Key Takeaways:

- The Falcon Flex Juggernaut: CrowdStrike is rewriting the rules of procurement with “Falcon Flex,” a consumption-based model that has already secured $1.35 billion in ARR, allowing customers to add modules instantly without new contracts.

- Hyper-Growth at Scale: Despite its massive size, the company is accelerating. Revenue grew 29% to over $4.57 billion, driven by the massive displacement of legacy vendors.

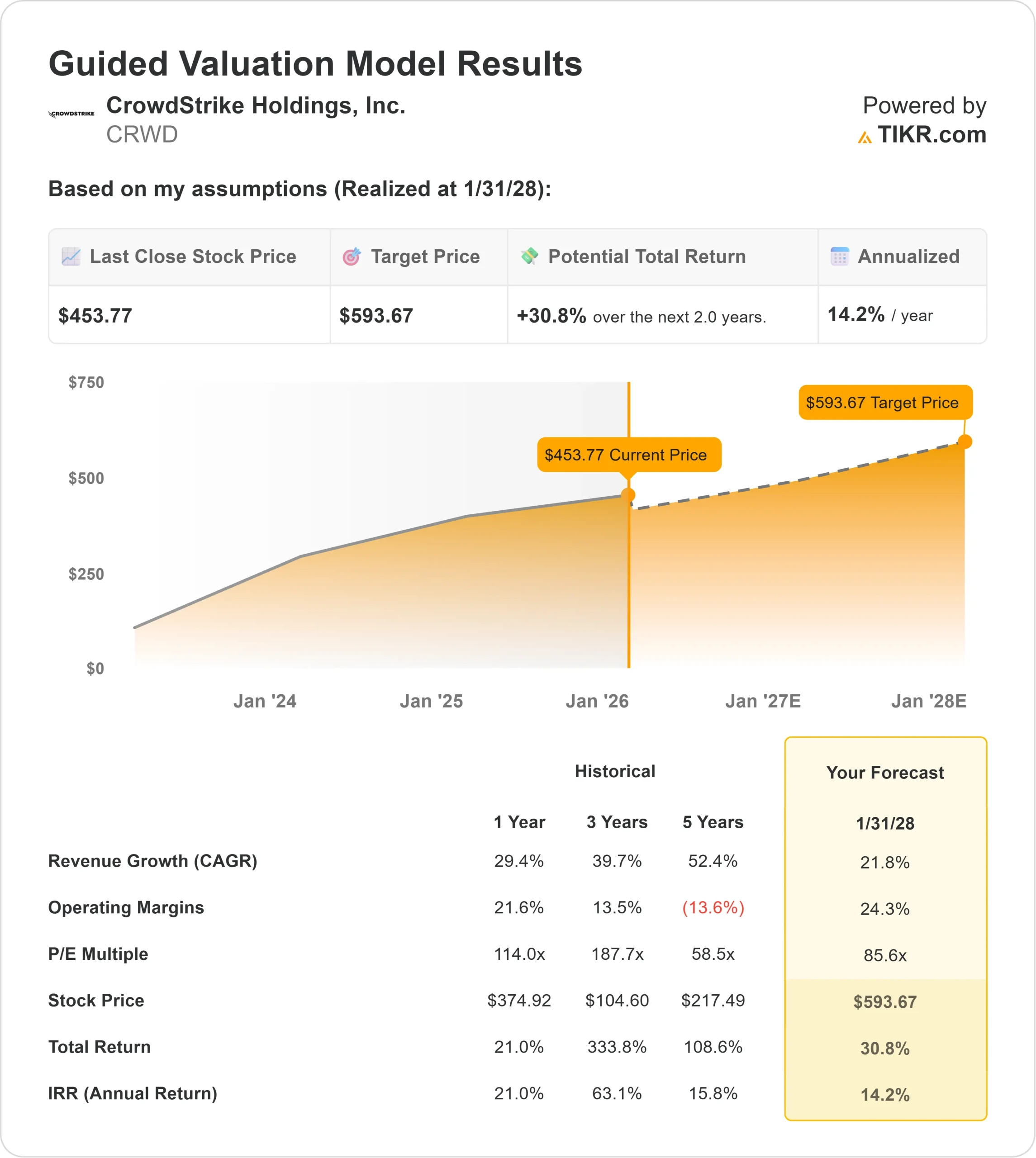

- Price Projection: The valuation model points to a target of $594 by early 2028, largely aligned with the current Wall Street consensus.

- Solid Returns: This target implies a 14% annualized return, signaling that while the stock is expensive, the growth runway justifies a “Buy” rating.

CrowdStrike (CRWD) is no longer just an endpoint security company.

CEO George Kurtz is executing a masterclass in platform strategy.

By consolidating endpoint, identity, and cloud security into a single agent, CrowdStrike is displacing legacy vendors like Splunk and McAfee at a rapid clip.

The numbers are staggering.

Annual Recurring Revenue (ARR) grew 33% year-over-year to reach new heights.

But the real story is cash flow.

While the company posted a GAAP operating loss of $284 million as it invests in growth, it is a cash machine, generating $1.23 billion in Levered Free Cash Flow over the last twelve months—a robust 27% margin.

With the stock trading at $454, it isn’t cheap—but best-in-class assets rarely are.

Is this the moment to pay up for quality, or wait for a dip that may never come?

What the Model Says for CRWD Stock

This analysis evaluates CrowdStrike’s potential through early 2028, factoring in the long-term displacement of legacy SIEM providers.

The model signals a Buy.

Using a forecast of 21.8% Revenue Growth (CAGR) and 24.3% Operating Margins, the model points to a target price of $594 by January 2028.

This implies a solid 14.2% annualized return from today’s levels.

This output suggests that CrowdStrike is “fairly valued” for its growth profile, offering double-digit returns without requiring an unrealistic valuation expansion.

Wall Street shares this view.

The average street target for early 2026 is roughly $554, which puts the model’s $594 target within striking distance of the consensus view.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CRWD stock:

1. Revenue Growth: 21.8%

First is Falcon Flex, which has removed friction from the sales process. Customers can now try and buy modules like “Identity Protection” instantly, driving net retention rates higher.

Second is the Next-Gen SIEM market.

CrowdStrike is aggressively targeting legacy SIEM vendors, offering a faster, cheaper alternative. Management noted that this replacement cycle is “accelerating,” with 80%+ of the data already sitting in their platform.

The model forecasts a robust 21.8% CAGR, assuming CrowdStrike captures a significant chunk of the $90 billion AI-security market.

2. Operating Margins: 24.3%

Gross margins remain elite at 74.3%, giving the company immense pricing power.

As the company cross-sells more modules to existing customers (who already have the agent installed), the cost of sales drops effectively to zero for that incremental revenue.

The model assumes Operating Margins will expand to 24.3% by 2028, a natural progression for a software monopoly in the making.

3. Exit P/E Multiple: 85.6x

CrowdStrike currently trades at a forward P/E of roughly 100x, a valuation reserved for the elite “Rule of 40” companies.

The model assumes an exit multiple of 85.6x.

While high, this multiple reflects the scarcity of software companies growing at 20%+ with 27%+ free cash flow margins.

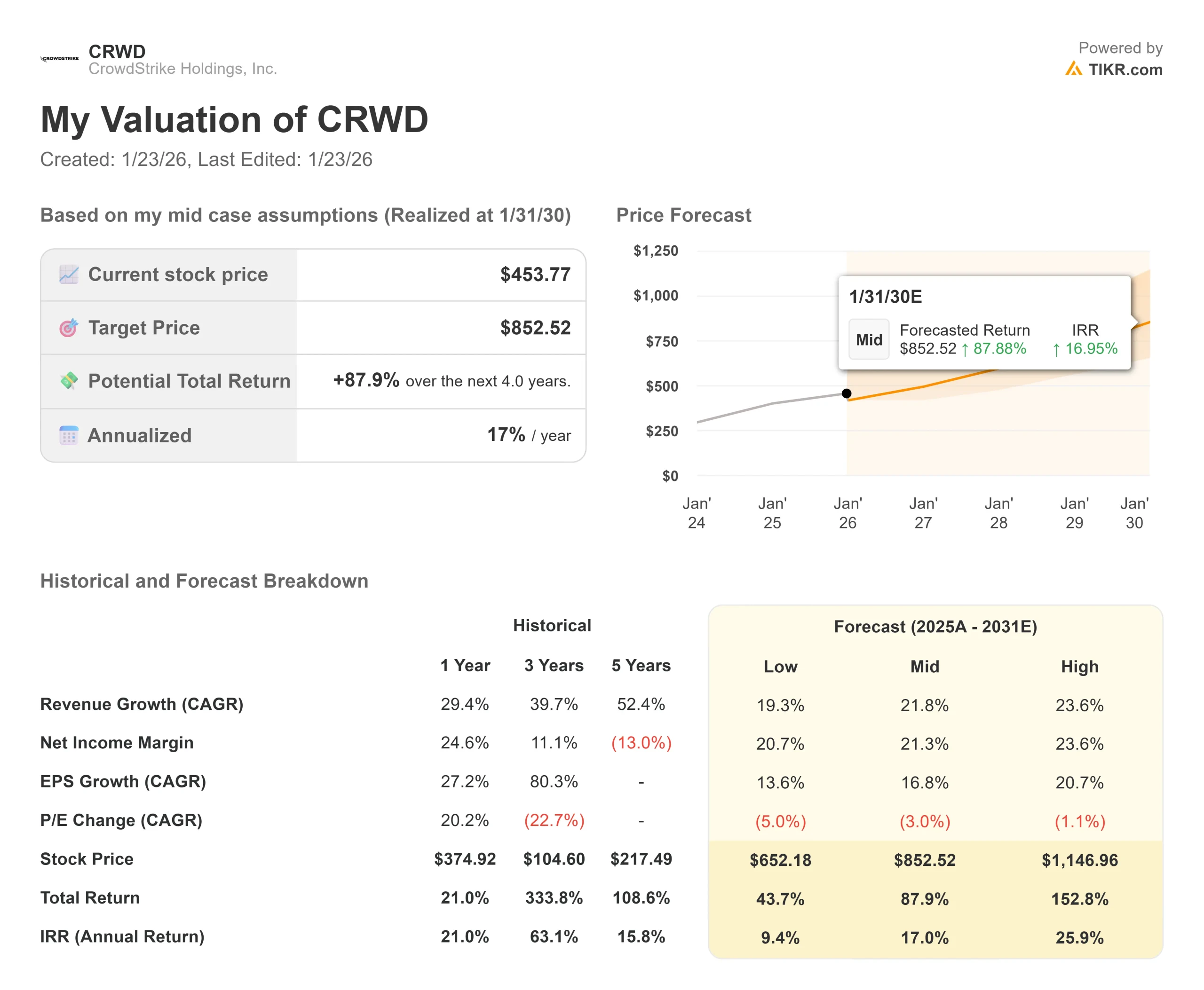

What Happens If Things Go Better or Worse?

The risk/reward profile is balanced, offering steady compounding in the base case (these are estimates, not guaranteed returns):

- Low Case: If the economy cools and IT budgets freeze, the stock could stagnate near the consensus target of $550, limiting short-term upside.

- Mid Case: If the Falcon Flex adoption continues at its current pace, the model points to a 31% Total Return by 2028.

- High Case: If AI-driven cyberattacks force companies to double down on security spend, the stock could outperform these targets, but the “Base Case” already prices in significant success.

See what analysts forecast for the next 5 years for CRWD stock (Free with TIKR) >>>

How Much Upside Does CRWD Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!