Key Takeaways:

- Beyond the Smartphone: Qualcomm is racing to diversify, aiming for $22 billion in revenue from “non-handset” sources like Automotive and IoT by fiscal 2029.

- The AI Inference Bet: CEO Cristiano Amon is attacking the data center market with the Cloud AI 100, AI 200, and AI 250 chips, positioning them as efficient alternatives for large-scale inference.

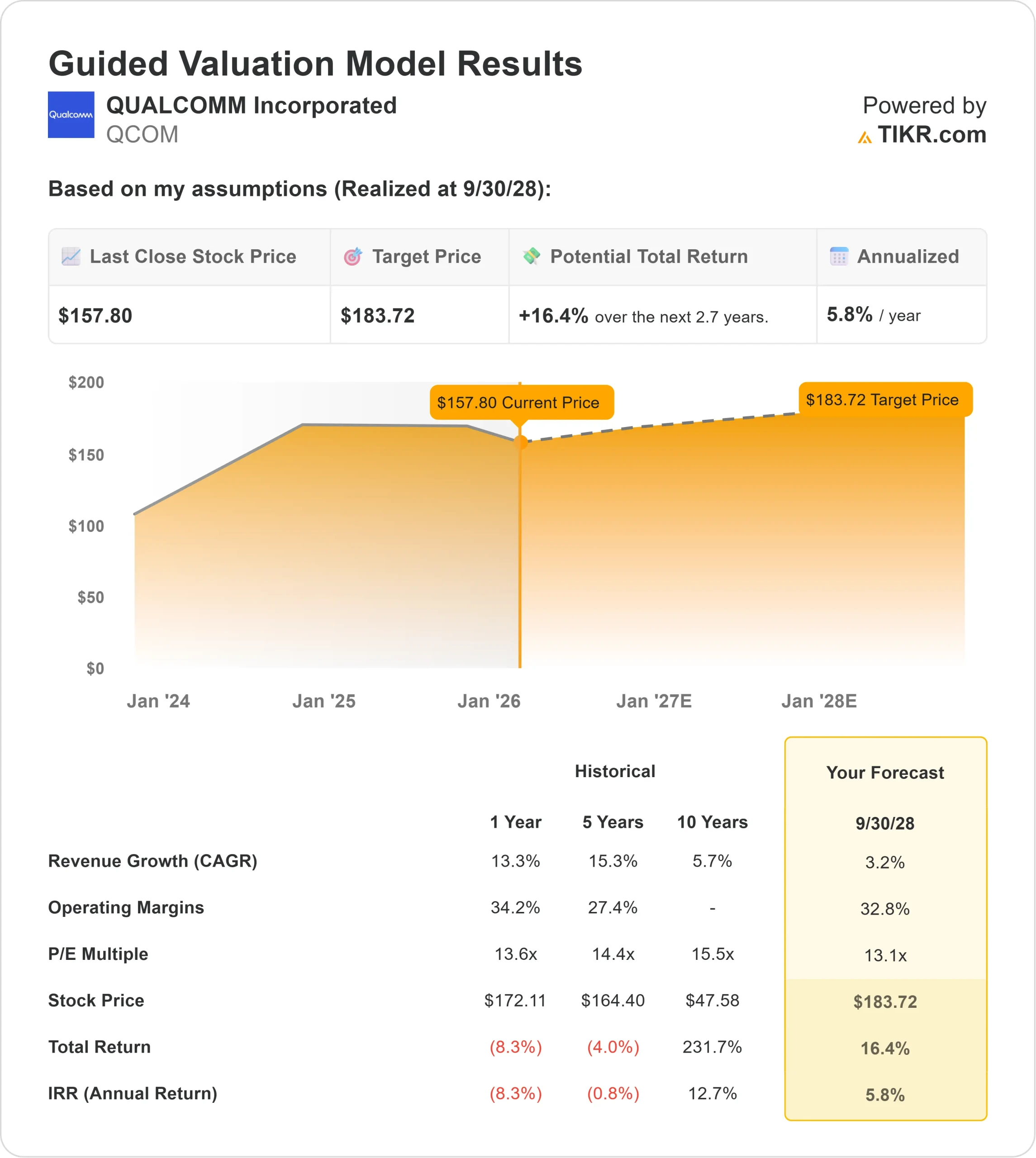

- Price Projection: The valuation model points to a target of $184 by 2028, suggesting the stock is nearing fair value.

- Modest Returns: With an implied 5.8% annualized return, the model signals a “Hold,” indicating that investors are paying a fair price for moderate growth.

Qualcomm (QCOM) is fighting to prove it is more than just a smartphone stock.

With the handset market maturing, CEO Cristiano Amon is pivoting the company hard toward the Connected Intelligent Edge.

The strategy hinges on two massive bets: Automotive and AI.

In Auto, the Snapdragon Digital Chassis has become an industry standard, driving a revenue pipeline that is rapidly converting to sales.

In AI, Qualcomm is challenging Nvidia’s dominance in inference (running AI models) with its new AI200 and AI250 processors, aiming to capture the “decode portion” of data center workloads.

Financially, the company remains a cash cow.

LTM Revenue stands at $44.3 billion, with healthy Operating Margins of 28.0%.

However, with the stock trading at $158, the market seems to have already priced in much of this stability. Is there enough growth left to justify buying more?

What the Model Says for QCOM Stock

This analysis evaluates Qualcomm’s potential through 2028, weighing the auto growth against the stagnation in smartphones.

The model signals a Hold.

Using a forecast of 3.2% Revenue Growth (CAGR) and 32.8% Operating Margins, the model points to a target price of $184 by September 2028.

This implies a 5.8% annualized return from today’s levels.

Essentially, the model suggests that Qualcomm is fairly valued. The diversification efforts are real, but they are currently just offsetting the slow growth of the massive mobile business rather than driving explosive upside.

Wall Street is slightly more optimistic.

The average street target for early 2026 is roughly $191, implying 21% upside over the next 12 months, suggesting analysts are pricing in a faster adoption of the AI chips than the conservative model assumes.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for QCOM stock:

1. Revenue Growth: 3.2%

The pivot is happening, but slowly.

Management confirmed they are on track for $22 billion in non-handset revenue by FY29, which would be “100% incremental” to their model.

However, the core handset market remains cyclical and saturated.

The model forecasts a modest 3.2% CAGR, reflecting the reality that while Auto and IoT are growing fast, they are fighting against the gravity of a massive, mature mobile segment.

2. Operating Margins: 32.8%

Gross margins are strong at 55.4%, driven by the company’s lucrative licensing division (QTL) and high-end Snapdragon chips.

The model assumes Operating Margins will expand to 32.8% by 2028, reflecting the company’s ability to maintain pricing power even as it enters new, competitive markets like the data center.

3. Exit P/E Multiple: 13.1x

Qualcomm currently trades at a forward P/E of roughly 13-14x, a discount to the broader tech sector.

The model assumes a stable exit multiple of 13.1x.

This multiple treats Qualcomm as a mature semiconductor stock rather than a high-growth AI darling. If the AI200 chips take a significant share from Nvidia, this multiple could expand, providing upside optionality.

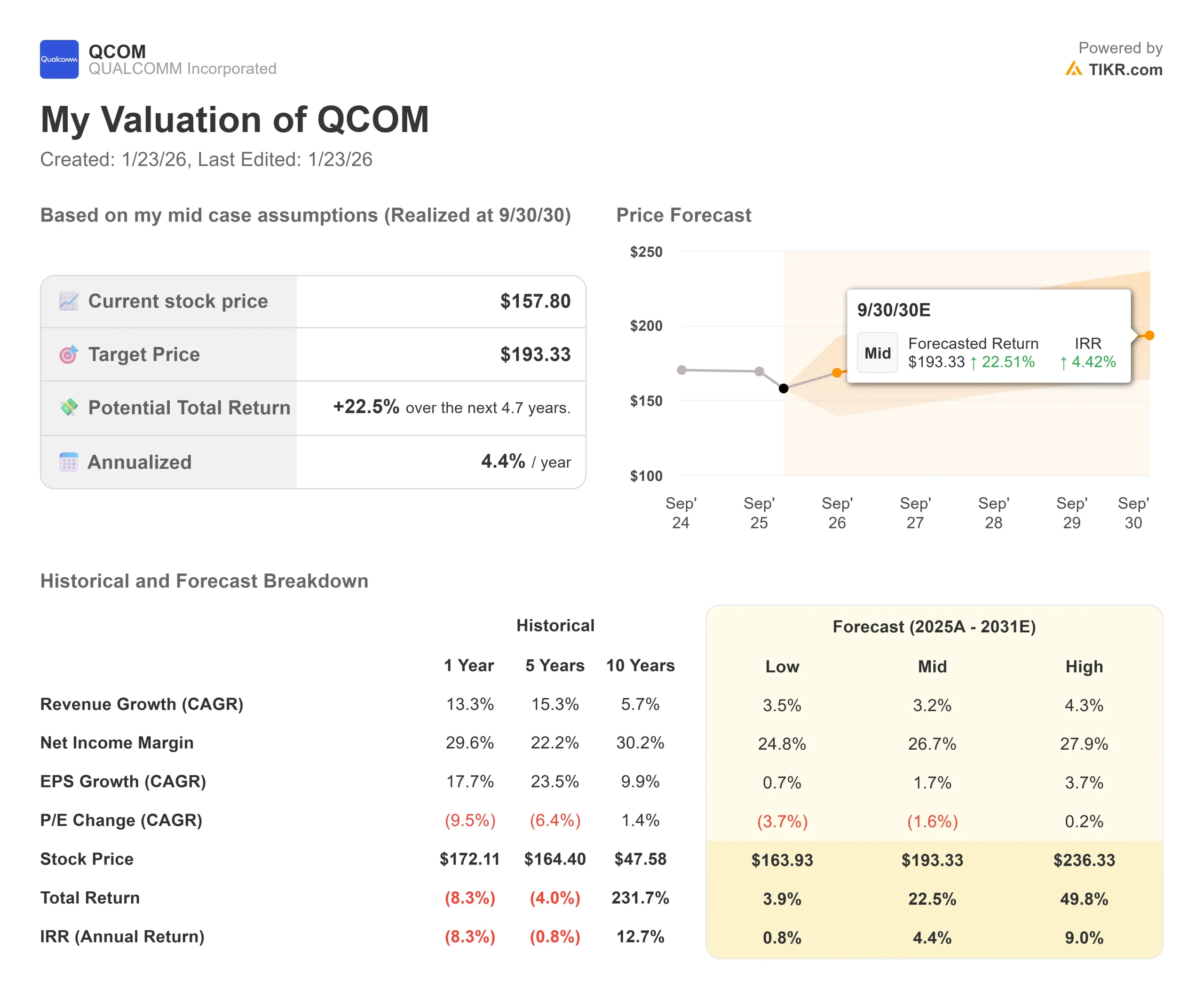

What Happens If Things Go Better or Worse?

The “Base Case” offers market-matching returns, but the variance depends on the success of the non-handset business (these are estimates, not guaranteed returns):

- Low Case: If the handset market contracts further, the stock could stagnate near $164, offering negative real returns.

- Mid Case: With steady execution on the diversification plan, the target sits at $184, a 5.8% Annual Return.

- High Case: If Qualcomm successfully breaks into the data center market, the stock could re-rate significantly higher, but the model remains conservative for now.

See what analysts forecast for the next 5 years for QCOM stock (Free with TIKR) >>>

How Much Upside Does QCOM Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!