Key Takeaways:

- Revenue Trajectory: Disney delivered about $94 billion in trailing revenue, with growth near 5% supported by streaming pricing and parks demand.

- Margin Recovery: Operating margins near 20% reflect cost control and improved streaming economics after prior restructuring.

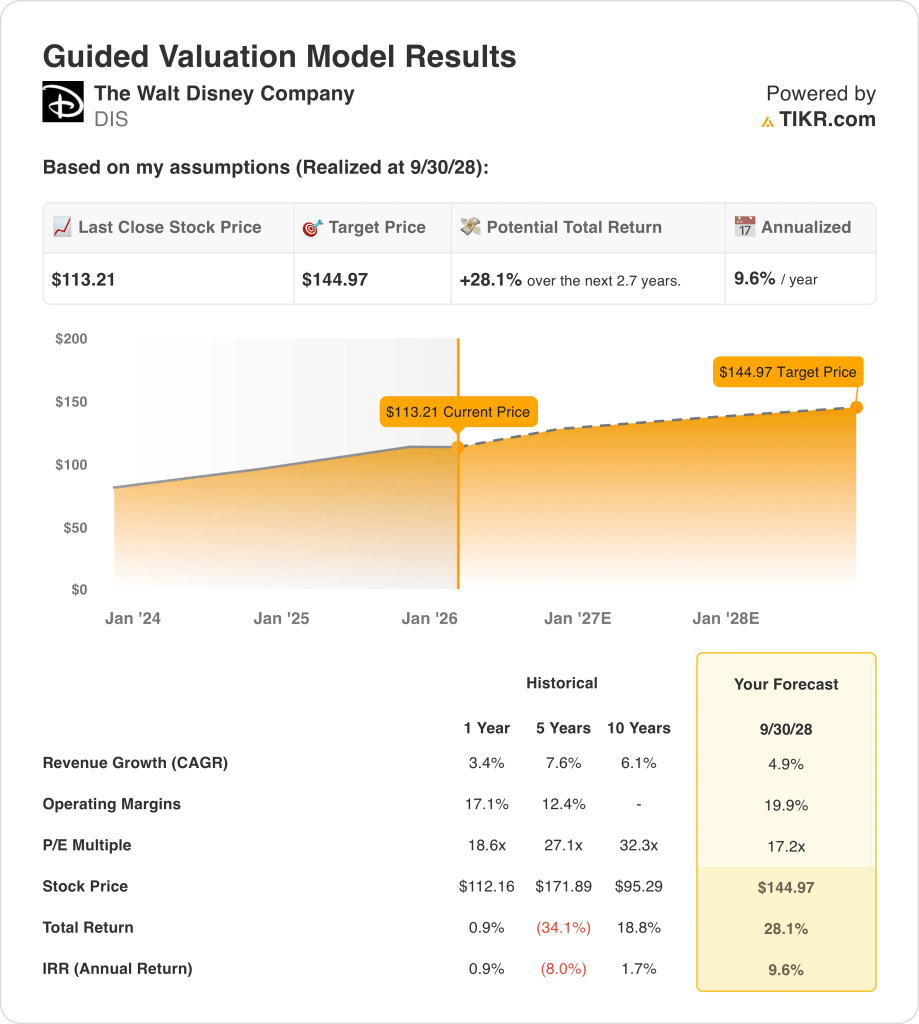

- Price Projection: Based on valuation assumptions, Disney stock could reach about $145 by 2028 from a current price near $113.

- Return Profile: This implies roughly 28% total upside, translating to about 10% annualized returns over the next 3 years.

The Walt Disney Company (DIS) is global entertainment, sports, and experiences businesses giant that generated more than $94 billion revenue last year across media networks, streaming, and parks.

Recent leadership changes at Lucasfilm and a new enterprise marketing organization sharpen creative execution as Disney restructures content, branding, and distribution priorities.

Disney stock produced roughly $2 billion in quarterly net income with operating margins near 15%, reflecting improving efficiency across streaming and parks operations.

Revenue growth near 5% is supported by streaming price increases, ESPN distribution deals, and park attendance, while margin gains come from cost discipline and content rationalization.

Even with operating margins approaching 20% and a valuation near 17x earnings, the stock still reflects caution around execution consistency.

What the Model Says for DIS Stock

We evaluated Disney’s outlook based on steady streaming scale, parks cash generation, and improving operating discipline across core entertainment segments.

Assuming 4.9% revenue growth, 19.9% operating margins, and a 17.2x exit multiple, the model implies a $144.97 share price.

That equates to a 28.1% total return, or a 9.6% annualized return by September 2028.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for DIS stock:

1. Revenue Growth: 4.9%

Disney stock generated roughly $94 billion in LTM revenue, with 3% one-year growth and 8% five-year CAGR, reflecting mature scale across media and experiences.

Recent revenue stability reflects parks attendance normalization and streaming losses narrowing, offset by slower linear television advertising and sports network pressure.

Forward growth depends on streaming profitability, park pricing discipline, and content monetization rather than subscriber expansion or aggressive international rollout.

A 4.9% revenue growth outlook balances normalized parks demand with steady streaming and licensing contributions.

2. Operating Margins: 19.9%

Disney’s operating margins reached about 17% recently, recovering from prior lows as cost reductions and streaming losses narrowed materially.

Margin improvement reflects lower content spend growth, ESPN pricing discipline, and higher-margin parks revenue supporting consolidated profitability.

Upside depends on sustained streaming breakeven and park pricing power, while risks include sports rights inflation and advertising cyclicality.

A 19.9% operating margins reflect normalized cost structures without assuming peak-cycle media profitability.

3. Exit P/E Multiple: 17.2x

Disney currently trades near 19× earnings, below historical peaks above 27× during stronger growth and clearer earnings momentum.

Investor caution reflects legacy media decline, streaming execution risk, and capital intensity, despite improving free cash flow trends.

The valuation assumes earnings stability and disciplined capital allocation rather than renewed growth multiple expansion.

Based on street consensus estimates, a 17.2× exit multiple supports a $144.97 target price and roughly 9.6% annualized returns.

What Happens If Things Go Better or Worse?

DIS stock outcomes depend on parks demand, streaming profitability, and content discipline, creating multiple execution paths through fiscal 2030.

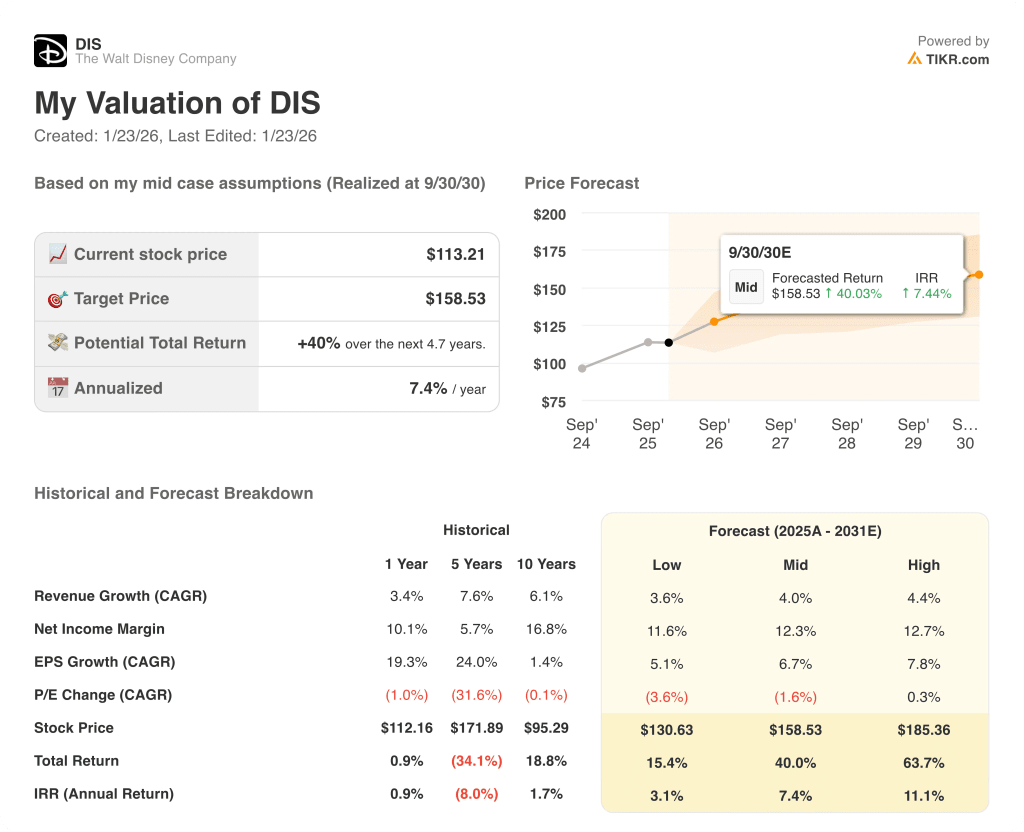

- Low Case: If media pressure persists and parks soften, revenue grows around 3.6% with margins near 11.6% → 3.1% annualized return.

- Mid Case: With parks stability and streaming breakeven, revenue growth near 4.0% and margins improving toward 12.3% → 7.4% annualized return.

- High Case: If streaming profits scale and parks pricing holds, revenue reaches about 4.4% with margins near 12.7% → 11.1% annualized return.

How Much Upside Does It Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!