapEx plans, directly benefiting ADI’s electro-optical interface and power management portfolios.

ATE Business Expansion: The automatic test equipment business hit an $800 million run rate, growing 40% in fiscal 2025. The transition to HBM4 memory chips will drive higher pin counts, more complexity, and greater instrumentation compute density. ADI is well-positioned with all major chip testers and expects this momentum to continue.

Maxim Synergies Accelerating: Revenue synergies from the Maxim acquisition reached hundreds of millions in fiscal 2025, ahead of the $1 billion target by 2027. The technology complementarity is playing out across automotive connectivity, power management, data centers, consumer, and healthcare applications. Management expects even stronger contributions in fiscal 2026.

Automotive Content Growth: Despite flat global vehicle production, ADI’s automotive revenue grew 16% to record levels. The company maintains 10% annual content growth driven by ADAS connectivity, functionally safe power solutions, and the new E2B Ethernet bus. Strong design wins position ADI for continued outperformance.

2. Operating margins: 37.1%

ADI operates with best-in-class profitability while investing heavily in future growth.

Current Performance: Fiscal 2025 gross margin reached 69.3%, up 140 basis points from the prior year. Operating margin expanded to 41.9% despite the normalization of variable compensation. The company converted 39% of its revenue into free cash flow.

Innovation Premium: New products command significantly higher average selling prices than legacy offerings, reflecting ADI’s ability to solve increasingly complex customer challenges. This pricing power, combined with operational leverage, supports margin expansion even during periods of heavy R&D investment.

Manufacturing Efficiency: After investing over $3 billion in capacity expansion following the Maxim acquisition, ADI has enhanced manufacturing optionality and resiliency. Higher utilization rates will drive further gross margin improvement as revenue grows beyond current levels.

Mix Improvement: Industrial and communications segments, which carry higher margins, are expected to lead growth in fiscal 2026.

3. Exit P/E Multiple: 29.5x

The market currently values ADI at 27.8x earnings. We assume modest expansion to 29.5x through our forecast period.

Quality Premium Warranted: ADI deserves a premium multiple given its market leadership position in high-performance analog, mission-critical applications across aerospace, defense, automotive safety, and AI infrastructure. The company combines secular growth exposure with fortress-like profitability and cash generation.

Technology Leadership: Record R&D investments are advancing ADI’s leadership in analog and mixed-signal, while expanding digital and AI capabilities. The company is building AI solutions directly into products, from acoustic platforms with machine learning to AI-enabled base stations.

Capital Allocation Excellence: ADI returned over $4 billion to shareholders in fiscal 2025 through dividends and buybacks while maintaining a strong balance sheet. The company targets a 100% free cash flow return over the long term, demonstrating confidence in its ability to sustain both growth investments and shareholder distributions.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Semiconductor companies face cyclical volatility and execution risk. Here’s how ADI stock might perform under different scenarios through October 2030:

- Low Case: If revenue growth slows to 9.4% and margins compress to 34.9%, the stock still offers a 3.2% annual return, reaching $356.

- Mid Case: With 10.4% growth and 37.1% margins (our base assumptions), we expect an annual return of 8.2% and the stock to reach $446.

- High Case: If AI infrastructure spending exceeds expectations and ADI maintains 38.9% margins while growing at 11.5%, returns could hit 12.8% annually, pushing the stock to $544.

See what analysts think about ADI stock right now (Free with TIKR) >>>

The range reflects different outcomes for AI CapEx spending, automotive production recovery, and execution on Maxim synergies.

In the low case, hyperscaler spending disappoints or tariffs significantly impact automotive demand.

In the high case, vertical power adoption accelerates faster than expected, aerospace and defense spending surges beyond current projections, and Maxim synergies exceed the $1 billion target as cross-selling gains traction across ADI’s expanded customer base.

How Much Upside Does Analog Devices Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!