Key Takeaways:

- Revenue Expansion: Celsius Holdings posted roughly $2 billion in trailing revenue, with a 29% growth outlook reflecting sustained energy drink demand.

- Margin Profile: Operating margins near 22% demonstrate improving scale economics as distribution efficiency and brand leverage increase.

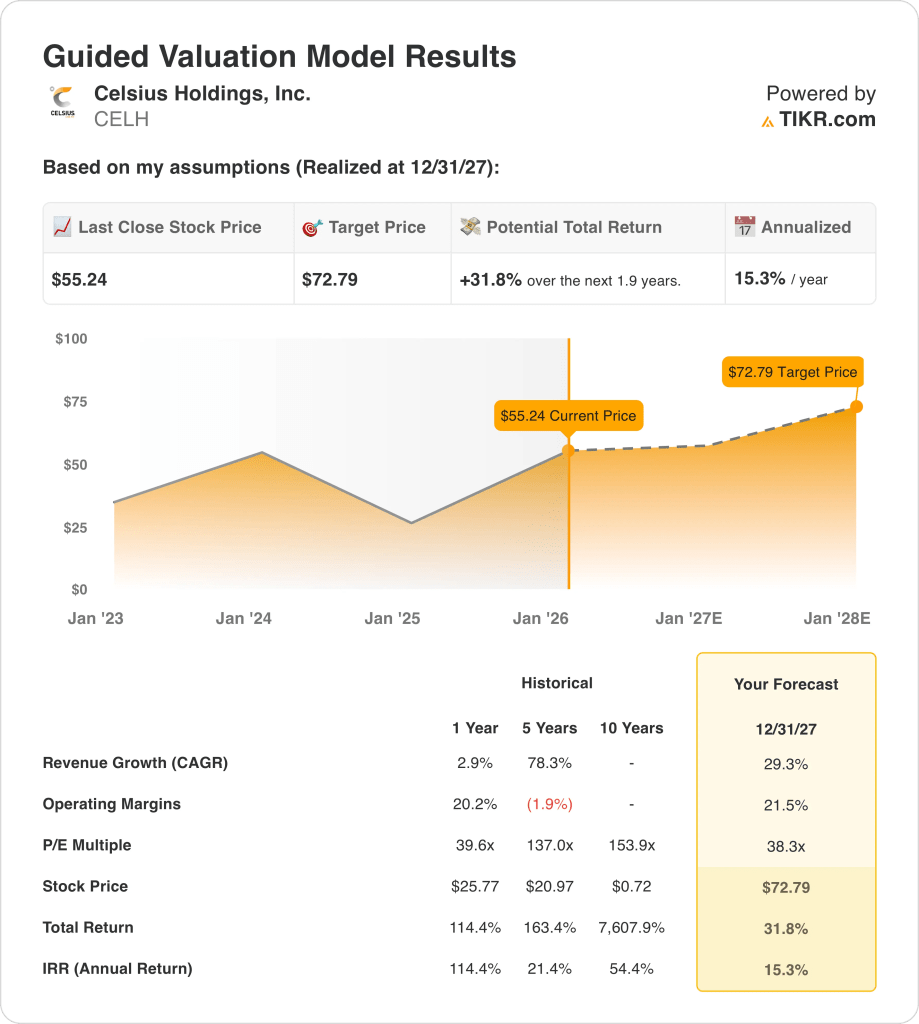

- Price Projection: Based on current assumptions, Celsius Holdings stock could reach $73 by 2027 from a price near $55.

- Return Outlook: This implies total upside of about 32% and an annualized return near 15% over the next two years.

Celsius Holdings (CELH) produces functional energy drinks, with products sold globally across retail and e-commerce, supporting a market value near $7 billion.

Leadership additions, including a new CMO and PepsiCo-linked board member, strengthen brand execution amid intensifying energy drink competition.

Celsius generated roughly $2 billion in trailing revenue, reflecting rapid category growth and expanding distribution across convenience, fitness, and mass channels.

Operating margins near 20% show improved cost discipline, while profitability benefits from scale, premium pricing, and growing repeat consumption.

Despite revenue growth near 29%, the stock trades around 38x earnings, creating tension between execution strength and valuation expectations.

What the Model Says for CELH Stock

We analyzed CELH Stock using assumptions on brand-led demand growth, improving operating leverage, and premium positioning within global energy drinks.

Based on 29.3% revenue growth, 21.5% operating margins, and a 38.3x exit multiple, the model projects CELH reaching $72.79.

That implies a 31.8% total return, or a 15.3% annualized return over 1.9 years, ending at $72.79.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CELH stock:

1. Revenue Growth: 29.3%

Revenue grew from $0.31 billion in 2021 to $2.13 billion LTM, reflecting sustained brand adoption across U.S. convenience and fitness channels.

Quarterly revenue reached $0.73 billion, up 173% year over year, confirming shelf expansion, repeat consumption, and distributor execution strength.

Growth durability depends on international scaling and competitive intensity, while category momentum and health-oriented positioning provide structural demand support.

According to consensus analyst estimates, 29.3% revenue growth reflects normalization from hypergrowth while maintaining premium energy share gains globally.

2. Operating Margins: 21.5%

Operating margins improved from negative levels in 2022 to about 20%, reflecting scale benefits across manufacturing, logistics, and marketing efficiency.

EBIT margins near 23% reflect pricing discipline and stronger fixed-cost absorption as volumes scale across major retail partners.

Margin risks include promotional pressure and input costs, while upside comes from international mix and lower per-unit distribution expenses.

In line with analyst consensus projections, 21.5% operating margins balance recent profitability gains with reinvestment needs to sustain brand growth.

3. Exit P/E Multiple: 38.3x

Celsius previously traded between 40x and 150x earnings during peak growth, reflecting investor confidence in category leadership and expansion runway.

The current valuation embeds moderation as growth normalizes, with investors cautious about competitive responses from larger beverage incumbents.

Execution consistency and sustained margin delivery are required to justify premium valuation levels without renewed multiple expansion.

A 38.3x exit multiple reflects strong brand economics while accounting for slower but still elevated growth expectations.

What Happens If Things Go Better or Worse?

Celsius’s outcomes depend on sustained energy drink demand, brand execution, and margin discipline, setting up a range of possible paths through 2029.

- Low Case: If category growth cools and promotions rise, revenue grows around 19.1% with margins near 12.5% → 2.9% annualized return.

- Mid Case: With core distribution and brand momentum intact, revenue growth near 21.0% and margins improving toward 13.6% → 10.9% annualized return.

- High Case: If international expansion accelerates and costs stay controlled, revenue reaches about 22.9% with margins near 14.2% → 18.2% annualized return.

How Much Upside Does It Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!