Key Takeaways:

- Robust Growth: Stryker delivered 9.5% organic growth in Q3, marking four consecutive years of roughly 10% organic growth

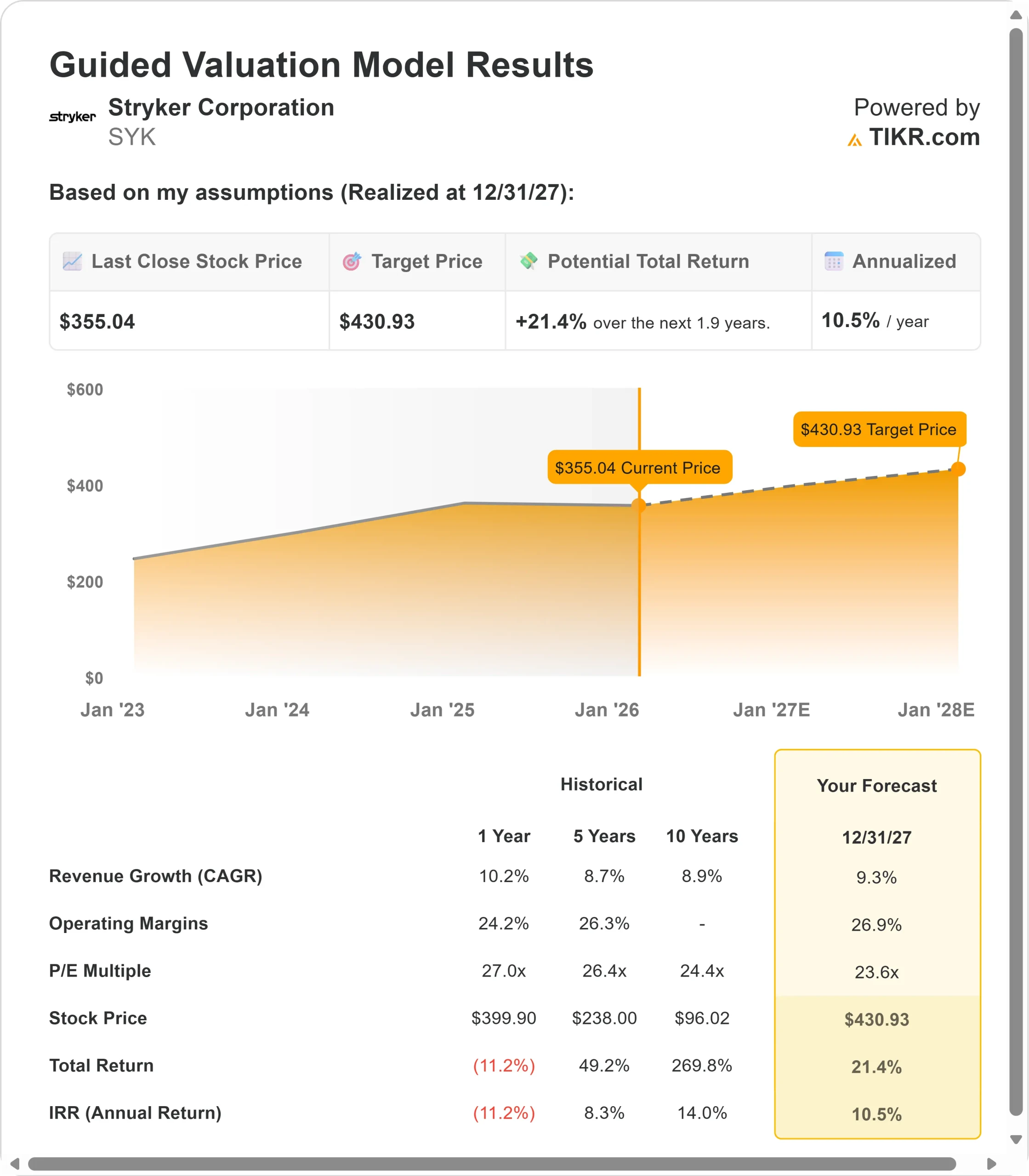

- Price Projection: Based on current momentum, the stock could reach $431 by December 2027

- Potential Gains: This target implies a total return of 21% from the current price of $355

- Annual Return: Investors could see roughly 11% annual growth over the next 1.9 years

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Stryker (SYK) just posted its best-ever Q3 for Mako robot installations, both in the U.S. and globally. The company grew organic sales 9.5% against a tough 11.5% comparison from last year, while expanding adjusted operating margins by 90 basis points to 25.6%.

With double-digit growth in Orthopaedics and high single-digit gains in MedSurg and Neurotechnology, CEO Kevin Lobo described this as the company’s “fourth consecutive year of growing roughly 10% organically.”

- The Knee business stood out with 8.4% U.S. growth, driven by market-leading robotics and the Mako platform’s high utilization rates.

- Trauma and Extremities surged 13.2%, driven by strength in Upper Extremities and core trauma products.

- The recently acquired Inari business delivered double-digit pro forma growth despite destocking headwinds.

Tariff impacts reached $200 million for the full year. With nearly $3 billion in year-to-date operating cash flow and a strong balance sheet, SYK stock at $355 offers upside for investors who understand the company’s margin-expansion story and its dominance in capital equipment.

See analysts’ full growth forecasts and estimates for SYK stock (It’s free) >>>

What the Model Says for Stryker Stock

We analyzed Stryker through the lens of its transformation from a pure medical device maker into a comprehensive surgical robotics, capital equipment, and medical technology platform.

The company operates across three segments: MedSurg and Neurotechnology (instruments, endoscopy, medical beds, vascular products), Orthopaedics (knees, hips, trauma, extremities), and the newly integrated Inari vascular business.

With record Mako installations, strong procedural volumes, healthy hospital capital budgets, and only a modest decline in monthly penetration in top markets, Stryker has significant room to run.

Many hospitals that purchased Mako systems are now buying them outright rather than leasing, signaling confidence in the technology’s ROI.

Using a forecast of 9.3% annual revenue growth and 26.9% operating margins, our model projects the stock will rise to $431 within 1.9 years. This assumes a 23.6x price-to-earnings multiple.

That represents a slight contraction from Stryker’s current P/E of 24.5x.

As the company navigates tariff headwinds while maintaining disciplined margin expansion and investing in M&A, the multiple should compress modestly.

However, the real value lies in sustained organic growth across all three segments and the continued adoption of robotic-assisted surgery.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for SYK stock:

1. Revenue Growth: 9.3%

Stryker’s growth engine operates across multiple proven franchises.

Robotic Surgery Expansion: Mako installations hit all-time Q3 records. Every installation drives ongoing implant sales with high utilization rates. The platform now addresses complex primary hip cases and hip revisions, expanding the addressable market beyond standard procedures.

Capital Equipment Strength: Hospitals maintain strong balance sheets with robust capital budgets. ProCuity beds saw extremely strong demand, and the order book remains elevated. Products like the LIFEPAK 35, just launched in Europe, are opening new growth avenues.

Trauma and Extremities Momentum: This business grew 13.2% with double-digit gains in Upper Extremities and core trauma. Mako Shoulder remains in limited launch but shows strong early adoption. The Pangea plating portfolio continues driving market share gains.

Inari Integration: The vascular business delivered double-digit pro forma growth with procedural growth in the teens. Destocking will be complete by Q1 2026, removing a growth headwind. International expansion through Stryker’s infrastructure begins accelerating in H2 2026.

2. Operating margins: 26.9%

Stryker operates with disciplined margin expansion despite external pressures.

Current Performance: Q3 adjusted operating margin reached 25.6%, up 90 basis points year-over-year. This marks the second consecutive year of 100 basis points of margin expansion.

Tariff Management: Despite $200 million in tariff impacts for 2025, the company still delivered strong margin improvement through business mix optimization, supply chain efficiency, and manufacturing improvements.

Pricing Power: The company maintains positive pricing across most businesses, particularly in MedSurg. Orthopaedics pricing remains above historic levels as the company leverages innovation and differentiated products.

3. Exit P/E Multiple: 23.6x

The market currently values Stryker at 24.5x earnings. We assume multiple contracts at a modest 23.6x through our forecast period.

Reflects Maturity and Quality: Stryker’s P/E has averaged 27x over the past year and 26.4x over 5 years. The current multiple reflects a high-quality business with proven execution, though growth is moderating from double-digit levels.

Premium Warranted: Stryker deserves a market premium due to its market-leading Mako platform (150+ installations in Q3 alone), diversified portfolio across high-margin segments, strong international expansion opportunity (only 6.3% organic growth suggests upside), proven M&A track record, and consistent margin expansion.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

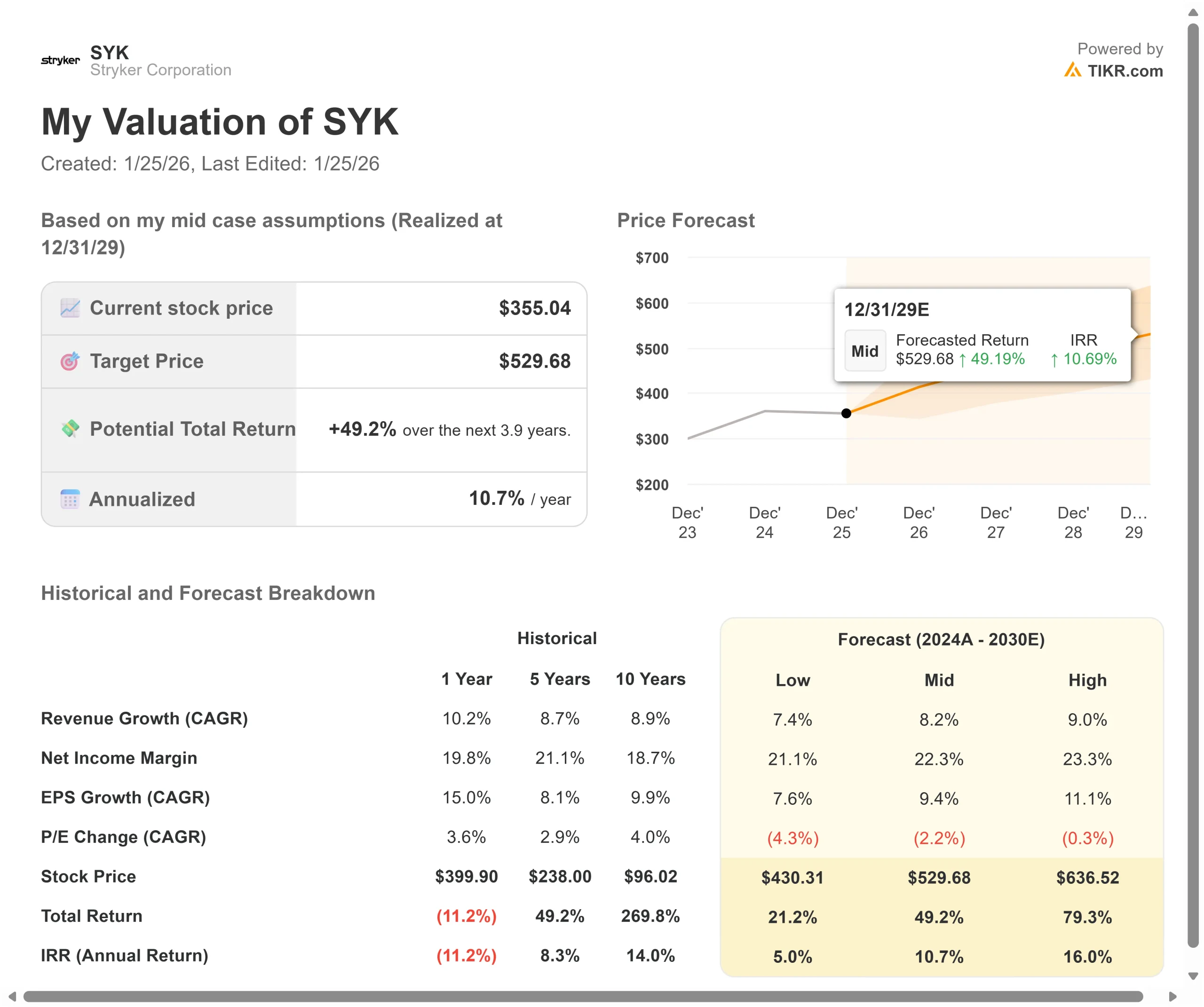

Medical device businesses face competition, regulatory, and macro risks. Here’s how Stryker stock might perform under different scenarios through December 2027:

- Low Case: If revenue growth slows to 7.4% and margins compress to 21.1%, the stock still offers a 5% annual return

- Mid Case: With 8.2% growth and 22.3% margins (our base assumptions), we expect an annual return of 10.7%

- High Case: If robotic adoption accelerates and Stryker maintains 23.3% margins while growing at 9%, returns could hit 16% annually

See what analysts think about SYK stock right now (Free with TIKR) >>>

The range reflects different adoption curves for Mako, the success of the Inari integration, and international expansion timing. In the worst case, tariffs intensify further, competition pressures pricing, or capital spending weakens.

In the high case, Mako Shoulder reaches full launch sooner than expected, Inari international expansion accelerates, destocking completes early, and M&A adds meaningful growth faster than anticipated.

How Much Upside Does Stryker Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!